The Indispensable Value of Tracking Your Spending

Before diving into the “how,” it’s crucial to solidify the “why.” Understanding the profound benefits of tracking your spending provides the motivation necessary to transform this practice from a chore into a powerful financial habit. Many people believe they have a good handle on their finances, only to be surprised when they actually see the numbers laid out. This initial shock often turns into the catalyst for significant positive change.

Firstly, tracking your spending offers unparalleled financial clarity. It replaces vague assumptions with concrete data, showing you exactly where every dollar originates and where it ultimately lands. This transparency is the first step towards taking control. Without this knowledge, budgeting becomes a guessing game, and financial planning is akin to navigating a ship without a compass.

Secondly, it empowers you to identify and eliminate wasteful spending. Those small, seemingly insignificant daily purchases – the extra coffee, the impulse online buy, the unused subscription – can collectively drain hundreds, if not thousands, of dollars from your accounts each year. By meticulously logging every transaction, these “spending leaks” become glaringly obvious, presenting immediate opportunities to redirect funds towards more meaningful goals. Imagine discovering that simply cutting out a few unnecessary habits could free up enough money to fund a significant portion of your emergency fund or accelerate your debt repayment plan.

Furthermore, spending tracking is the precursor to effective budgeting. It provides the real-world data needed to accurately How To Create A Monthly Budget that is realistic, sustainable, and tailored to your actual spending habits. Instead of making arbitrary allocations, you can base your budget on historical data, making it far more likely to stick. This synergy between tracking and budgeting creates a virtuous cycle of financial improvement.

Finally, and perhaps most importantly, consistent spending tracking significantly contributes to your long-term financial goals, including building wealth. By understanding your cash flow, you can optimize your savings rate, identify funds to invest, and make strategic decisions that propel you towards financial independence. Whether your goal is to save for a down payment, retire early, or embark on the journey of How To Build Generational Wealth, knowing precisely where your money is going is the critical first step. It shifts you from a reactive financial stance to a proactive one, putting you firmly in the driver’s seat of your financial destiny.

Traditional Methods for Manual Spending Tracking

While the digital age offers a plethora of sophisticated tools, sometimes the simplest methods are the most effective, especially for beginners or those who prefer a hands-on approach. Traditional spending tracking methods, though requiring more discipline, offer a tangible connection to your money that digital solutions might sometimes obscure.

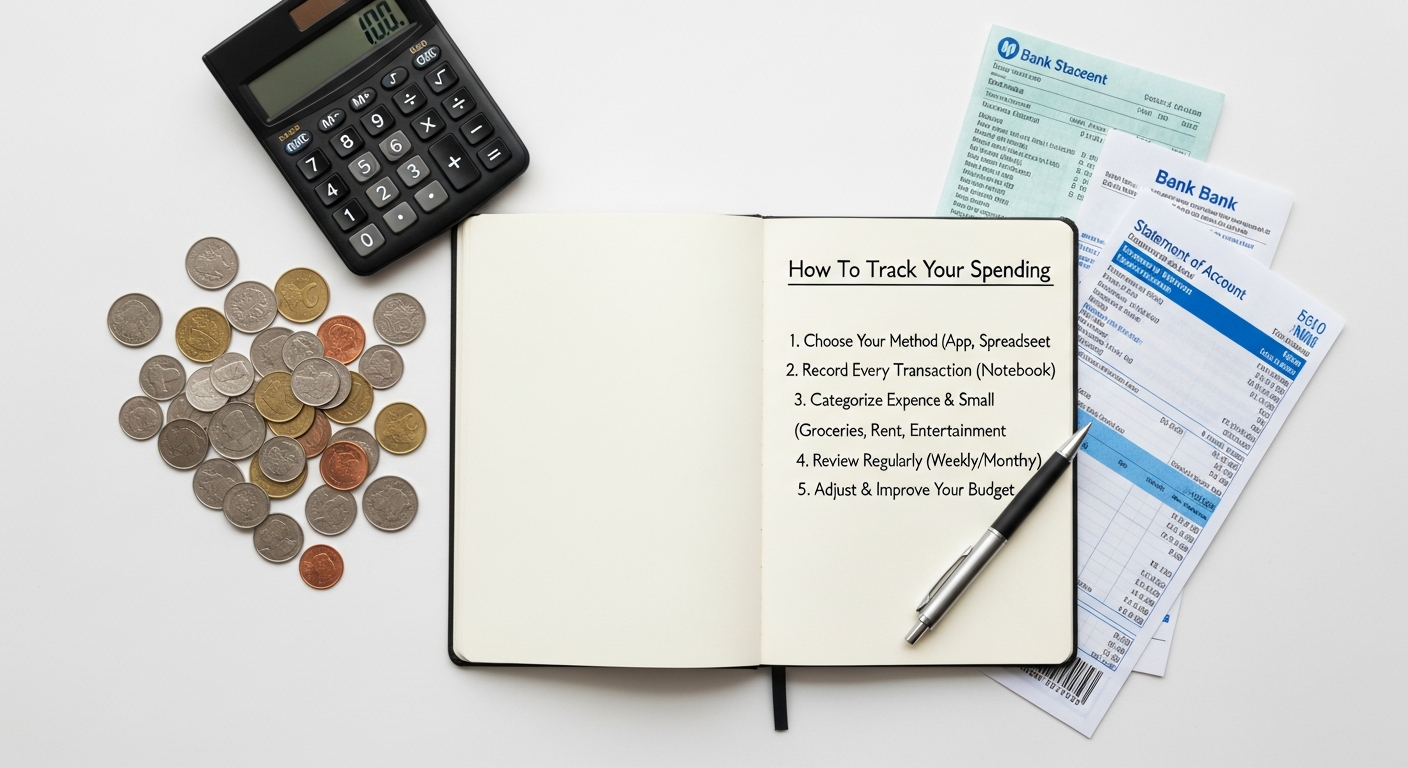

The classic pen and paper method remains a timeless choice. This involves simply carrying a small notebook and jotting down every single expense as it occurs, no matter how small. Alongside the amount, you’d note the date, the vendor, and the category (e.g., groceries, transport, entertainment). At the end of the day or week, you would tally up your expenses by category.

Pros of Pen and Paper:

- Simplicity: No apps to download, no technology to learn.

- Tangibility: The physical act of writing can reinforce awareness.

- Accessibility: Requires only a pen and paper, readily available.

- Zero Cost: Virtually free to implement.

Cons of Pen and Paper:

- Manual Effort: Highly dependent on consistent, manual input.

- Prone to Errors: Calculation mistakes can easily occur.

- Lack of Automation: No automatic categorization or data analysis.

- Loss Risk: Easy to misplace or damage your notes.

A step up in organization is the use of spreadsheets, whether on Excel, Google Sheets, or similar programs. This method leverages the power of digital tables and basic formulas to automate calculations and organize data more efficiently. You would manually input your transactions, but the spreadsheet can automatically sum categories, calculate totals, and even create simple charts. Many free templates are available online to get you started, or you can create one from scratch.

Pros of Spreadsheets:

- Customization: Fully adaptable to your specific needs and categories.

- Automation (Basic): Formulas can handle calculations, reducing manual errors.

- Data Visualization: Can generate graphs and charts for better insights.

- Scalability: Can manage large amounts of data over time.

Cons of Spreadsheets:

- Manual Data Entry: Still requires diligent input of every transaction.

- Learning Curve: Basic spreadsheet knowledge is helpful for effective use.

- Time-Consuming: Can be tedious, especially if not updated regularly.

- No Real-time Sync: Doesn’t automatically pull data from bank accounts.

The envelope system, while primarily a budgeting technique, is also a form of spending tracking for cash-based expenses. This involves allocating physical cash into separate envelopes for different spending categories (e.g., “Groceries,” “Entertainment,” “Dining Out”) at the beginning of the month. Once an envelope is empty, spending in that category stops until the next month. While effective for cash, its utility diminishes with increasing reliance on digital payments.

Regardless of the traditional method chosen, the key to success lies in consistent execution and unwavering discipline. These methods force a direct engagement with your money, fostering a heightened sense of awareness that can be incredibly valuable in kickstarting your journey towards financial mastery.

Leveraging Digital Tools and Apps for Effortless Tracking

Budgeting Apps and Personal Finance Software stand at the forefront of this digital revolution. Platforms like Mint, YNAB (You Need A Budget), Personal Capital, and PocketGuard offer comprehensive features that go far beyond simple transaction logging. These apps typically connect directly to your bank accounts, credit cards, and even investment portfolios, automatically importing and categorizing your transactions.

Key Features of Budgeting Apps:

- Automatic Transaction Import: Eliminates manual data entry, significantly reducing the time commitment.

- Smart Categorization: Uses AI and machine learning to categorize expenses, often allowing for customization and rule creation.

- Real-time Updates: Provides an up-to-the-minute view of your financial standing.

- Budgeting Tools: Integrates tracking with budgeting features, allowing you to set spending limits and monitor progress.

- Goal Tracking: Helps you set and monitor progress towards financial goals like saving for a down payment or retirement.

- Net Worth Tracking: Aggregates all your assets and liabilities to show your overall financial health.

- Reporting and Analytics: Generates visual reports, charts, and graphs to help you understand spending patterns and trends.

Pros of Budgeting Apps:

- Convenience: Automates most of the tracking process.

- Comprehensive View: Centralizes all financial data in one place.

- Powerful Insights: Advanced analytics reveal spending patterns and opportunities for savings.

- Accessibility: Available on mobile devices, allowing for on-the-go monitoring.

Cons of Budgeting Apps:

- Security Concerns: Requires linking bank accounts, raising data privacy questions for some users.

- Subscription Fees: Many of the most robust apps come with a monthly or annual cost.

- Learning Curve: Can take time to set up and customize effectively.

- Over-reliance: Can lead to less active engagement with your money if not used mindfully.

Beyond dedicated budgeting apps, your bank and credit card apps often provide surprisingly robust spending tracking features. Most financial institutions now offer transaction categorization, spending summaries, and even budgeting tools directly within their mobile applications. While these might not be as comprehensive as specialized budgeting software, they offer a convenient and secure way to monitor your primary accounts without needing to share your data with a third party.

Finally, receipt scanning apps can be invaluable for tracking cash expenses or business-related outgoings. Apps like Expensify or Shoeboxed allow you to snap a photo of a receipt, which then digitizes the information, categorizes it, and stores it in the cloud. This not only aids in tracking but also simplifies tax preparation and expense reporting.

When choosing a digital tool, consider your personal preferences, your comfort level with technology, and your specific financial goals. The best app is the one you will consistently use. Experiment with a few free options or trials to find the perfect fit that integrates seamlessly into your financial routine for 2026.

The Art of Categorization and Analysis: Making Sense of Your Data

Simply logging transactions, whether manually or automatically, is only half the battle. The true power of spending tracking lies in the intelligent categorization and subsequent analysis of that data. Without proper categorization, your spending log is just a list of numbers; with it, it transforms into a treasure map revealing your financial habits and pointing towards opportunities for growth.

The first step is establishing a consistent set of categories. These should be broad enough to capture similar expenses but specific enough to provide meaningful insights. Common categories include:

- Fixed Expenses: Rent/Mortgage, Loan Payments, Insurance Premiums, Subscriptions.

- Variable Expenses: Groceries, Dining Out, Utilities (can vary), Transportation, Entertainment, Clothing, Personal Care.

- Savings/Investments: Contributions to emergency fund, retirement accounts, investment portfolios.

- Debt Repayment: Extra payments beyond minimums.

It’s crucial to distinguish between needs and wants. Needs are essential for living (housing, food, basic utilities), while wants are discretionary (dining out, entertainment, designer clothes). Clear categorization helps you identify where your “want” spending truly stands. Many digital tools offer default categories, but you should customize them to reflect your unique lifestyle and priorities. For example, if you have multiple pets, “Pet Care” might be a more useful category than lumping it under “Miscellaneous.”

Once you have your categories, consistent application is paramount. Every transaction should be assigned to its appropriate category. This is where digital tools shine, often learning your preferences over time. For manual methods, this requires diligence. Avoid creating an “Other” or “Miscellaneous” category that becomes a dumping ground for too many expenses, as this defeats the purpose of granular insights.

The real magic happens during the analysis phase. Set aside dedicated time each week or month to review your spending data. This is not about judgment, but about understanding. Ask yourself critical questions:

- Where did most of my money go this month?

- Are there any categories where I consistently overspend?

- Are my expenses aligned with my financial goals and values?

- Could I have reduced spending in any particular area without significant sacrifice?

- Are there any unexpected or recurring expenses I wasn’t aware of?

Looking at trends over several months can be even more revealing. You might notice seasonal spikes in utility bills, or that your “dining out” budget consistently creeps up during certain times of the year. This historical data provides a powerful foundation for future financial planning and for understanding your true cost of living.

This analytical process directly feeds into your ability to How To Create A Monthly Budget. By understanding your actual spending patterns, you can create a budget that is not only realistic but also effective in guiding your financial decisions. It empowers you to make informed adjustments, reallocate funds, and identify specific areas where you can cut back without feeling deprived. For instance, if your analysis reveals a high spend on subscriptions you rarely use, this data can prompt you to How To Negotiate Bills And Lower Expenses, potentially canceling or downgrading services to save money. This proactive approach transforms raw data into actionable intelligence, propelling you closer to your financial aspirations for 2026 and beyond.

Integrating Spending Tracking with Your Financial Goals

Spending tracking is not an end in itself; it is a powerful means to achieve your broader financial objectives. The true efficacy of knowing where your money goes comes from its integration into your overall financial strategy, linking daily habits to long-term aspirations. Without this connection, tracking can feel like a pointless exercise.

The most immediate connection is to budgeting. As discussed, your spending data provides the empirical evidence needed to How To Create A Monthly Budget that is grounded in reality. Instead of guessing how much you spend on groceries or entertainment, you’ll know. This data-driven approach removes much of the frustration often associated with budgeting, making it more sustainable. Your tracking insights allow you to set realistic spending limits for each category, ensuring your budget is a practical roadmap, not an idealistic wish list. Regular review of your tracked spending against your budget helps identify areas where adjustments are needed, allowing you to fine-tune your financial plan throughout 2026.

Beyond budgeting, spending tracking is instrumental in identifying opportunities for savings and expense reduction. When you categorize and analyze your expenses, you inevitably uncover areas where you might be overspending or where money is simply slipping through the cracks. This might be recurring subscriptions you no longer use, excessive dining out, or even inefficient utility usage. This knowledge empowers you to take action. For instance, discovering a high monthly bill for internet or car insurance could prompt you to explore How To Negotiate Bills And Lower Expenses. Armed with precise figures, you can approach service providers with confidence, demonstrating your awareness and pushing for better deals. Every dollar saved through conscious reduction can be directly redirected towards your financial goals.

Furthermore, spending tracking plays a critical role in setting and achieving realistic financial goals. Whether you’re saving for a down payment on a house, planning a dream vacation, building an emergency fund, or investing for retirement, knowing your cash flow is non-negotiable. By understanding your discretionary income – the money left after all essential expenses and savings contributions – you can determine how quickly you can reach your targets. This clarity allows you to set aggressive yet attainable milestones, providing the motivation to stick to your plan. You can visualize how cutting back on certain expenses translates directly into accelerating your progress towards these goals.

Crucially, consistent spending tracking is a cornerstone for those aspiring to How To Build Generational Wealth. Building significant wealth requires not just earning money, but effectively managing and investing it. Tracking provides the fundamental data needed to maximize your savings rate, identify funds for investment, and ensure your financial decisions align with your long-term vision. It fosters a discipline and awareness that are essential for sustained financial growth, allowing you to make strategic choices that compound over time, securing a prosperous future for yourself and your descendants. In essence, spending tracking transforms your financial aspirations from abstract dreams into concrete, actionable plans, providing the data-driven clarity needed to navigate your path to prosperity in 2026 and beyond.

Overcoming Common Spending Tracking Challenges

While the benefits of spending tracking are undeniable, the journey is not without its hurdles. Many individuals start with great enthusiasm only to find themselves struggling with consistency or feeling overwhelmed. Recognizing these common challenges and equipping yourself with strategies to overcome them is key to turning tracking into a sustainable habit.

One of the most frequent obstacles is a lack of consistency. Life gets busy, and tracking expenses can feel like an extra chore. To combat this, aim to integrate tracking into your existing routine. If you use a digital app, dedicate 5-10 minutes each morning or evening to review and categorize transactions. For manual methods, make it a habit to log purchases immediately. Set reminders on your phone, or link it to another daily task, like checking emails or having your morning coffee. Remember, consistency over perfection is the goal. A few missed transactions are less detrimental than giving up entirely.

Another challenge is feeling overwhelmed, especially when starting out or dealing with a complex financial situation. The sheer volume of transactions or the unfamiliarity with budgeting concepts can be daunting. The solution here is to start small. Don’t try to track every single penny perfectly from day one. Begin by focusing on your biggest spending categories, like housing, food, and transportation. Once you’ve mastered those, gradually add more detail. If using a spreadsheet, use a simple template before attempting to build a complex system. Break down the task into manageable chunks.

Forgetting to log transactions is a common issue, particularly with cash purchases. This is where digital tools offer a distinct advantage by automatically importing most debit and credit card transactions. For cash, make it a rule to get a receipt for every purchase and log it immediately, or at least before the end of the day. Some people keep a small “receipt wallet” to gather all paper receipts until they can be logged. The trick is to develop a system that minimizes the time between purchase and logging.

Emotional spending can also complicate tracking. When purchases are driven by stress, boredom, or excitement, they can often be impulsive and difficult to categorize or justify later. Tracking itself can help reveal patterns of emotional spending. If you notice spikes in certain categories during periods of stress, it’s an opportunity to address the underlying emotions rather than just the spending. This often requires a deeper dive into your relationship with money, but the tracking data provides the necessary insights.

Finally, dealing with irregular income or expenses presents a unique challenge. Freelancers, commission-based earners, or those with significant annual expenses (like insurance premiums or property taxes) might find monthly tracking less straightforward. For irregular income, focus on tracking expenses rigorously to understand your minimum monthly burn rate. For irregular expenses, create a sinking fund – setting aside a small amount each month into a separate savings account so the large annual bill doesn’t disrupt your budget. This proactive approach smooths out the financial impact and makes tracking more predictable. By anticipating these common hurdles and implementing these practical strategies, you can transform spending tracking from a potential burden into a powerful, enduring habit that serves your financial well-being in 2026 and beyond.

Advanced Strategies for Enhanced Financial Control

Once you’ve mastered the basics of spending tracking and integrated it into your financial routine, you can explore more advanced strategies to gain even greater control over your money and accelerate your financial progress. These techniques build upon the foundation of knowing where your money goes, transforming data into powerful levers for wealth building.

One highly effective advanced strategy is Zero-Based Budgeting (ZBB). While traditional budgeting allocates funds to categories, ZBB takes it a step further by assigning every single dollar of your income a “job” until your income minus your expenses (including savings and debt payments) equals zero. This ensures no money is left unaccounted for and compels you to be intentional with every penny. Your detailed spending tracking data is absolutely crucial for setting up an accurate and realistic zero-based budget. It helps you understand your true fixed and variable expenses, allowing you to allocate funds precisely. This method is particularly powerful for those looking to maximize savings and debt repayment, as it forces a conscious decision about where every dollar goes, greatly enhancing the effectiveness of your How To Create A Monthly Budget.

Another popular framework is the 50/30/20 Rule. This guideline suggests allocating 50% of your after-tax income to Needs, 30% to Wants, and 20% to Savings & Debt Repayment. Your meticulously tracked spending categories allow you to easily determine if your current allocations align with this rule. If you find your “Wants” are consistently exceeding 30%, your tracking data pinpoints exactly where adjustments need to be made. This rule provides a helpful benchmark for financial health and helps simplify the budgeting process once your spending patterns are clear.

Beyond just tracking, automating your savings and investments is a crucial advanced step. Once you understand your cash flow through diligent tracking, you can set up automatic transfers from your checking account to your savings, investment accounts, or debt repayment accounts immediately after you get paid. This “pay yourself first” approach ensures that your financial goals are prioritized, making it much harder to accidentally spend money earmarked for future wealth. This strategy is foundational for anyone serious about How To Build Generational Wealth, as it ensures consistent contributions to your growth engines.

Regular and structured financial reviews elevate spending tracking from a daily task to a strategic planning session. Beyond the weekly or monthly check-ins, consider conducting quarterly or annual deep dives into your financial data. During these reviews, analyze your spending trends over longer periods, assess your progress towards major goals, review your net worth, and make adjustments to your budget or financial plan for the coming months or the next year, such as for 2026. This is also an excellent time to look for opportunities to How To Negotiate Bills And Lower Expenses, as contracts and rates often change annually.

Finally, use your spending data to optimize debt repayment strategies. If you’re carrying high-interest debt, your tracking can reveal how much extra you can realistically afford to pay each month. This allows you to aggressively tackle debt using methods like the debt snowball or avalanche, freeing up cash flow faster for savings and investments. The clarity provided by comprehensive spending tracking empowers you to make informed, impactful decisions that go far beyond just knowing where your money goes; it actively helps you direct it towards a future of financial freedom and prosperity.

Frequently Asked Questions

Recommended Resources

Check out Social Media Marketing Tips 2026 on Page Release for a deeper dive.

Learn more about this topic in How To Diversify Your Investment Portfolio at AssetBar.