In the dynamic landscape of personal finance, individuals are increasingly faced with a critical decision: how to best manage their investments and navigate their financial future. Two prominent paths have emerged, each offering distinct advantages and catering to different needs: the traditional financial advisor and the modern robo-advisor. For many, the choice between human expertise and algorithmic efficiency is far from straightforward. This comprehensive guide from Fin3go delves deep into the nuances of robo advisor vs financial advisor, dissecting their methodologies, benefits, drawbacks, and ultimately, helping you determine which approach aligns best with your financial goals, personal preferences, and investment philosophy.

Understanding the Traditional Financial Advisor: The Human Touch in Wealth Management

A traditional financial advisor is a licensed professional who provides personalized financial guidance and investment management services. They typically work with clients one-on-one, building long-term relationships based on trust and a deep understanding of the client’s unique circumstances. Their role extends far beyond merely recommending investments; they act as a comprehensive financial planner, strategist, and often, a behavioral coach.

What Services Do Traditional Financial Advisors Offer?

- Holistic Financial Planning: This is the cornerstone of their service. Advisors help you set financial goals (e.g., retirement, buying a home, funding education), assess your current financial situation, and create a detailed roadmap to achieve those goals. This often includes estate planning, tax planning, insurance analysis, and budgeting advice.

- Personalized Investment Management: Based on your risk tolerance, time horizon, and objectives, they construct and manage a diversified investment portfolio. This involves asset allocation, fund selection, rebalancing, and ongoing performance monitoring.

- Behavioral Coaching: Perhaps one of their most invaluable contributions is helping clients avoid emotionally driven investment decisions during market volatility. They provide a steady hand, preventing impulsive reactions that could derail long-term plans.

- Complex Financial Situations: For individuals with intricate financial lives—such as business owners, high-net-worth individuals, or those facing significant life changes like divorce or inheritance—a traditional advisor can offer tailored strategies and navigate complex regulations.

- Debt Management Strategies: While not their primary focus, many advisors will integrate debt management into your overall financial plan. They can discuss strategies like the Snowball Vs Avalanche Debt Payoff Method and help you determine which approach aligns best with your financial personality and goals, freeing up capital for investment.

How Are Traditional Financial Advisors Compensated?

Compensation structures for traditional advisors vary, impacting the overall cost to the client:

- Fee-Only: These advisors are paid directly by their clients, typically as a percentage of assets under management (AUM), an hourly rate, or a flat fee for specific services. This structure is generally preferred as it minimizes conflicts of interest.

- Commission-Based: These advisors earn commissions from the financial products they sell, such as mutual funds, annuities, or insurance policies. This can create potential conflicts of interest, as their recommendations might be influenced by the commission they stand to earn.

- Fee-Based: A hybrid model where advisors may charge fees for advice but also earn commissions from product sales. It’s crucial to understand the specific fee structure before engaging their services.

Typical fees for AUM can range from 0.5% to 1.5% annually, depending on the advisor’s services, experience, and the amount of assets managed. While seemingly small, these fees can add up significantly over time.

When is a Traditional Financial Advisor the Right Choice?

You might benefit most from a human advisor if:

- You have a complex financial situation (e.g., high net worth, multiple income streams, business ownership, significant inheritance).

- You prefer personalized, face-to-face interaction and value the human element of advice.

- You need comprehensive financial planning beyond just investment management.

- You’re prone to emotional investing and need a professional to keep you on track.

- You require guidance on estate planning, tax optimization, or charitable giving.

Demystifying the Robo-Advisor: The Power of Algorithmic Investing

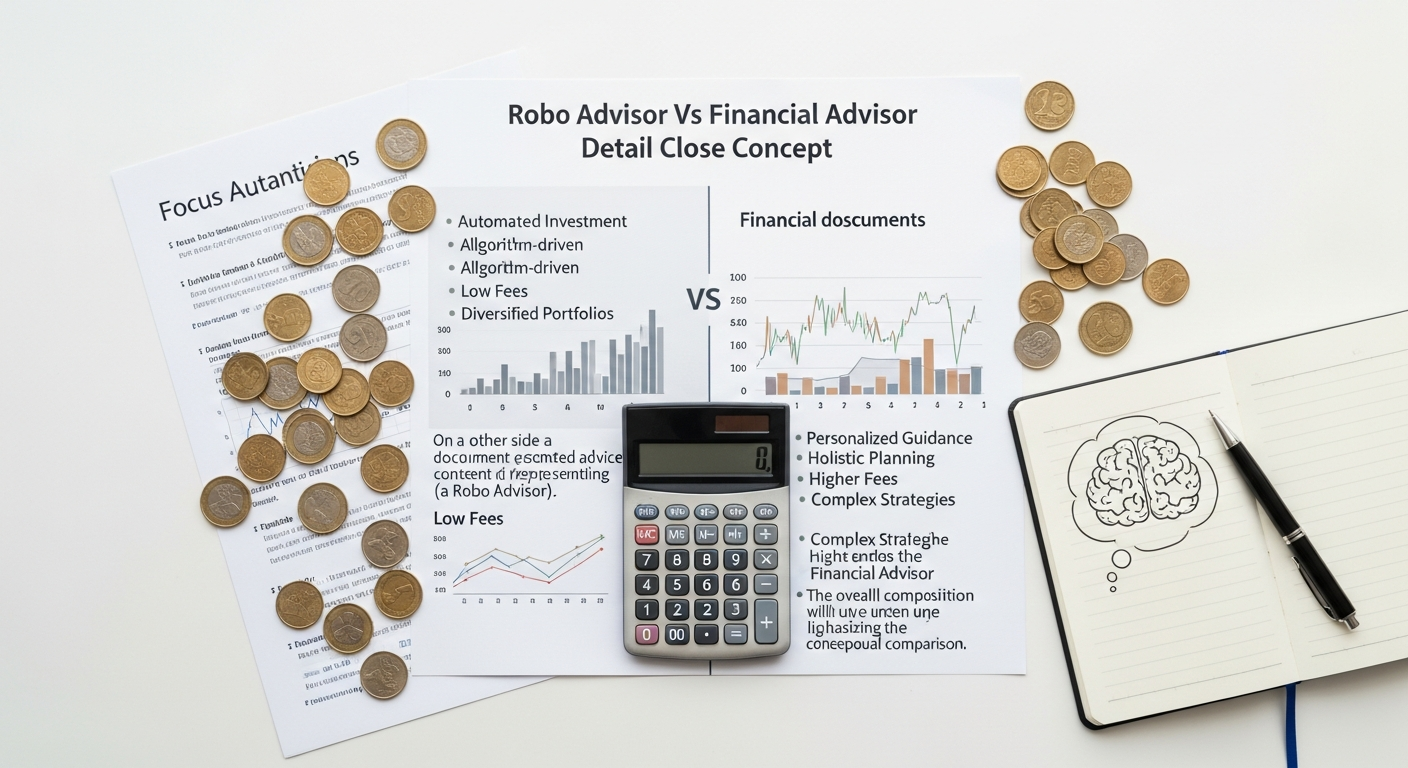

Robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with little to no human intervention. They leverage sophisticated software to build and manage diversified investment portfolios based on your stated financial goals, risk tolerance, and time horizon. Since their emergence, robo-advisors have revolutionized access to investment management, making it more affordable and accessible to a broader audience.

How Do Robo-Advisors Work?

The process typically begins with an online questionnaire designed to assess your financial situation, investment objectives, and comfort level with risk. Based on your responses, the algorithm recommends a suitable portfolio, usually composed of low-cost exchange-traded funds (ETFs) or mutual funds. Once funded, the robo-advisor automates several key investment functions:

- Portfolio Construction: Diversified portfolios tailored to your risk profile.

- Automatic Rebalancing: The platform regularly adjusts your portfolio to maintain its target asset allocation, ensuring it doesn’t drift too far from your initial strategy.

- Tax-Loss Harvesting: Many robo-advisors offer this feature, which involves selling investments at a loss to offset capital gains and ordinary income, potentially reducing your tax bill.

- Dividend Reinvestment: Automatically reinvesting dividends back into your portfolio to accelerate growth through compounding.

- Goal-Based Planning: While less comprehensive than a human advisor, many platforms allow you to set specific goals (e.g., retirement, down payment) and track progress.

Cost Structure of Robo-Advisors

One of the most compelling advantages of robo-advisors is their cost-effectiveness. Fees are typically a small percentage of assets under management (AUM), often ranging from 0.15% to 0.50% annually. This is significantly lower than traditional advisors. Additionally, the underlying ETFs chosen by robo-advisors usually have very low expense ratios, further reducing the overall cost of investing.

When is a Robo-Advisor the Right Choice?

A robo-advisor might be an excellent fit if:

- You’re a beginner investor looking for a simple, low-cost way to start.

- You have a relatively straightforward financial situation.

- You prefer a hands-off, automated approach to investing.

- You are comfortable with digital platforms and minimal human interaction.

- You want to keep investment management fees as low as possible.

- You are disciplined and don’t require emotional coaching during market fluctuations.

- You’ve already mastered How To Create A Monthly Budget and have a clear understanding of your disposable income available for investing.

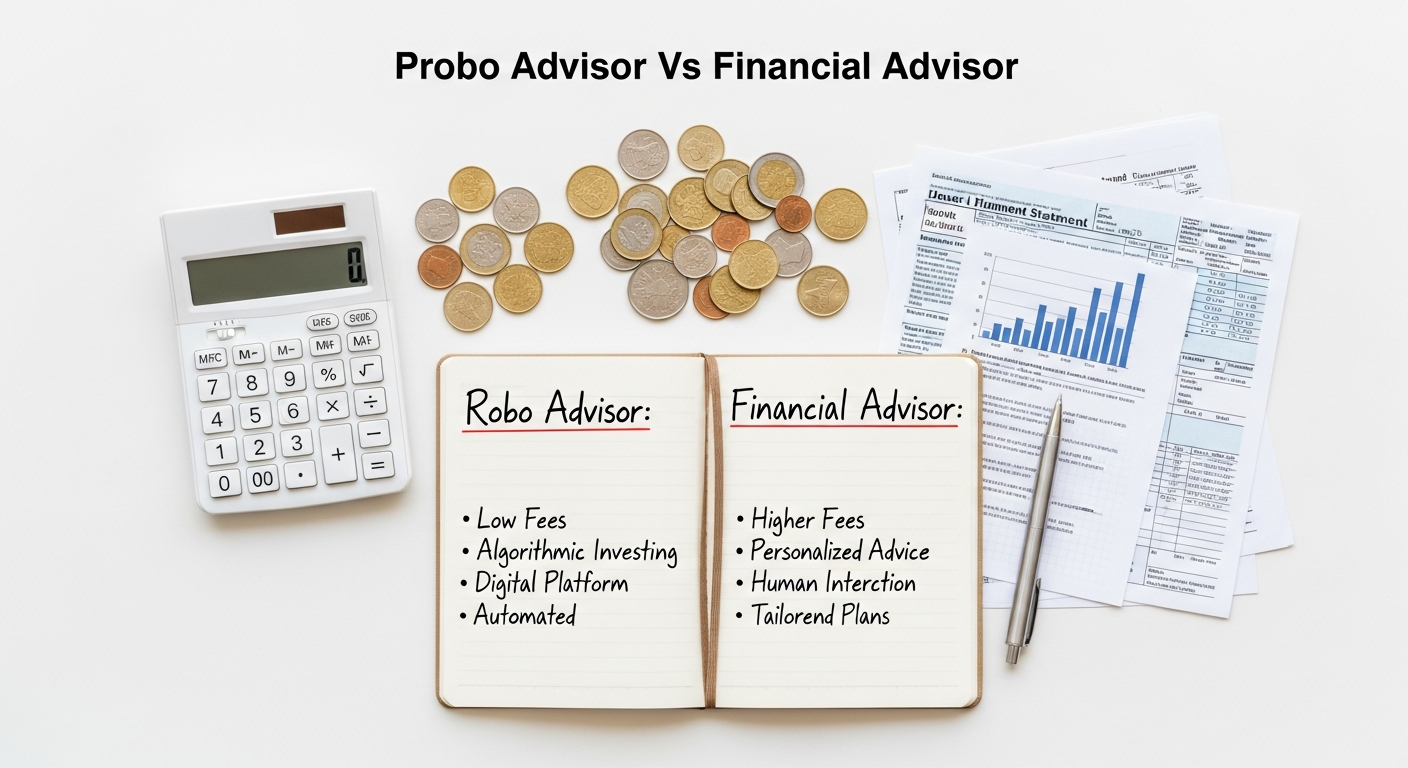

Key Differences: Robo Advisor vs Financial Advisor – A Side-by-Side Comparison

While both robo-advisors and traditional financial advisors aim to help you grow your wealth, their approaches, services, and costs differ significantly. Understanding these distinctions is crucial for making an informed decision.

Personalization and Human Interaction

- Traditional Financial Advisor: Offers a highly personalized experience. They get to know you, your family, your aspirations, and your fears. This human connection allows for nuanced advice, empathy during tough times, and the ability to adapt strategies to highly specific, evolving life events. They can help you plan for unique scenarios like funding a special needs trust or navigating complex business succession.

- Robo-Advisor: Provides standardized portfolios based on algorithms. While the initial questionnaire personalizes your risk profile, the advice is generic. There’s minimal to no human interaction, which can be a drawback for those who prefer guidance and reassurance from a person, especially during market downturns. The advice is limited to investment selection and rebalancing; complex financial situations are generally beyond their scope.

Scope of Services

- Traditional Financial Advisor: Offers a broad spectrum of services encompassing comprehensive financial planning: retirement planning, estate planning, tax planning, insurance needs analysis, budgeting, debt strategies, and even guidance on charitable giving. They look at your entire financial picture.

- Robo-Advisor: Primarily focuses on automated investment management. Some platforms offer basic goal-setting tools or access to human advisors for an additional fee (hybrid models), but they generally don’t provide the in-depth, holistic financial planning that a traditional advisor does. They won’t help you draft a will or strategize complex tax deductions.

Cost and Accessibility

- Traditional Financial Advisor: Generally more expensive, with fees typically ranging from 0.5% to 1.5% of AUM annually, or hourly/flat fees. Many also have minimum asset requirements, often starting at $100,000 or more, making them less accessible to new investors or those with smaller portfolios.

- Robo-Advisor: Significantly more affordable, with fees typically between 0.15% and 0.50% of AUM. Minimum investment requirements are often very low, sometimes as little as $0 or $100, making them highly accessible to virtually anyone looking to start investing.

Emotional and Behavioral Support

- Traditional Financial Advisor: Acts as a behavioral coach, providing emotional support and preventing clients from making impulsive, fear-driven decisions during market downturns or greed-driven decisions during booms. This guidance can be invaluable in sticking to a long-term plan.

- Robo-Advisor: Offers no emotional or behavioral coaching. While the automation helps remove human emotion from the investment process itself, it doesn’t prevent an investor from panicking and withdrawing funds manually during a downturn, potentially harming their long-term returns.

Tax Efficiency

- Traditional Financial Advisor: Can offer highly personalized tax planning strategies, integrating investment decisions with your overall tax situation, income, and deductions to maximize after-tax returns. This includes complex tax-loss harvesting strategies specific to your holdings and other financial assets.

- Robo-Advisor: Many offer automated tax-loss harvesting, which can be effective for straightforward portfolios. However, they generally don’t provide broader tax planning advice that considers your entire financial profile, such as income tax, estate tax, or capital gains from external investments.

The Hybrid Approach: Getting the Best of Both Worlds

Recognizing the strengths of both human and digital advice, a growing number of platforms and advisors are offering a hybrid model. These services combine the low-cost, automated investment management of a robo-advisor with occasional access to a human financial advisor for personalized advice. This can be an ideal solution for those who appreciate automation but still want the option of human interaction for more complex questions or reassurance.

How Hybrid Models Work

Typically, a hybrid model involves:

- Automated portfolio management (like a standard robo-advisor).

- Access to certified financial planners (CFPs) via phone, video call, or email for specific questions or annual reviews.

- Fees that are usually higher than pure robo-advisors but lower than traditional financial advisors (e.g., 0.35% to 0.80% of AUM).

- Minimum investment requirements that fall between pure robo and traditional advisors.

Who Benefits from a Hybrid Approach?

The hybrid model is well-suited for:

- Investors with growing assets who are outgrowing basic robo-advisor services but aren’t ready for a full-service traditional advisor.

- Individuals who want a cost-effective solution but still value the safety net of human expertise.

- Those who have specific, occasional questions about retirement planning, college savings, or major life events, but don’t need ongoing, comprehensive planning.

- People exploring Passive Income Ideas 2026 and want some expert input on how to integrate these into their overall financial strategy without committing to a high-cost advisor.

Making Your Decision: A Framework for Choosing Your Financial Partner

The choice between a robo-advisor and a traditional financial advisor is deeply personal and depends on a multitude of factors. There’s no single “best” option; rather, it’s about finding the solution that best fits your current financial situation, future goals, and personal preferences.

Assess Your Financial Complexity

Start by evaluating the complexity of your financial life. Do you have:

- Multiple income streams or business ventures?

- Significant assets spread across various accounts?

- Specific estate planning needs (e.g., trusts, beneficiaries with special needs)?

- Complex tax situations (e.g., stock options, rental properties, self-employment)?

- Major life transitions on the horizon (e.g., marriage, divorce, inheritance, retirement)?

If you answered yes to several of these, a traditional financial advisor or a hybrid model offering substantial human interaction might be more appropriate. For simpler situations, a robo-advisor could suffice.

Consider Your Investment Knowledge and Confidence

- High Confidence / Knowledge: If you’re comfortable with investment concepts, understand risk, and can maintain discipline during market volatility, a robo-advisor can be a powerful, low-cost tool.

- Low Confidence / Knowledge: If you’re new to investing, easily swayed by market news, or simply prefer to delegate the decision-making, a traditional advisor can provide the education, reassurance, and expertise you need.

Evaluate Your Need for Comprehensive Planning

Are you looking for just investment management, or do you need help with your entire financial ecosystem?

- Investment Focus: If your primary need is to build a diversified portfolio and have it automatically managed at a low cost, a robo-advisor is a strong contender.

- Holistic Planning: If you need guidance on budgeting (How To Create A Monthly Budget is a fundamental step), debt management (like choosing between Snowball Vs Avalanche Debt Payoff Method), retirement projections, insurance analysis, and strategies for achieving diverse financial goals, a traditional advisor offers unparalleled breadth.

Determine Your Budget for Financial Advice

Your available budget will naturally influence your choice.

- Cost-Sensitive: Robo-advisors are the most economical choice, making professional investment management accessible even with small starting balances.

- Value-Oriented: If you recognize the value of personalized, comprehensive advice and have the assets to justify the fees, a traditional advisor can offer significant long-term value, potentially saving you more in taxes or preventing costly mistakes than their fees.

Consider Your Preference for Interaction

Do you prefer digital interaction or a personal relationship?

- Digital Native: If you’re comfortable managing most aspects of your life online and prefer the convenience of digital platforms, a robo-advisor is a natural fit.

- Human Connection:

- If you value direct communication, face-to-face meetings, and a trusted advisor who knows your story, then a traditional financial advisor is your preference.

Conclusion: Your Path to Financial Well-being

The debate of robo advisor vs financial advisor isn’t about one being inherently superior to the other. Instead, it’s about aligning the right tool with your specific needs, preferences, and financial stage. Robo-advisors have democratized investing, offering efficient, low-cost portfolio management for a wide audience. Traditional financial advisors, on the other hand, provide invaluable personalized advice, holistic planning, and crucial emotional support for those with complex financial lives or a desire for a human connection.

As your financial journey evolves, so too might your needs. A young investor starting with a small portfolio might thrive with a robo-advisor. As their wealth grows, their financial situation becomes more complex, or they begin exploring advanced strategies like incorporating Passive Income Ideas 2026 into their portfolio, they might transition to a hybrid model or a full-service human advisor. The key is to regularly assess your financial landscape and choose a partner that empowers you to achieve your financial aspirations effectively and confidently.

Frequently Asked Questions About Robo Advisors vs Financial Advisors

Q1: Can I use both a robo-advisor and a traditional financial advisor?

A1: Yes, absolutely. Many individuals choose a hybrid approach, or even use both services for different purposes. For instance, you might use a robo-advisor for a straightforward retirement account and a traditional advisor for complex estate planning or business financial advice. Some traditional advisors might even use robo-advisor platforms for managing parts of their clients’ portfolios, offering the best of both worlds.

Q2: Are robo-advisors safe and regulated?

A2: Yes, reputable robo-advisors are regulated by the U.S. Securities and Exchange Commission (SEC) and are members of the Securities Investor Protection Corporation (SIPC), which protects your investments up to $500,000 in case the firm fails. While your investment value can fluctuate with market conditions, the safety of your assets held by the platform is generally assured.

Q3: How do I find a good traditional financial advisor?

A3: Look for a fee-only, fiduciary advisor who is legally bound to act in your best interest. Credentials like Certified Financial Planner (CFP®) are a strong indicator of expertise. You can find advisors through organizations like the National Association of Personal Financial Advisors (NAPFA) or the CFP Board’s “Find a CFP Professional” tool. Always interview several advisors to ensure a good fit.

Q4: What’s the minimum investment for a traditional financial advisor versus a robo-advisor?

A4: Traditional financial advisors often have minimum asset requirements, typically starting from $100,000 to $500,000, though some may work with lower amounts for a higher flat fee. Robo-advisors, conversely, are known for their low minimums, with many platforms requiring as little as $0 or $100 to start investing, making them highly accessible for new investors.

Q5: Can a robo-advisor help me with budgeting and debt payoff strategies?

A5: Pure robo-advisors typically focus solely on investment management and do not offer personalized advice on budgeting or specific debt payoff strategies like the Snowball Vs Avalanche Debt Payoff Method. Some hybrid platforms might offer basic tools or limited access to a human advisor for such questions. For in-depth guidance on How To Create A Monthly Budget and comprehensive debt strategies, a human financial advisor is generally a better resource.

Q6: If I start with a robo-advisor, can I switch to a traditional advisor later?

A6: Yes, you absolutely can. As your wealth grows and your financial situation becomes more complex, you might find that the comprehensive services of a traditional financial advisor become more appealing. Many investors start with a robo-advisor and transition to a human advisor once their portfolio reaches a certain size or their planning needs become more intricate. The process of transferring assets between institutions is generally straightforward.

Recommended Resources

You might also enjoy How To Build An Online Community For Your Brand from Kacerr.

Learn more about this topic in Shopify Vs Woocommerce Which Is Better at E-ComProfits.