Why a Separate Business Bank Account is Non-Negotiable for Every Entrepreneur

For many new business owners, especially sole proprietors or those just starting with online business ideas you can start with no money, the temptation to simply use a personal bank account for business transactions can be strong. It seems easier, less complicated, and perhaps even cost-saving initially. However, succumbing to this temptation is a common pitfall that can lead to a host of problems down the line. A dedicated business bank account is not merely a convenience; it’s a critical component of sound financial management and legal prudence. Let’s delve into why this separation is absolutely essential.

Legal Protection and Liability Shield

- Maintaining the Corporate Veil: If your business is structured as an LLC (Limited Liability Company), Corporation, or Partnership, one of the primary benefits is limited personal liability. This means your personal assets are typically protected from business debts and lawsuits. Mixing personal and business finances, a practice known as “commingling,” can legally blur the lines between you and your business. Should your business face legal challenges, a court might “pierce the corporate veil,” holding you personally responsible for business liabilities. A separate business account helps demonstrate that your business is a distinct legal entity, reinforcing this crucial liability shield.

- Audit Preparedness: The IRS (Internal Revenue Service) takes a keen interest in how businesses manage their finances. In the unfortunate event of an audit, having a clear separation between personal and business transactions simplifies the process immensely. Auditors can quickly see that business funds are used solely for business purposes, reducing scrutiny and potential penalties. Without this separation, every personal transaction on a mixed account could be subject to intense review, turning an audit into a much more arduous and stressful ordeal.

Streamlined Financial Management and Accounting

- Simplified Bookkeeping: Imagine sifting through hundreds of transactions on a single bank statement, trying to discern which ones are business-related and which are personal. It’s a nightmare scenario for bookkeeping. A dedicated business account ensures that every entry is directly tied to your company’s operations, making reconciliation, expense tracking, and income categorization straightforward. This clarity is invaluable for accurate financial reporting and making informed business decisions.

- Easier Tax Preparation: Tax season is stressful enough without having to untangle commingled finances. With a business account, all your deductible expenses, revenue, and payroll are neatly organized. This makes filing your business taxes much simpler, reducing the time and effort required, and minimizing the risk of errors that could lead to penalties. Your accountant will thank you, and you’ll save on accounting fees.

- Clear Financial Reporting: To grow your business, you need a clear picture of its financial health. A business bank account provides the data necessary to generate accurate profit and loss statements, balance sheets, and cash flow reports. These reports are vital for understanding your business’s performance, identifying trends, and making strategic decisions about investments, pricing, and expansion.

Professionalism and Credibility

- Projecting a Professional Image: Paying vendors, receiving payments from clients, and issuing payroll from a business-branded account conveys professionalism. It signals that you are serious about your venture and operate as a legitimate entity, building trust with clients, suppliers, and potential investors. Imagine trying to secure a major contract and asking the client to pay your personal checking account – it simply doesn’t inspire confidence.

- Access to Business Services: Most banks offer specialized services tailored for businesses, such as business credit cards, lines of credit, merchant services for processing customer payments, and payroll solutions. You can only access these crucial tools, which are vital for scaling operations, if you have a formal business banking relationship. Furthermore, establishing a positive banking relationship now can pave the way for easier access to loans and financing options when your business needs capital for growth.

- Attracting Investors and Partners: If you ever plan to seek investment or take on business partners, a separate, well-managed business bank account is non-negotiable. Investors and partners want to see clear financial records and a professional operation. Commingled finances are a major red flag that suggests a lack of seriousness and poor financial management, making your business far less attractive.

In essence, opening a business bank account is a foundational step towards legitimacy, efficiency, and long-term success. It’s an investment in your peace of mind and your business’s future, ensuring you maintain control and clarity over your financial landscape.

Choosing the Right Business Bank: Factors to Consider

Once you understand the absolute necessity of a business bank account, the next crucial step is deciding where to open one. The financial landscape is diverse, offering a wide array of options from traditional brick-and-mortar institutions to cutting-edge online-only banks. Making the right choice involves carefully considering your business’s specific needs, your operational style, and your long-term financial goals. This decision can significantly impact your daily operations, your expenses, and your ability to manage your money effectively.

Traditional Banks vs. Online Banks: A Fin3go Perspective

The first major fork in the road is deciding between a traditional bank and a modern online-only institution. This is where the Fin3go article “Which online bank is right for you” can provide excellent supplementary reading, as many of the considerations for personal online banking also apply to business accounts.

- Traditional Banks (e.g., Chase, Bank of America, Wells Fargo):

- Pros: Physical branches for in-person deposits (especially cash), face-to-face customer service, extensive ATM networks, a full suite of business services (loans, lines of credit, merchant services), and often a personal relationship with a business banker. This can be reassuring for businesses that handle a lot of cash or prefer direct interaction.

- Cons: Often higher fees (monthly maintenance, transaction fees), stricter requirements for fee waivers, potentially less user-friendly online interfaces compared to fintech challengers, and slower adoption of new technologies.

- Online Banks (e.g., Bluevine, Novo, Mercury):

- Pros: Generally lower or no monthly fees, higher interest rates on balances, robust mobile apps and online platforms, seamless integration with accounting software (like QuickBooks or Xero), modern features, and often 24/7 digital customer support. They are ideal for businesses that primarily conduct transactions digitally, don’t handle much cash, and appreciate technological efficiency. Many online business ideas you can start with no money find these options particularly appealing due to their low overhead.

- Cons: No physical branches for cash deposits (often rely on third-party networks like Allpoint or Green Dot, which may incur fees), less personal interaction, and potentially fewer complex financial products like large business loans (though this is rapidly changing).

Your choice here largely depends on your business model. A retail store with daily cash transactions might lean towards a traditional bank, while a freelance designer or an e-commerce store might find an online bank more suitable and cost-effective.

Key Factors to Evaluate Before Deciding

Beyond the online vs. traditional debate, several other factors demand your attention:

- Fees and Minimum Balances: This is paramount. Scrutinize monthly service fees, transaction fees (for deposits, withdrawals, transfers, wire transfers), ATM fees, overdraft fees, and any fees for exceeding transaction limits. Many banks offer ways to waive monthly fees, often by maintaining a minimum daily balance or meeting certain transaction volume requirements. Understand these thoroughly to avoid unexpected costs.

- Services Offered: What specific features does your business need?

- Merchant Services: If you accept credit card payments, does the bank offer integrated merchant accounts or partnerships with payment processors?

- Online and Mobile Banking: A strong, intuitive online platform and mobile app are crucial for managing your finances on the go, especially for modern businesses. Look for features like mobile check deposit, bill pay, and robust security.

- Integrations: Does the bank integrate seamlessly with your accounting software (e.g., QuickBooks, Xero)? This can save countless hours in bookkeeping and reconciliation.

- Payroll Services: If you plan to hire employees, does the bank offer or partner with payroll solutions?

- Lending Options: Consider their offerings for business loans, lines of credit, and SBA loans if you anticipate needing financing for growth.

- Customer Service: How accessible and responsive is their customer support? Check reviews for their ability to resolve issues quickly and efficiently. Do they offer dedicated business banking specialists?

- ATM and Branch Access: Even if you choose an online bank, consider their ATM network. For traditional banks, assess the convenience of their branch locations relative to your business.

- Scalability: As your business grows, will your chosen bank be able to meet your evolving needs? Consider if they offer higher-tier accounts or more sophisticated financial products that you might require in the future.

- User Reviews and Reputation: Leverage online reviews (Google, Trustpilot, industry-specific forums) to get a sense of other business owners’ experiences with the bank’s services, fees, and customer support.

By meticulously evaluating these factors, you can confidently select a business bank that aligns with your operational realities and supports your financial aspirations. Taking the time upfront to research and compare options will save you headaches and money in the long run, ensuring your banking partner is a true asset to your business.

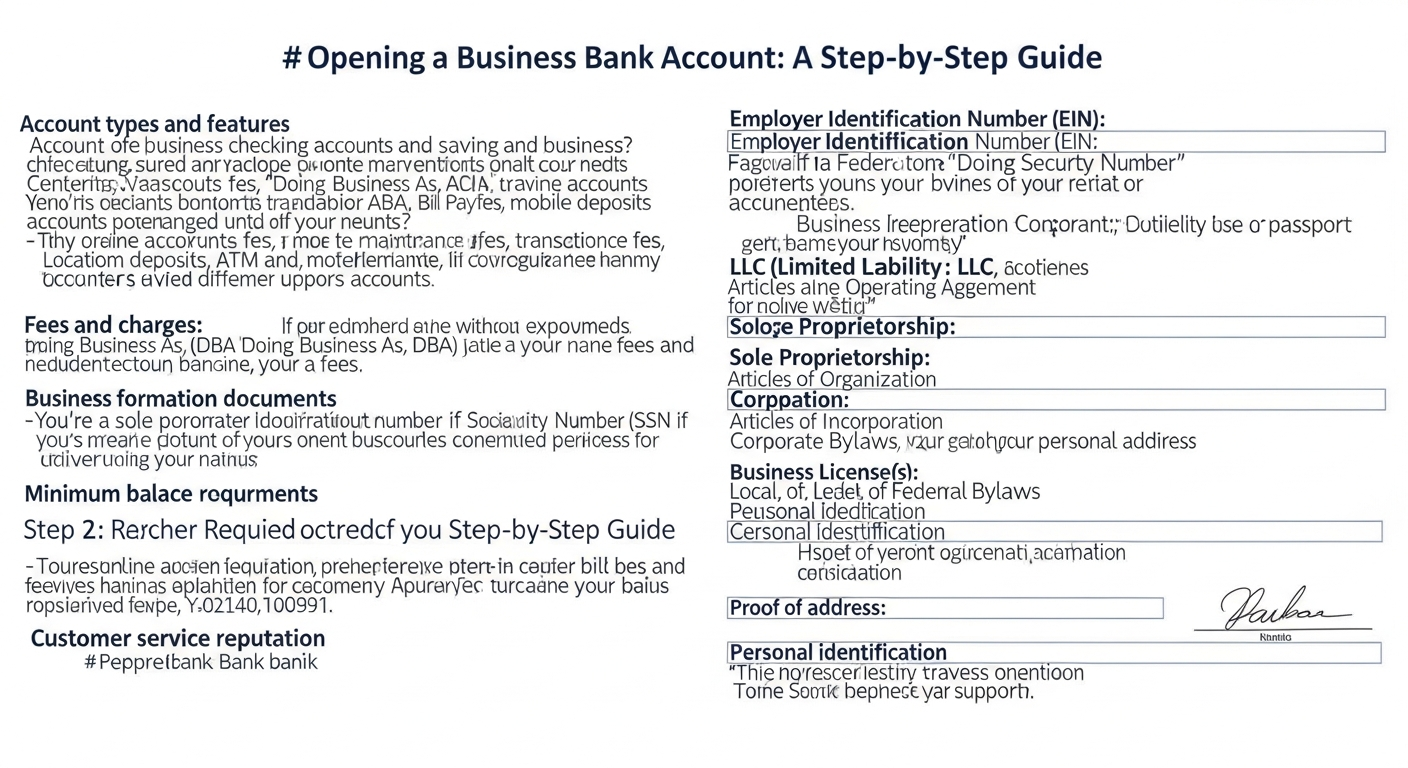

Gathering Your Essential Documents: The Pre-Application Checklist

Universal Requirements for All Business Types

Regardless of your business structure, there are a few foundational documents and pieces of information you will almost certainly need:

- Employer Identification Number (EIN): This is a unique nine-digit tax ID number assigned by the IRS to businesses, much like a Social Security Number for individuals. It’s required for most business structures (LLCs, Corporations, Partnerships, and Sole Proprietors with employees). You can obtain an EIN for free directly from the IRS website. It takes only a few minutes to apply online and receive it instantly.

- Personal Identification: The bank will need to verify the identity of all individuals who will be signatories on the account. This typically includes:

- Government-issued photo ID (e.g., driver’s license, passport, state ID).

- Social Security Number (SSN) for each authorized signer.

- Proof of address (e.g., utility bill, lease agreement, or another official document showing your current residential address).

- Business Name and Address: Your official business name (as registered with the state, if applicable) and your primary business address.

- Business Phone Number and Email Address: Contact information specific to your business.

- Description of Business Activities: A brief overview of what your business does, its industry, and its primary source of income.

Documents Required Based on Business Structure

The specific legal structure of your business dictates additional documentation you’ll need to provide. Banks require these to confirm your business’s legitimacy and the authority of the individuals opening the account.

Sole Proprietorship or DBA (Doing Business As)

If you’re operating as a sole proprietorship, perhaps running one of the many online business ideas you can start with no money, and haven’t formally registered your business with the state beyond a “Doing Business As” (DBA) name, the requirements are simpler:

- Fictitious Business Name Statement (DBA): If you operate under a name other than your legal personal name, you’ll need proof of your DBA registration, usually filed with your county or state.

- Business License (if applicable): Depending on your industry and location, you might need a local, state, or federal business license.

Note: Even as a sole proprietor, getting an EIN is often recommended, especially if you plan to hire employees or want to keep your SSN more private on business documents.

Limited Liability Company (LLC)

LLCs require more formal documentation to establish their legal existence:

- Articles of Organization (or Certificate of Formation): This document is filed with your state’s Secretary of State (or equivalent office) to legally create your LLC.

- Operating Agreement: While not always legally required in all states, an operating agreement is crucial. It outlines the ownership structure, management responsibilities, and operational procedures of your LLC. Banks often request it to confirm who has the authority to open and manage the account.

- EIN Confirmation Letter (SS-4): The official letter from the IRS confirming your business’s EIN.

Corporation (S-Corp, C-Corp)

Corporations have the most extensive documentation requirements due to their complex structure:

- Articles of Incorporation: Filed with your state to legally establish the corporation.

- Corporate Bylaws: These internal documents outline the corporation’s rules, regulations, and operational procedures, including how officers are appointed and who has signatory authority.

- Corporate Resolution: A formal document, often included in the meeting minutes of the board of directors, that authorizes specific individuals (e.g., President, Treasurer) to open and manage bank accounts on behalf of the corporation.

- EIN Confirmation Letter (SS-4): The official letter from the IRS confirming your business’s EIN.

Partnership (General Partnership, Limited Partnership)

Partnerships also require specific legal agreements:

- Partnership Agreement: This critical document details the ownership percentages, responsibilities, profit and loss distribution, and decision-making authority for each partner. It also specifies who has the authority to open and manage bank accounts.

- EIN Confirmation Letter (SS-4): The official letter from the IRS confirming your business’s EIN.

- Any state registration documents: Depending on your state, you might have specific registration requirements for partnerships.

Before heading to the bank or initiating an online application, it’s wise to call ahead or check the bank’s website for their precise list of required documents for your specific business type. Gathering everything beforehand ensures a smooth and efficient account opening experience, setting you up for financial success from day one.

The Application Process: Your Step-by-Step Walkthrough

With your bank chosen and all your documents in hand, you’re ready to tackle the application itself. The process can vary slightly depending on whether you opt for a traditional brick-and-mortar bank or an online-only institution, but the core steps remain consistent. Approaching this stage methodically will ensure a smooth experience and get your business banking up and running without unnecessary hurdles.

Step 1: Initiating the Application – Online vs. In-Person

- Online Application (for digital banks or traditional banks with robust online platforms):

- Access the Bank’s Website: Navigate to the business banking section of your chosen bank’s website. Look for “Open a Business Account” or similar prompts.

- Complete the Online Form: You’ll be guided through a series of digital forms requesting your business information, personal details of all owners/signatories, and questions about your business activities.

- Upload Documents: You’ll typically be prompted to upload digital copies (scans or clear photos) of all your pre-prepared documents (EIN letter, Articles of Organization, ID, etc.). Ensure these are legible and correctly formatted.

- Electronic Signatures: Many online applications allow for electronic signatures, making the process fully digital.

- Review and Submit: Double-check all entered information for accuracy before submitting. Errors can cause delays.

- In-Person Application (for traditional banks):

- Schedule an Appointment: While walk-ins are sometimes possible, scheduling an appointment with a business banking specialist ensures you have dedicated time and expertise.

- Bring All Documents: Arrive with all your original documents and, ideally, a set of photocopies. The bank will likely make their own copies.

- Meet with a Banker: The specialist will guide you through the application forms, explain the account features, and answer any questions you have. This is a great opportunity to clarify fee structures or specific service offerings.

- Sign Documents: You will sign various forms, including the account agreement, signature cards, and potentially agreements for any additional services (e.g., online banking access, debit cards).

Step 2: Providing Business and Personal Details

During the application, you’ll be asked to input or verbally provide the information you gathered in the previous step. This includes:

- Your business’s legal name, DBA name (if applicable), and physical address.

- Your EIN.

- Your business structure (Sole Proprietor, LLC, C-Corp, S-Corp, Partnership).

- Nature of your business operations.

- Personal details (name, address, SSN, date of birth) for all owners, partners, and authorized signers.

- Shareholder information (for corporations).

- Initial deposit amount and source of funds.

Be prepared to answer questions about the source of your initial deposit, especially if it’s a significant amount, as banks are required to comply with anti-money laundering regulations.

Step 3: Account Review and Approval

After submitting your application and documents, the bank will review everything. This process typically involves:

- Verification: The bank will verify the authenticity of your documents and information with relevant government agencies (e.g., Secretary of State, IRS).

- Background Checks: They will conduct background checks on all authorized signers, including checking credit history (though personal credit is less critical for a basic checking account, it can influence future lending products) and verifying identity to comply with “Know Your Customer” (KYC) regulations.

- Compliance Review: Ensuring your business and its activities comply with banking regulations and their internal policies.

The approval timeframe can vary. Online banks often boast quicker approvals, sometimes within minutes or a few business days, especially for simpler structures like sole proprietorships or single-member LLCs. Traditional banks might take a bit longer, from a few days to a week, particularly if additional verification is needed or if your business structure is more complex.

Step 4: Funding Your Account

Once approved, you’ll need to make an initial deposit to activate your account. This can typically be done via:

- Electronic Funds Transfer (EFT): Transferring funds from an existing personal or business account.

- Check Deposit: Depositing a personal check or a cashier’s check.

- Cash Deposit: If at a physical branch.

- Wire Transfer: For larger amounts or international transfers.

Be aware of any minimum initial deposit requirements the bank may have.

Common Pitfalls to Avoid During Application

- Incomplete Documentation: This is the biggest cause of delays. Double-check your checklist.

- Inconsistent Information: Ensure your business name, address, and EIN match exactly across all documents. Discrepancies can trigger verification issues.

- Lack of Clarity on Business Activities: Be clear and concise about what your business does. Vague descriptions can raise red flags.

- Not Understanding Fees: Don’t sign anything until you fully understand the fee schedule, minimum balance requirements, and any ways to waive monthly fees. Ask questions!

By following these steps and being meticulous with your preparation, you’ll navigate the business bank account application process with confidence, setting a strong financial foundation for your venture.

Activating and Managing Your New Account: Beyond Opening

Congratulations! You’ve successfully opened your business bank account. While the initial hurdle is cleared, the journey doesn’t end there. Activating and effectively managing your new account is crucial for harnessing its full potential and ensuring your business’s financial health. This involves more than just depositing money; it’s about integrating the account into your daily operations and leveraging its features for optimal control and efficiency.

Setting Up Your Account for Optimal Use

- Fund Your Account: As discussed, make your initial deposit. Ensure it meets any minimum balance requirements to avoid fees or account closures. Consider setting up a recurring transfer from a personal account if you’re bootstrapping with online business ideas you can start with no money, to ensure a steady float for initial expenses.

- Activate Your Debit Card and Online Banking: You’ll typically receive a business debit card (and possibly checks) in the mail. Activate your debit card immediately. More importantly, set up your online banking portal and/or mobile app. This is your primary interface for managing your funds, viewing transactions, and setting up payments. Explore all the features available.

- Link to Payment Processors: If your business accepts online payments (e.g., via Stripe, PayPal, Square, Shopify Payments), link your new business bank account to these platforms. This ensures that all your business revenue flows directly into your dedicated business account, maintaining that crucial financial separation.

- Integrate with Accounting Software: Connect your business bank account to your chosen accounting software (e.g., QuickBooks, Xero, FreshBooks). This integration automates transaction importing, simplifies reconciliation, and provides real-time insights into your business’s financial performance. This step is a game-changer for efficient bookkeeping.

- Set Up Bill Pay and Recurring Payments: Use your bank’s online bill pay feature to schedule recurring payments for business expenses like rent, utilities, software subscriptions, or loan payments. This helps ensure bills are paid on time and simplifies expense tracking.

- Order Checks (if needed): While many businesses operate largely paperless, having business checks on hand can be useful for certain vendors or situations. Ensure your checks prominently display your business name and address.

Proactive Account Management for Financial Control

Opening the account is just the beginning. Ongoing, proactive management is key to maintaining financial control and preventing issues.

- Regularly Monitor Transactions: Make it a habit to review your bank statements and online transactions frequently. This helps you:

- Catch Errors: Identify any unauthorized transactions, incorrect charges, or banking errors quickly.

- Track Expenses: Stay on top of where your money is going and ensure all expenses are legitimate business costs.

- Manage Cash Flow: Understand your incoming and outgoing funds to make informed decisions about spending and investment.

- Reconcile Your Account: At least monthly, reconcile your bank statements with your accounting software records. This process ensures that your internal records match the bank’s records, catching discrepancies and confirming accuracy.

- Set Up Alerts: Most banks offer customizable alerts via email or text. Set up notifications for:

- Low balance warnings.

- Large transactions (deposits or withdrawals).

- Overdrafts.

- Unusual activity.

These alerts provide real-time oversight and help you react quickly to important account activity.

- Maintain Sufficient Balances: Be mindful of your account balance to avoid overdraft fees or insufficient funds. Consider keeping a buffer for unexpected expenses. If your bank offers interest-bearing accounts, maintaining a healthy balance can also passively grow your funds.

- Separate Funds for Taxes: A smart strategy, especially for self-employed individuals, is to set aside a percentage of your income for taxes in a separate savings account linked to your business checking. This helps prevent sticker shock during tax season and is a crucial aspect of financial planning, mirroring the importance of how to plan for retirement by setting aside funds regularly.

- Review Fees Annually: Banks can change their fee structures. Annually, review your account statement for any new or increased fees. If you find your current bank is no longer cost-effective or meeting your needs, don’t hesitate to explore other options.

By diligently activating and managing your business bank account, you transform it from a mere storage facility for money into a powerful tool for financial insight, control, and growth. This proactive approach ensures your business’s finances are always in order, allowing you to focus on what you do best: running and expanding your enterprise.

Leveraging Your Business Account for Future Financial Success

Opening and managing a business bank account is more than just a compliance step; it’s a strategic move that can significantly influence your business’s long-term financial health and growth trajectory. By proactively using your account data and banking relationship, you can unlock opportunities for better cash flow, smarter investments, and robust future planning. This is where your business account truly becomes an asset, propelling you towards greater financial independence and stability.

Strategic Cash Flow Management

- Understanding Your Financial Rhythms: Your business bank account statements provide a treasure trove of data. By regularly analyzing your income and expenditure patterns, you can identify peak seasons, slow periods, and recurring expenses. This insight is invaluable for forecasting cash flow, ensuring you have enough liquidity to cover upcoming obligations, and making informed decisions about inventory, hiring, or marketing spend.

- Creating a Budget that Works: With clear visibility into your financial inflows and outflows, you can create a realistic and effective business budget. A well-structured budget, informed by your banking data, helps you allocate funds wisely, control discretionary spending, and set financial goals. It’s a foundational step towards taking control of your personal finances, extended to your business.

- Setting Aside Funds for Growth and Contingencies: Just as individuals plan for their future, businesses need to save. Use your business savings accounts (often linked to your checking) to build a reserve for unexpected emergencies, invest in new equipment, fund expansion, or save for future projects. This financial discipline, facilitated by separate accounts, minimizes reliance on debt for unforeseen needs.

Building Business Credit and Accessing Capital

- Establishing a Banking Relationship: A strong, positive relationship with your bank, built on consistent account activity and responsible management, can be incredibly beneficial. As your business grows, you might need financing for expansion, working capital, or large purchases. Banks are more likely to lend to businesses with whom they have a proven track record.

- Building Business Credit: Many banks offer business credit cards or small business loans. Using these responsibly and paying them off on time contributes to building your business credit score, separate from your personal credit. A robust business credit score opens doors to better loan terms, higher credit limits, and easier access to capital when you need it most.

- Exploring Lines of Credit: A business line of credit can act as a flexible safety net, providing access to funds up to a certain limit that you can draw upon as needed and repay. Your bank, having insight into your cash flow through your business account, is the natural place to explore such options.

Planning for Long-Term Sustainability and Personal Wealth

- Retirement Planning for Business Owners: As a business owner, your personal retirement planning is intricately linked to your business’s financial success. Your business bank account provides the clarity needed to determine how much you can contribute to various business retirement plans, such as a SEP IRA, Solo 401(k), or SIMPLE IRA. By setting up these plans through your business, you not only save for your future but also potentially reduce your taxable income. This directly ties into Fin3go’s guidance on “How to plan for retirement,” emphasizing the importance of starting early and making consistent contributions.

- Succession Planning and Exit Strategies: For larger businesses, a well-managed business account with clear financial records is vital for future succession planning or potential sale. Prospective buyers or inheritors will want to see transparent, organized financials to assess the business’s value and viability.

- Diversifying Investments: As your business generates profits, your bank can also offer or connect you with services for investing excess cash in short-term, low-risk instruments, or even facilitate transfers to investment accounts for longer-term growth. This allows your money to work harder for you, both within and outside your operational accounts.

Your business bank account is far more than just a place to hold money. It’s a financial hub that, when leveraged strategically, provides the data, tools, and relationships necessary to make informed decisions, secure financing, manage cash flow effectively, and ultimately achieve both your business and personal financial goals. By consistently engaging with your banking partner and utilizing the financial insights derived from your account, you are actively building a resilient and prosperous future for your enterprise in 2026 and beyond.

Common Pitfalls and How to Avoid Them

Even with the best intentions and a clear understanding of the steps involved, new business owners can sometimes stumble into common traps when it comes to managing their business bank accounts. Recognizing these pitfalls in advance can help you steer clear of them, ensuring your financial foundation remains solid and your business continues to thrive without unnecessary setbacks. Fin3go aims to empower you to avoid these issues, maintaining control over your financial journey.

1. Commingling Personal and Business Funds

- The Pitfall: This is arguably the most common and damaging mistake. Using your business account to pay for personal groceries, or your personal account to pay for business supplies, blurs the financial lines.

- Why it’s Bad: As discussed earlier, it undermines legal liability protection (piercing the corporate veil), makes bookkeeping a nightmare, complicates tax preparation, and can raise red flags during an audit. It also makes it incredibly difficult to get a true picture of your business’s profitability.

- How to Avoid: Be disciplined. Once your business account is open, commit to using it exclusively for business transactions. Get

Recommended Resources

Related reading: Best Business Ideas For Beginners 2025 (AssetBar).

You might also enjoy Best Store Credit Cards For Rewards 2026 from Gold Points.