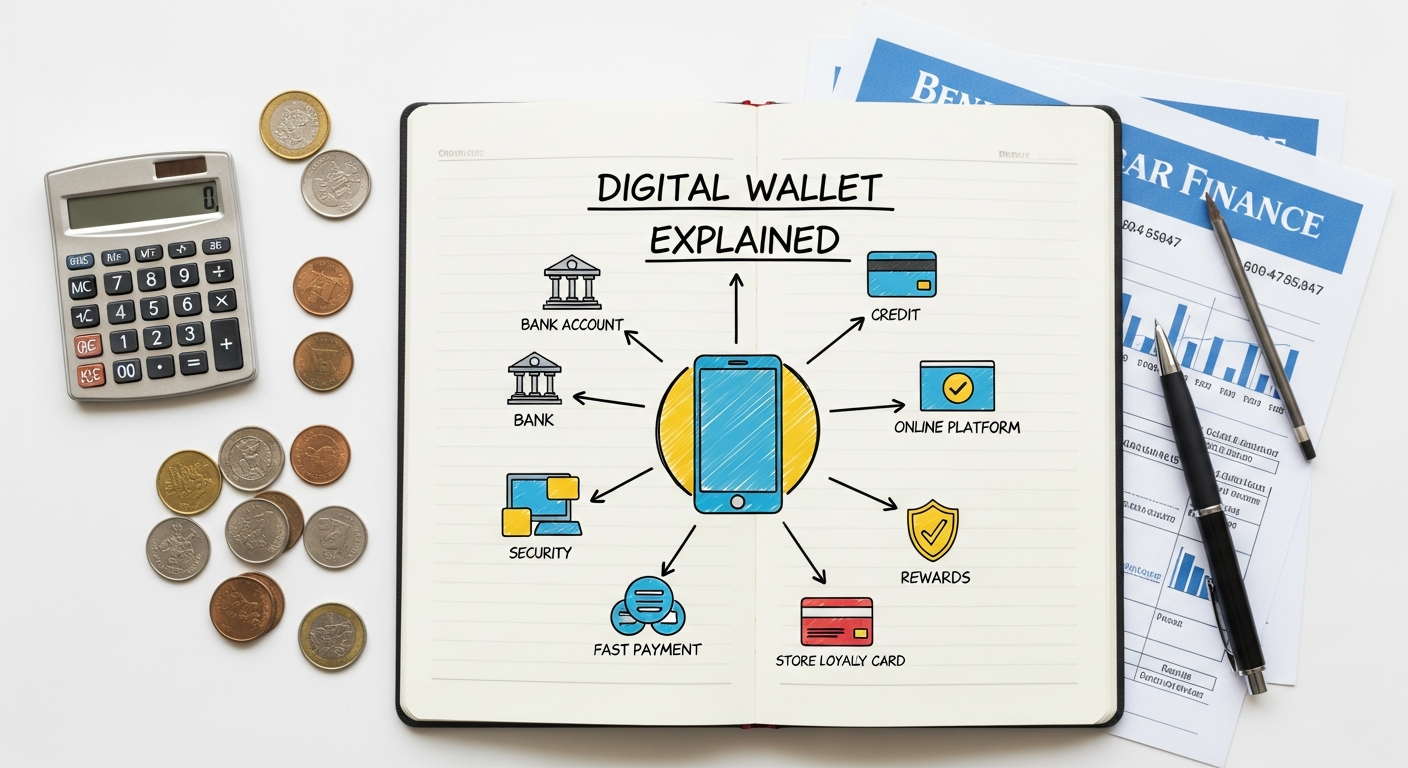

What Exactly is a Digital Wallet? An Essential Fin3go Explanation

At its core, a digital wallet, often interchangeably referred to as an e-wallet or mobile wallet, is a software-based system that securely stores payment information and passwords for numerous payment methods and websites. Instead of carrying a bulky physical wallet filled with credit cards, debit cards, loyalty cards, and even identification, a digital wallet centralizes all this data within a single, accessible application on your smartphone, tablet, or even smartwatch. Imagine having all your essential financial instruments neatly organized and available at your fingertips, ready to be deployed with a simple tap or scan.

The primary function of a digital wallet is to facilitate electronic transactions. This means you can make purchases in stores, online, or within apps without needing to physically present your cards or cash. Beyond mere payment processing, however, modern digital wallets have evolved into sophisticated financial management hubs. They can store gift cards, boarding passes, event tickets, and sometimes even digital versions of driver’s licenses or health insurance cards, depending on regional regulations and technological adoption.

The evolution of the digital wallet traces back to the early days of online payment systems like PayPal, which digitized money transfers and payments. However, the true ubiquitous emergence of the digital wallet as we know it today began with the advent of smartphones and Near Field Communication (NFC) technology. Companies like Apple, Google, and Samsung spearheaded this revolution, integrating secure payment capabilities directly into their mobile devices, making tap-to-pay functionality a mainstream reality.

For Fin3go readers, understanding this foundational concept is crucial because digital wallets are not just about convenience; they are about control, security, and a seamless integration of financial activities into daily life. They represent a significant leap forward in how we interact with our money, offering a blend of traditional banking services with innovative technological features that empower users with greater financial agility and insight. As we delve deeper, you’ll see how these tools are becoming indispensable for anyone looking to optimize their personal finance strategy.

The Mechanics Behind Digital Wallets: How They Work Their Magic

The seemingly effortless process of tapping your phone to pay or scanning a QR code at checkout belies a complex, multi-layered system designed for speed, efficiency, and paramount security. Understanding the underlying mechanics of a digital wallet is key to appreciating its value and trusting its capabilities.

The cornerstone of in-person digital wallet payments for many systems is Near Field Communication (NFC). This short-range wireless technology allows two devices, typically your smartphone and a payment terminal, to communicate when they are brought within a few centimeters of each other. When you initiate a payment, your digital wallet app sends encrypted payment information to the terminal via NFC. The terminal then processes this data with your bank or card issuer, much like a traditional card swipe, but without the physical card.

Another prevalent method, particularly in online payments, peer-to-peer transactions, and in regions where NFC infrastructure is less common, involves QR codes. A Quick Response (QR) code is a two-dimensional barcode that can be scanned by a smartphone camera. When used for payments, a merchant might display a QR code containing their payment details, which you scan to initiate a transfer, or your digital wallet might generate a unique QR code for the merchant to scan, authorizing the payment. This method is popular with apps like Venmo, Cash App, and various payment systems in Asia.

Tokenization: The Heart of Digital Wallet Security

Perhaps the most critical security feature underpinning digital wallets is tokenization. When you add a credit or debit card to your digital wallet, the actual card number is not stored directly on your device or transmitted during a transaction. Instead, your card issuer or payment network generates a unique, encrypted token—a randomized, disposable number—that represents your card information for that specific device.

- Enhanced Security: During a transaction, it’s this token, not your actual card number, that is passed to the merchant. If a data breach were to occur at the merchant’s end, hackers would only obtain this meaningless token, rendering it useless for fraudulent activity. Your real card number remains secure and isolated.

- Dynamic Nature: Some tokenization systems even generate a new, single-use token for each transaction, adding an extra layer of protection against interception and reuse.

Further Security Layers

Beyond tokenization, digital wallets incorporate several other robust security measures:

- Biometric Authentication: Most digital wallets require a fingerprint, facial scan, or PIN to authorize a payment or even access the app, ensuring that only you can use your wallet.

- Encryption: All data stored within the digital wallet and transmitted during a transaction is heavily encrypted, protecting it from unauthorized access.

- Multi-Factor Authentication (MFA): For initial setup or high-value transactions, digital wallets might employ MFA, requiring verification through a separate device or method.

- Device-Level Security: The security of your smartphone itself (passcodes, remote wipe capabilities) adds another layer of protection to your digital wallet.

These intricate mechanisms work in concert to make digital wallet transactions not just convenient, but often more secure than traditional card-based payments. For Fin3go readers keen on understanding the financial technology that underpins their daily lives, recognizing these security protocols provides peace of mind and reinforces the trustworthiness of digital payment solutions.

Types of Digital Wallets and Their Ecosystems

1. Mobile Wallets (Device-Specific)

These are perhaps the most recognized form of digital wallets, deeply integrated into smartphone operating systems. They leverage NFC technology for in-store payments and are often pre-installed or easily accessible on devices.

- Apple Pay: Exclusively for Apple devices (iPhone, Apple Watch, iPad, Mac). It allows users to store credit, debit, loyalty cards, and transit passes. Payments are authorized via Face ID, Touch ID, or passcode. Its tight integration with the Apple ecosystem makes it incredibly seamless for users of Apple products.

- Google Pay: Available on Android devices and accessible via web browsers. It offers similar functionality to Apple Pay, including in-store NFC payments, online payments, and peer-to-peer money transfers. Google Pay also integrates with Google’s broader services, providing loyalty programs and offers.

- Samsung Pay: Unique among mobile wallets due to its support for both NFC and Magnetic Secure Transmission (MST) technology. MST allows Samsung Pay to work with older, non-NFC card readers by emulating a card swipe, giving it wider acceptance in some markets. It’s available on compatible Samsung Galaxy devices.

These mobile wallets prioritize convenience and security, making them ideal for everyday transactions and reducing the need to carry physical cards.

2. Payment Apps (Peer-to-Peer & Online)

These applications primarily focus on facilitating money transfers between individuals (P2P) and often serve as payment gateways for online purchases. While some offer in-store payment options, their strength lies in their versatility for digital transactions.

- PayPal: A pioneer in online payments, PayPal allows users to send and receive money, make online purchases, and often integrates with various e-commerce platforms. It acts as an intermediary, allowing transactions without sharing banking details directly with merchants.

- Venmo: Owned by PayPal, Venmo is popular for its social payment features, allowing users to easily split bills, send money to friends, and make purchases at select online and in-app merchants. Its social feed adds a unique dimension to financial interactions.

- Cash App (Square Cash): A mobile payment service developed by Block, Inc., allowing users to transfer money to one another using a mobile phone app. It also offers a debit card (Cash Card), direct deposit capabilities, and even the ability to buy and sell Bitcoin and stocks.

- Zelle: Integrated directly into many banking apps, Zelle facilitates fast, free P2P transfers between bank accounts within the U.S. It bypasses the need for a separate app for many users, making it exceptionally convenient for bank customers.

These apps are indispensable for managing everyday financial interactions, from splitting restaurant checks to paying rent, and are often a component of effective strategies on How To Create A Monthly Budget by simplifying tracking of various income and expenditure flows.

3. Cryptocurrency Wallets

Distinct from traditional digital wallets, crypto wallets are designed specifically to store the public and private keys required to access and manage cryptocurrencies. They don’t hold the crypto itself (which resides on the blockchain) but provide the interface to interact with it.

- Hot Wallets: Connected to the internet (e.g., exchange wallets, mobile apps, desktop software). They offer convenience for active trading and transactions but are generally considered less secure than cold wallets due to their online exposure.

- Cold Wallets: Offline storage solutions (e.g., hardware wallets, paper wallets). They provide maximum security by keeping private keys disconnected from the internet, ideal for long-term holding of significant crypto assets.

While not directly facilitating fiat currency payments in the same way, the integration of crypto capabilities into broader digital wallet ecosystems is a growing trend, hinting at future financial convergence.

4. Retailer-Specific & In-App Wallets

Many large retailers and service providers have developed their own digital wallet functionalities within their apps. Examples include Starbucks (for paying for coffee and earning rewards), Amazon (for seamless checkout), and airline apps (for boarding passes and in-flight purchases). These are typically designed to enhance loyalty programs and streamline transactions within their specific ecosystem.

The landscape of digital wallets is continuously evolving, with new players and integrations emerging regularly. For Fin3go readers, understanding this diverse ecosystem empowers you to choose the tools that best fit your financial needs and lifestyle, enhancing both convenience and control over your money.

The Myriad Benefits of Embracing Digital Wallets

Beyond the initial novelty, the widespread adoption of digital wallets is driven by a compelling suite of benefits that address key aspects of modern financial life. For individuals seeking efficiency, security, and greater control over their spending, the advantages are clear and significant.

1. Unparalleled Convenience and Speed

The most immediate and apparent benefit of a digital wallet is the sheer convenience it offers.

- Tap-and-Go Payments: In-store purchases become lightning-fast. No fumbling for cards, no swiping, no waiting for chip readers. A quick tap of your phone or watch is often all it takes.

- Online Checkout Simplification: Digital wallets store your payment and shipping details, allowing for one-click or streamlined checkout processes on numerous e-commerce sites and apps, drastically reducing cart abandonment.

- Reduced Clutter: Your physical wallet becomes lighter, freed from the need to carry multiple credit cards, debit cards, and loyalty cards. Your phone is often all you need.

- Accessibility: If you always have your phone, you always have your wallet. This can be a lifesaver if you forget your physical wallet but remember your phone.

2. Enhanced Security Features

As detailed in the mechanics section, digital wallets are designed with multiple layers of security that often surpass the protection offered by traditional physical cards.

- Tokenization: Your actual card number is never transmitted or stored with the merchant, significantly reducing the risk of fraud in the event of a data breach.

- Biometric Authentication: Payments require your fingerprint, face scan, or PIN, meaning even if your phone is stolen, unauthorized users cannot access your funds without your unique biometric data.

- Encryption: All data is encrypted, both at rest and in transit, safeguarding your financial information.

- Remote Wipe Capabilities: In case of loss or theft, many digital wallets allow you to remotely lock or wipe your financial data from your device, providing an immediate layer of protection.

3. Budgeting and Financial Tracking Capabilities

This is where digital wallets truly shine for Fin3go’s audience. Many digital wallet platforms offer integrated tools that can significantly aid in personal financial management.

- Transaction History: Detailed records of all your spending are instantly available within the app, categorized and timestamped.

- Spending Insights: Some wallets provide analytics, breaking down your spending by category (e.g., groceries, entertainment, transport), helping you visualize where your money goes. This functionality is invaluable when you’re learning How To Create A Monthly Budget, as it provides real-time data to inform your financial planning.

- Integration with Budgeting Apps: Many digital wallets can sync with dedicated budgeting software, further enhancing your ability to track expenses, set limits, and stay on top of your financial goals.

4. Rewards, Loyalty Programs, and Offers

Digital wallets often integrate seamlessly with loyalty programs and offer exclusive deals.

- Digital Loyalty Cards: Store all your loyalty cards digitally, ensuring you never miss out on points or rewards. Some wallets even automatically apply loyalty points at checkout.

- Exclusive Deals: Many platforms offer cashback, discounts, or special promotions when you pay using their digital wallet, providing tangible savings.

5. Streamlined International Payments and Transfers

For those who travel or conduct international business, digital wallets can simplify cross-border transactions, often offering competitive exchange rates and lower fees compared to traditional banking methods. This makes managing finances across different currencies much more accessible and transparent.

In essence, embracing a digital wallet is not just about adopting a new technology; it’s about upgrading your entire financial interaction. It offers a powerful combination of security, convenience, and insightful tools that can transform how you manage, spend, and understand your money, aligning perfectly with Fin3go’s mission to empower smarter financial decisions.

Navigating the Challenges and Considerations of Digital Wallets

While the benefits of digital wallets are compelling, a balanced perspective requires acknowledging the potential challenges and considerations. For Fin3go readers, understanding these aspects is vital for making informed decisions and mitigating potential downsides.

1. Dependency on Technology and Battery Life

The very strength of digital wallets—their integration with smart devices—is also a potential vulnerability.

- Battery Dependency: A dead phone battery means a dead wallet. If your device runs out of power, you lose access to your payment methods, which can be particularly inconvenient in critical situations.

- Device Malfunctions: Technical glitches, software updates, or hardware failures can temporarily or permanently disrupt access to your digital wallet, leaving you without a payment option.

- Internet Connectivity: While NFC payments often don’t require an active internet connection, many digital wallet features, such as peer-to-peer transfers, loading new cards, or accessing detailed transaction histories, do.

2. Acceptance Limitations

Despite growing adoption, digital wallets are not universally accepted.

- Merchant Infrastructure: Smaller businesses, older payment terminals, or establishments in certain regions may not have NFC-enabled terminals or accept specific digital payment apps. This necessitates carrying a backup physical card or cash.

- Regional Disparities: Acceptance rates can vary significantly by country and even within cities, making it important to research local payment norms when traveling.

3. Data Privacy and Security Concerns (Beyond Tokenization)

While tokenization protects your card numbers, other privacy concerns can arise.

- Personal Data Collection: Digital wallet providers collect vast amounts of transactional data, including where, when, and what you purchase. While often anonymized for analytics, the sheer volume of this data raises privacy questions about how it’s used, shared, and protected.

- Device Security: The security of your digital wallet is intrinsically linked to the security of your device. A compromised smartphone (e.g., through malware or inadequate device security practices) could potentially expose your wallet data, even with biometrics.

4. Risk of Overspending and Financial Discipline

The ease and speed of digital payments can, for some individuals, lead to less conscious spending.

- Reduced Tangibility of Money: The act of handing over physical cash creates a tangible connection to the money being spent. Digital transactions, being invisible and instantaneous, can sometimes detach individuals from the reality of their spending, potentially leading to impulsive purchases.

- Seamlessness and Speed: While a benefit, this can also be a pitfall for those struggling with financial discipline. The lack of friction in transactions can make it easier to overspend without realizing the cumulative impact. For Fin3go readers, this underscores the importance of having a robust financial strategy, whether it’s diligently following How To Create A Monthly Budget or applying strategies like the Snowball Vs Avalanche Debt Payoff Method to manage existing debt effectively. Digital wallets are tools; their benefit depends on the user’s financial habits.

5. Potential for Vendor Lock-in

Relying heavily on one specific digital wallet ecosystem (e.g., exclusively Apple Pay or Google Pay) can create a degree of vendor lock-in, making it harder to switch devices or platforms without some inconvenience in transferring payment methods and loyalty programs.

By being aware of these challenges, Fin3go readers can adopt digital wallets responsibly, implementing strategies like carrying a backup payment method, regularly reviewing transaction histories, and maintaining strong device security to maximize the benefits while minimizing the risks.

Digital Wallets and the Future of Personal Finance

The journey of the digital wallet is far from over; it stands at the precipice of even more profound transformations that will redefine personal finance. As technology continues to evolve at an exponential pace, digital wallets are poised to become not just payment tools but central command centers for our entire financial lives.

1. Enhanced Integration with AI and Personalized Financial Advice

The vast amounts of transaction data collected by digital wallets present an incredible opportunity for artificial intelligence (AI). Future digital wallets will likely:

- Offer Hyper-Personalized Budgeting: Moving beyond simple categorization, AI could analyze spending patterns, predict future expenses, and proactively suggest adjustments to your How To Create A Monthly Budget in real-time.

- Automated Savings and Investments: AI-powered features could identify surplus funds and automatically transfer them to savings accounts or micro-investment platforms, optimizing your financial growth without manual intervention.

- Proactive Financial Health Checks: The wallet could alert you to potential overspending trends, suggest strategies to tackle debt (perhaps even recommending the Snowball Vs Avalanche Debt Payoff Method based on your financial profile), and identify opportunities for better financial management.

2. Expansion into Decentralized Finance (DeFi) and Cryptocurrency

While some digital wallets already offer basic crypto features, the integration with DeFi is set to deepen.

- Seamless Crypto Transactions: Expect easier buying, selling, and spending of cryptocurrencies directly from your primary digital wallet, bridging the gap between traditional fiat and digital assets.

- DeFi Access: Digital wallets could become gateways to decentralized lending, borrowing, and staking protocols, allowing users to earn interest on their crypto holdings or participate in other DeFi services. This opens up new avenues for Passive Income Ideas 2026 for the technologically savvy investor.

- NFT Integration: Storing and showcasing non-fungible tokens (NFTs) could become a standard feature, alongside payment methods and loyalty cards.

3. Digital Identities and Credentials

The concept of a “digital wallet” is expanding beyond just financial instruments.

- Digital IDs: Many governments are exploring integrating digital driver’s licenses, national ID cards, and health insurance information into secure digital wallets, offering a single, authenticated source for personal identification.

- Credential Management: University degrees, professional certifications, and even vaccination records could be securely stored and presented via digital wallets, streamlining verification processes.

4. Adoption of Central Bank Digital Currencies (CBDCs)

As central banks worldwide research and pilot their own digital currencies, digital wallets will be the primary interface for consumers to hold and transact with CBDCs. This could fundamentally alter payment systems, offering new levels of financial inclusion and direct access to central bank money.

5. Cross-Border Payments and Remittances

Digital wallets are set to revolutionize international money transfers, making them faster, cheaper, and more transparent. Blockchain technology, combined with digital wallet interfaces, could significantly reduce the friction and costs associated with remittances, benefiting global economies and individual users.

The future of digital wallets points towards a highly personalized, integrated, and intelligent financial ecosystem. For Fin3go readers, staying abreast of these developments means being empowered to leverage the most advanced tools for wealth management, income generation (like exploring new Passive Income Ideas 2026), and ensuring robust financial health in an increasingly digital world. The digital wallet isn’t just a trend; it’s the future of how we interact with our money and our identities.

Frequently Asked Questions

Recommended Resources

Learn more about this topic in How To Invest Money For Beginners at AssetBar.

Learn more about this topic in How To Write A Business Proposal at Page Release.