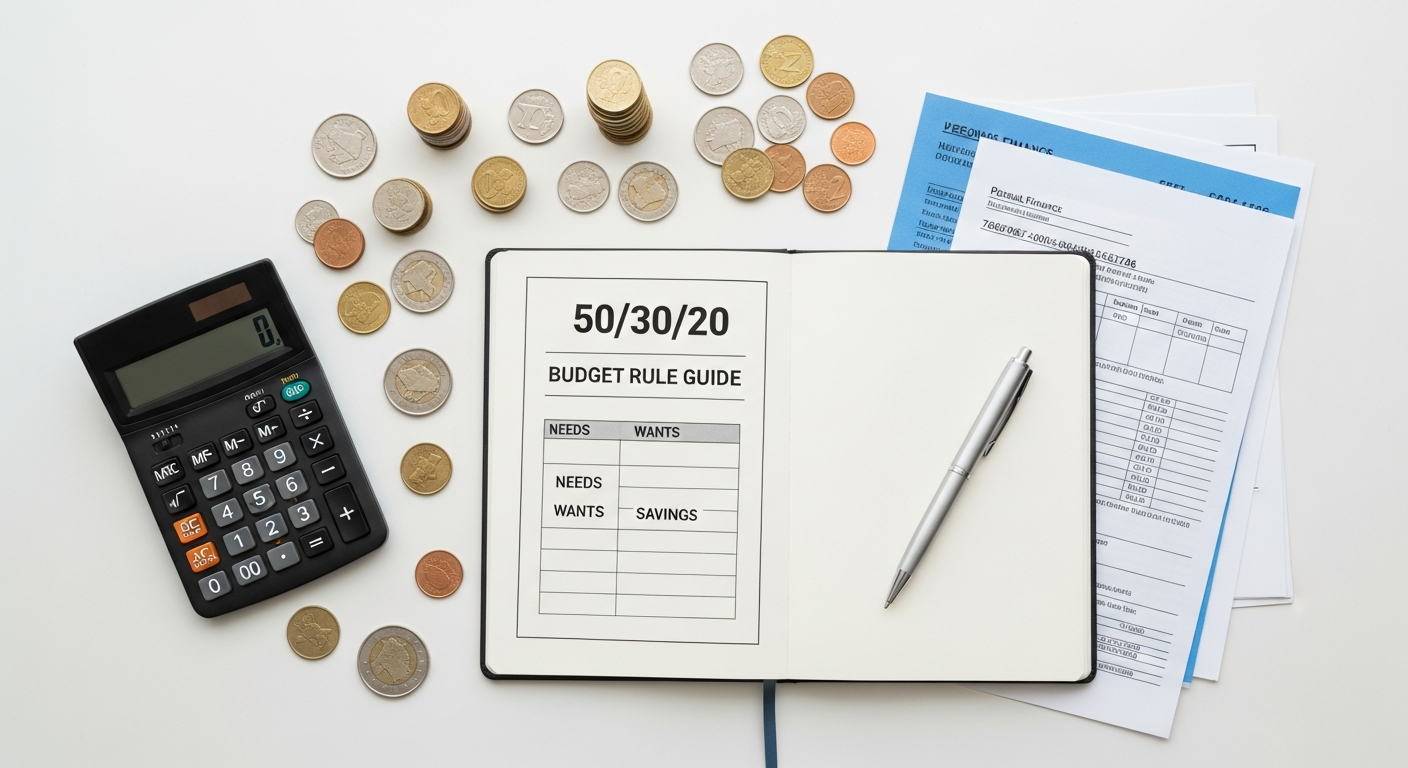

Understanding the 50/30/20 Budget Rule: A Foundational Principle for Financial Success

The 50/30/20 budget rule is more than just a budgeting technique; it’s a philosophy that simplifies money management into three core categories based on percentages of your after-tax (net) income. The premise is elegantly simple: 50% of your income should go towards Needs, 30% towards Wants, and 20% towards Savings & Debt Repayment. This rule’s enduring popularity stems from its balance between disciplined saving and the flexibility to enjoy life, making it a sustainable model for long-term financial health.

Unlike overly restrictive budgets that can lead to burnout, or overly lax approaches that result in financial drift, the 50/30/20 rule provides a balanced framework. It acknowledges that life involves both essential expenses and discretionary spending, while crucially prioritizing future financial security. For many, the initial challenge with budgeting is often the sheer complexity of tracking every single dollar. This rule abstracts that complexity, allowing you to focus on the broader allocation of your funds, which can be particularly empowering for those new to structured financial planning or those who have found other methods too cumbersome.

The beauty of this framework lies in its adaptability. While the percentages serve as a robust guideline, the rule understands that individual circumstances vary. It provides a strong foundation upon which you can build, offering a clear roadmap to allocate your income effectively. By consistently applying the 50/30/20 budget rule guide, you gain not just control over your finances, but also a profound understanding of your spending habits and priorities, which is the first step towards achieving any significant financial goal, from building an emergency fund to planning for retirement.

Deconstructing the 50%: Your Essential Needs

The largest portion of your income, 50%, is allocated to your essential Needs. These are the non-negotiable expenses that are absolutely vital for your survival and maintaining your basic standard of living. Without these, your life would be significantly disrupted or impossible to sustain. Understanding and accurately categorizing your needs is paramount for the 50/30/20 budget rule to function effectively. Misclassifying wants as needs is a common pitfall that can derail your budget before it even begins.

Typical expenses that fall under the 50% Needs category include:

- Housing: Rent or mortgage payments. This is often the single largest expense for most households.

- Utilities: Electricity, gas, water, and basic internet services. While internet might seem like a luxury to some, in the modern era, it’s often essential for work, education, and even accessing basic services.

- Groceries: Food purchased for home consumption. This specifically refers to staple foods, not dining out or gourmet ingredients for hobbies.

- Transportation: Car payments, fuel, public transport fares, basic car maintenance, and insurance. This covers getting to work or necessary appointments.

- Healthcare: Health insurance premiums, essential prescription medications, and unavoidable medical co-pays.

- Minimum Debt Payments: The absolute minimum payments required on credit cards, student loans, or other debts to avoid late fees and negative impacts on your credit score. Note that anything beyond the minimum payment falls into the 20% savings category.

For many individuals and families, staying within the 50% allocation for needs can be a significant challenge, especially in high cost-of-living areas. If your needs consistently exceed 50% of your net income, it’s a clear signal that you need to re-evaluate your core expenses. This might involve exploring more affordable housing options, optimizing your transportation costs, or rigorously scrutinizing your grocery budget. This is where strategic financial maneuvering comes into play. For instance, you might explore opportunities to How To Negotiate Bills And Lower Expenses, a critical skill that can free up significant funds. This could involve calling your internet or insurance providers to inquire about better rates, reviewing your utility usage for potential savings, or even considering refinancing options for your mortgage or car loan if conditions are favorable.

The goal isn’t just to list your needs, but to actively manage them. Regularly reviewing these essential expenditures and seeking ways to reduce them, even incrementally, can have a profound impact on your overall budget. Every dollar saved in your “Needs” category is a dollar that can be redirected to your “Wants” or, even better, accelerated savings and debt repayment, significantly enhancing the power of your 50/30/20 budget rule guide.

Exploring the 30%: Your Wants and Lifestyle Choices

Defining “Wants” can sometimes be tricky, as what one person considers a want, another might argue is a need (e.g., a specific streaming service). The key distinction lies in whether you could live without it without severe detriment to your basic living standards. If the answer is yes, it’s a want. Examples of typical wants include:

- Dining Out & Takeaway: Meals from restaurants, cafes, or food delivery services.

- Entertainment: Movies, concerts, sporting events, streaming subscriptions (beyond a basic necessity for information/work), video games, hobbies.

- Vacations & Travel: Leisure trips, weekend getaways, and related expenses.

- Shopping (Non-Essential): New clothes, gadgets, home decor, or other items purchased for pleasure rather than necessity.

- Premium Services: High-tier internet packages, gym memberships (if not medically necessary), personal training, expensive beauty treatments.

- Hobbies & Leisure Activities: Costs associated with personal interests like art supplies, club memberships, or specialized sports equipment.

- Gifts & Donations: While admirable, these are generally discretionary expenses.

The 30% for wants isn’t a license for reckless spending; rather, it’s an invitation for mindful indulgence. This category provides the flexibility to enjoy the fruits of your labor, preventing the feeling of deprivation that can often lead to budget abandonment. However, it requires a conscious effort to ensure these expenses don’t creep into your needs or, more critically, eat into your savings and debt repayment goals.

One effective strategy for managing your wants is to prioritize them. If you have multiple desires, decide which ones bring you the most joy or value and allocate your 30% accordingly. Perhaps you value travel more than dining out, or a specific hobby more than new clothes. By making deliberate choices, you ensure your discretionary spending aligns with your true values. Furthermore, this is an excellent area to practice cost-saving measures without feeling completely deprived. For example, instead of multiple streaming services, choose one or two. Opt for a home-cooked meal with friends instead of an expensive restaurant. These small adjustments, when consistently applied, can keep your wants within the 30% limit, reinforcing the integrity of your 50/30/20 budget rule guide while still allowing for a fulfilling lifestyle.

Maximizing the 20%: Your Financial Future and Debt Repayment

The final, yet arguably most crucial, component of the 50/30/20 budget rule is the 20% allocated to Savings & Debt Repayment. This category is the engine of your financial growth and security, designed to build wealth, protect against unforeseen circumstances, and free you from the burden of high-interest debt. Consistently dedicating this portion of your income is a non-negotiable step towards achieving long-term financial independence and peace of mind.

What falls into the 20% category?

- Emergency Fund: This is paramount. Aim for at least 3-6 months’ worth of essential living expenses stored in an easily accessible, high-yield savings account. This fund acts as a critical safety net against job loss, medical emergencies, or unexpected home repairs, preventing you from incurring new debt.

- Retirement Savings: Contributions to tax-advantaged accounts like a 401(k) (especially if your employer offers a match – always contribute at least enough to get the full match, as it’s free money!), Roth IRA, or Traditional IRA. Starting early with retirement savings allows the power of compounding to work its magic over decades.

- Investments: Contributions to brokerage accounts for long-term growth, mutual funds, ETFs, or other investment vehicles beyond retirement accounts.

- High-Interest Debt Repayment: Any payments above the minimum required on credit cards, personal loans, or other consumer debts with high interest rates. Aggressively tackling these debts saves you money in interest and frees up cash flow in the long run.

- Future Goals: Saving for a down payment on a house, a child’s education, a new car, or any other significant future purchase.

The 20% allocation is where the real magic of wealth building begins. By consistently saving and investing, you leverage the power of compounding, where your money earns returns, and those returns, in turn, earn more returns. Over time, this snowball effect can lead to substantial wealth accumulation. For example, starting to invest just $100 per month at age 25 could result in a significantly larger sum by retirement than starting at age 35, thanks to those extra ten years of compounding.

Furthermore, dedicating a significant portion to accelerated debt repayment, especially high-interest debt, is a powerful form of “saving.” Every dollar you pay off early is a dollar you save on future interest payments. This strategy not only reduces financial stress but also liberates more of your income for future investments once the debt is cleared. This disciplined approach to the 20% is not just about personal financial security; it’s a cornerstone of How To Build Generational Wealth. By establishing strong savings habits, investing wisely, and eliminating debt, you create a robust financial legacy that can benefit your family for generations to come. This might involve setting up trusts, teaching financial literacy to your children, or making strategic investments that grow over time. The 20% isn’t merely about personal gain; it’s about securing a brighter financial future for you and your lineage, transforming your financial discipline into a lasting legacy.

Implementing the 50/30/20 Rule: A Step-by-Step Guide to Budgeting Success

Understanding the theory behind the 50/30/20 budget rule guide is one thing; putting it into practice is another. This section provides a practical, step-by-step methodology for implementing this rule, ensuring you can effectively manage your money and achieve your financial aspirations. This process is essentially a comprehensive guide on How To Create A Monthly Budget using the 50/30/20 framework.

Step 1: Calculate Your Net Income

Your net income is the amount of money you actually receive after taxes, deductions for health insurance, retirement contributions (if pre-tax), and any other payroll deductions. This is the crucial figure upon which your 50/30/20 percentages will be based. If your income varies, use an average of the last few months or a conservative estimate to avoid over-budgeting. If you contribute to a 401(k) or similar retirement account pre-tax, the 20% savings category will apply to your net income after that deduction, meaning you might be saving more than 20% in total, which is an excellent bonus!

Step 2: Track Your Spending

Before you can allocate, you need to understand where your money is currently going. For at least one month, diligently track every single dollar you spend. Use a budgeting app, a spreadsheet, or even a simple notebook. This step is critical for gaining insight into your actual spending habits, which may differ significantly from what you perceive them to be. This data will be invaluable for the next step.

Step 3: Categorize Your Expenses (Needs, Wants, Savings/Debt)

Now, take your tracked expenses and sort them into the three 50/30/20 categories. Be brutally honest with yourself. Is that daily latte a need or a want? Is that premium cable package truly essential? This categorization process is often eye-opening and highlights areas where your current spending deviates from the ideal 50/30/20 split. Remember the definitions:

- Needs (50%): Essentials for survival and basic living.

- Wants (30%): Discretionary spending for enjoyment and lifestyle.

- Savings & Debt Repayment (20%): Emergency fund, retirement, investments, extra debt payments.

Compare your current spending percentages against the 50/30/20 targets. Don’t be discouraged if they don’t align perfectly initially; this is a learning process.

Step 4: Adjust and Optimize Your Spending

Based on your categorization, identify areas where you need to make adjustments to align with the 50/30/20 rule.

- If Needs > 50%: Look for ways to reduce core expenses. Can you negotiate bills, find cheaper insurance, reduce grocery costs, or consider a more affordable living situation? This is where strategies for How To Negotiate Bills And Lower Expenses become invaluable.

- If Wants > 30%: Determine which discretionary expenses you can cut back on or eliminate. Can you cook more at home, limit subscriptions, or find free entertainment options? Prioritize the wants that bring you the most joy.

- If Savings & Debt Repayment < 20%: You’ll need to free up funds from your Needs or Wants categories to meet this target. Remember, this 20% is crucial for your financial future.

Create a new budget based on these adjusted allocations. This might be a trial-and-error process for the first few months.

Step 5: Automate Your Savings and Debt Repayment

One of the most powerful strategies for success with the 50/30/20 rule is automation. Set up automatic transfers from your checking account to your savings, investment, and debt repayment accounts immediately after you get paid. “Pay yourself first” ensures that your 20% is secured before you have a chance to spend it. This removes the temptation to dip into your future security and builds consistent financial habits without conscious effort.

Step 6: Review and Adapt Regularly

Your financial situation is not static. Life changes, income fluctuates, and goals evolve. Make it a habit to review your 50/30/20 budget monthly or quarterly. Are your allocations still realistic? Have your needs changed? Are you on track with your savings goals? Adjust as necessary. For instance, as you approach 2026, you might want to review your investment strategy or adjust your savings targets based on market performance or new financial goals. This regular review ensures your budget remains a living, breathing document that serves your current financial reality and future aspirations.

Beyond the Basics: Advanced Strategies for Long-Term Financial Mastery

While the 50/30/20 budget rule guide provides an excellent foundation, truly mastering your finances involves looking beyond the basic allocations and employing advanced strategies. For those aiming not just for financial stability but for significant wealth accumulation and even How To Build Generational Wealth, these additional tactics can supercharge your progress.

Aggressive Debt Repayment Strategies

Once your emergency fund is sufficiently established, consider redirecting even more than the minimum 20% towards high-interest debt. Strategies like the debt snowball (paying off the smallest debt first to build momentum) or the debt avalanche (paying off the highest-interest debt first to save the most money) can accelerate your journey to becoming debt-free. By eliminating consumer debt, you free up substantial cash flow that can then be fully redirected to investments, dramatically increasing your wealth-building capacity.

Income Optimization and Diversification

Budgeting often focuses on cutting expenses, but increasing your income is an equally powerful lever. Explore opportunities for professional development to earn a raise, consider a side hustle, or even invest in skills that allow for higher-paying work. Diversifying your income streams provides greater financial resilience and more capital to fuel your 20% savings and investment goals. Every extra dollar earned, when strategically applied to savings or debt, amplifies the effectiveness of your 50/30/20 framework.

Strategic Investing and Portfolio Diversification

Don’t just save; invest wisely. Beyond basic retirement accounts, explore diversified investment portfolios tailored to your risk tolerance and time horizon. This might include a mix of stocks, bonds, real estate, or even alternative investments. Understanding concepts like asset allocation, rebalancing, and tax-loss harvesting can significantly enhance your long-term returns. For those looking to build generational wealth, these investment decisions become even more critical, often involving setting up trusts, engaging in estate planning, and educating future generations on financial literacy.

Leveraging Tax-Advantaged Accounts

Maximize contributions to all available tax-advantaged accounts. This includes not only 401(k)s and IRAs but also Health Savings Accounts (HSAs), 529 plans for education, and potentially Roth conversions. These accounts offer significant tax benefits that can dramatically accelerate your wealth accumulation, effectively making your money work harder for you. Understanding the nuances of these accounts can save you thousands in taxes over your lifetime, allowing more of your hard-earned money to grow.

Financial Planning and Legacy Building

For those aspiring to build generational wealth, comprehensive financial planning is essential. This involves working with a financial advisor to develop a long-term strategy that encompasses investment planning, estate planning, risk management, and philanthropic goals. It’s about creating a legacy that extends beyond your lifetime, providing financial security and opportunities for future generations. This might involve structured gifting, setting up educational funds for grandchildren, or establishing family foundations, all rooted in the disciplined financial habits initiated by your consistent application of the 50/30/20 rule.

By integrating these advanced strategies with the fundamental principles of the 50/30/20 budget rule, you move beyond mere budgeting to a holistic approach to financial mastery. This journey is continuous, requiring regular review and adaptation, but the rewards of financial freedom, security, and the ability to build a lasting legacy are immeasurable as we look towards a prosperous 2026 and beyond.

Frequently Asked Questions

Is the 50/30/20 rule suitable for everyone?▾

What if my needs exceed 50% of my income?▾

How do I track my spending effectively for this budget?▾

Budgeting Apps: Many apps (e.g., Mint, YNAB, Personal Capital) link to your bank accounts and automatically categorize transactions.

Spreadsheets: A simple Excel or Google Sheets document can be customized to track income and expenses.

Manual Tracking: A notebook or ledger for those who prefer a hands-on approach.

The most important aspect is consistency. Choose a method you’ll stick with daily or weekly to ensure an accurate picture of your cash flow and adherence to your budget categories.

Can I use the 50/30/20 rule if I have a lot of debt?▾

What’s the difference between “needs” and “wants”?▾

Needs: Essential expenses required for survival and maintaining a basic standard of living. You would face severe hardship or inability to function without them (e.g., basic shelter, food, utilities, transportation to work, essential healthcare).

Wants: Discretionary expenses that improve your quality of life, provide enjoyment, or fulfill desires, but are not strictly necessary for survival. You could live without them (e.g., dining out, entertainment, vacations, designer clothes, premium streaming services).

The key is honest self-assessment. While a smartphone might feel like a need, the latest model with unlimited data might be a want, while a basic plan is a need.

How often should I review my 50/30/20 budget?▾

Recommended Resources

You might also enjoy Tax Deductions Everyone Should Know from Trading Costs.

Related reading: Facebook Ads For Ecommerce Beginners (E-ComProfits).

From Our Network

- how to do a content audit (en Pagerelease)

- how to use data-driven marketing to grow faster (en Kacerr)

- what is a Roth IRA and should you open one (en Assetbar)