Understanding Buy Now, Pay Later (BNPL): What It Is and How It Works

Buy Now, Pay Later (BNPL) represents a modern twist on an age-old concept: installment payments. What sets BNPL apart in the digital age is its seamless integration into the online shopping experience and its often interest-free nature. At its core, BNPL allows you to split the cost of a purchase into several smaller, manageable payments, typically over a few weeks or months.

The Mechanics of BNPL

When you opt for a BNPL service at checkout, the process is usually quick and straightforward:

- Instant Approval: Unlike traditional credit applications that can involve extensive checks and waiting periods, BNPL providers often offer instant approval based on minimal information. This typically involves a soft credit check, which doesn’t impact your credit score.

- Initial Payment: You usually pay a portion of the total cost upfront, often 25% for a typical “pay-in-four” model.

- Scheduled Installments: The remaining balance is then divided into a series of equal installments, usually paid every two weeks. The most common structure is four payments over six weeks, but some providers offer longer terms for larger purchases.

- Interest-Free (Often): A significant draw of BNPL is that these installments are frequently interest-free, provided you make all payments on time. If you miss a payment, however, late fees can apply.

- Merchant Pays a Fee: The BNPL provider makes its money by charging the merchant a fee for each transaction, similar to credit card processing fees. This allows them to offer interest-free plans to consumers.

Key Players in the BNPL Market

The BNPL landscape is dominated by several key players, each with slightly different offerings and target markets. Companies like Affirm, Afterpay, Klarna, and Zip (formerly Quadpay) have become household names, integrating their services across thousands of online retailers and physical stores. While the core model remains consistent, variations exist in payment terms, late fee structures, and the types of purchases eligible for BNPL financing. Understanding these nuances is crucial for consumers considering this payment method.

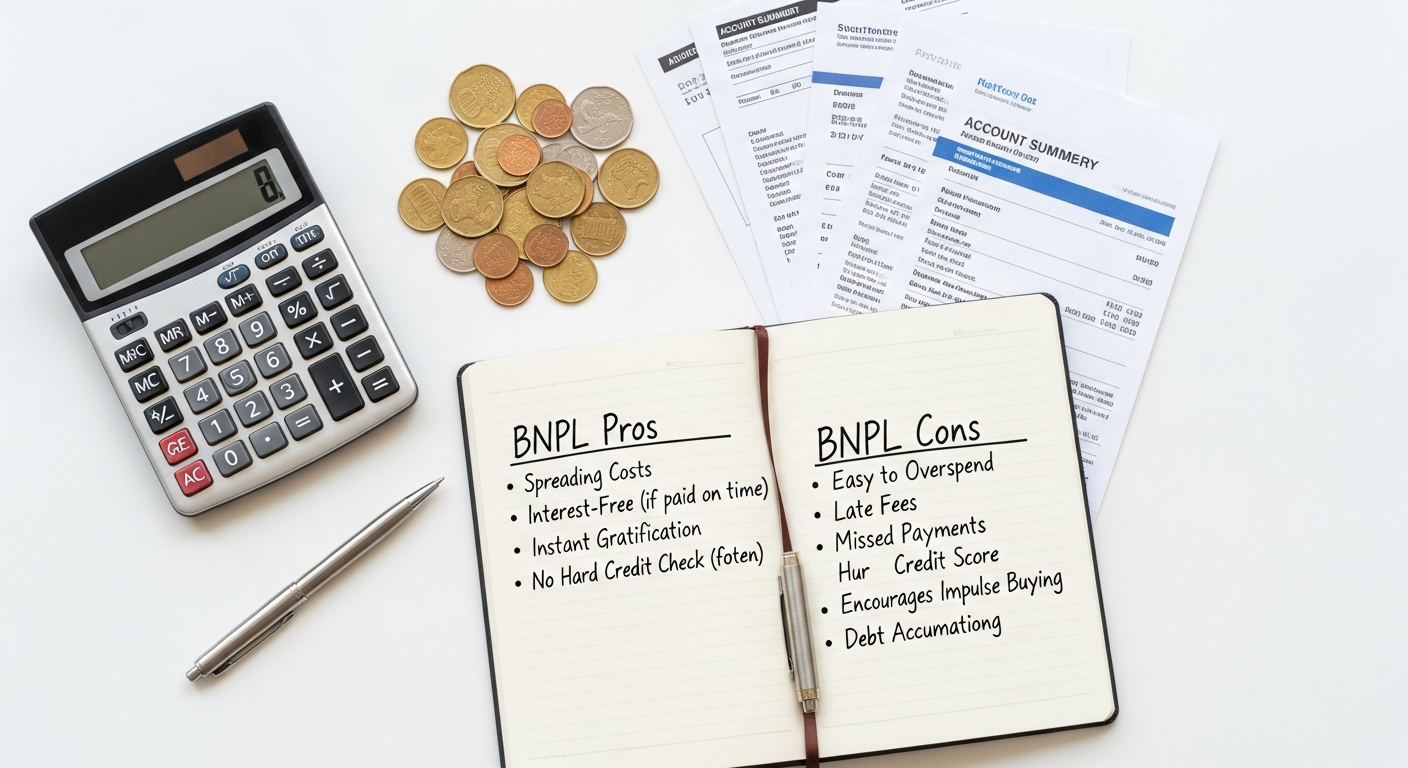

The Allure of BNPL: Exploring the Pros for Consumers

The rapid adoption of Buy Now, Pay Later services is not without reason. For many consumers, BNPL offers a compelling set of advantages that address common financial pain points and enhance the shopping experience.

1. Interest-Free Financing (When Managed Responsibly)

- Cost Savings: Perhaps the most significant advantage is the ability to spread the cost of a purchase over several payments without incurring interest charges. This stands in stark contrast to credit cards, which typically charge high Annual Percentage Rates (APRs) if balances aren’t paid in full by the due date. For consumers who diligently make their payments on time, BNPL can be a genuinely cheaper way to finance a purchase than revolving credit.

- Budgeting Aid: By breaking down a larger lump sum into smaller, predictable installments, BNPL can make expensive items more accessible and easier to fit into a monthly budget. This can be particularly useful for planned purchases that might strain immediate cash flow. However, it’s crucial to integrate these payments into a robust financial plan. Understanding How To Create A Monthly Budget is paramount to ensure BNPL doesn’t lead to overextension.

2. Increased Purchasing Power and Accessibility

- Bridging Income Gaps: For individuals who may not have immediate funds for a desired item but anticipate receiving income soon, BNPL can bridge that temporary gap. It allows consumers to acquire necessities or desired goods without waiting, which can be particularly useful for emergency purchases or time-sensitive deals.

- Alternative to Traditional Credit: BNPL offers an alternative financing option for those who may not qualify for traditional credit cards due to a limited credit history or a lower credit score. This broadens access to credit, albeit often for smaller, short-term loans.

3. Convenience and Simplicity

- Seamless Checkout Experience: BNPL services are typically integrated directly into the online checkout process, making it incredibly easy to select as a payment option. The application process is usually quick, requiring minimal personal information and often providing instant approval.

- Transparency: Most BNPL providers clearly outline the payment schedule, amounts, and any potential fees upfront. This transparency can help consumers understand their financial commitments before completing a purchase, though it’s still vital to read the terms carefully.

4. Reduced Risk Compared to High-Interest Credit Cards (Under Specific Conditions)

- Fixed Payment Schedule: The structured payment plan of BNPL can be less intimidating than a revolving credit card balance, which can fluctuate based on spending and minimum payments. Consumers know exactly what they owe and when.

- Lower Barrier to Entry: For new consumers or those rebuilding credit, BNPL can offer a taste of managing credit obligations without the potentially overwhelming limits and interest rates of a standard credit card.

Navigating the Pitfalls: The Cons and Risks of BNPL

1. Encouragement of Overspending and Debt Accumulation

- Illusion of Affordability: BNPL can create an illusion of affordability, making expensive items seem within reach by breaking down the cost into smaller chunks. This can lead consumers to purchase items they wouldn’t otherwise afford or need, resulting in impulse buying and overspending.

- Juggling Multiple Payments: It’s easy to sign up for multiple BNPL plans across different retailers and providers. Juggling several bi-weekly payments can quickly become complex, making it difficult to track total obligations and increasing the likelihood of missing payments. This fragmented debt can be harder to manage than a single credit card statement.

- Cumulative Debt: Individually, each BNPL plan might seem small, but collectively, they can add up to a substantial amount of debt. This cumulative burden can strain your finances, especially if unexpected expenses arise or income fluctuates.

2. Potential for Fees and Penalties

- Late Fees: While BNPL is often advertised as “interest-free,” this only holds true if all payments are made on time. Missing a payment typically incurs late fees, which can sometimes be substantial and quickly erode any perceived savings. Some providers also charge fees for rescheduling payments or for insufficient funds.

- Hidden Charges: While transparency has improved, consumers must still meticulously read the terms and conditions. Some BNPL plans for larger purchases might involve interest, or there could be fees for specific actions not immediately obvious.

3. Impact on Credit Score and Financial Health

-

Reporting Practices Vary: The impact of BNPL on your credit score is complex and varies significantly by provider. Some BNPL companies report your payment activity (both positive and negative) to credit bureaus, while others do not.

- Positive Reporting: If a BNPL provider reports on-time payments, it can help build a positive credit history, especially for those with thin credit files.

- Negative Reporting: Conversely, missed or late payments can be reported to credit bureaus, leading to a negative impact on your credit score. This can make it harder to qualify for larger loans (like mortgages or auto loans) in the future.

- Credit Utilization: While individual BNPL loans are usually small, having multiple open accounts can sometimes be viewed as a higher risk by traditional lenders, potentially affecting your debt-to-income ratio or overall credit profile, even if not directly reported as a traditional loan.

- Credit Checks: Most BNPL services perform a “soft” credit check, which doesn’t affect your score. However, some may perform a “hard” credit check, especially for larger purchases or longer payment terms, which can temporarily lower your score.

4. Less Consumer Protection Compared to Credit Cards

- Dispute Resolution: Traditional credit cards offer robust consumer protections under laws like the Fair Credit Billing Act, which makes it easier to dispute fraudulent charges or issues with purchased goods. BNPL services generally offer fewer consumer protections in this regard, making dispute resolution potentially more challenging. If you return an item, getting a refund processed through a BNPL provider can sometimes be more complicated than with a credit card.

- Regulatory Landscape: The BNPL industry is still relatively new and, in many regions, less regulated than traditional financial products. This evolving regulatory landscape means consumer protections can vary and may not be as comprehensive as those for banks or credit card companies.

BNPL’s Impact on Your Financial Health and Credit Score

Understanding how Buy Now, Pay Later services intertwine with your broader financial health and credit score is crucial for making informed decisions. While often presented as a benign alternative to credit, BNPL has distinct implications that can either bolster or undermine your financial stability.

The Nuances of Credit Reporting

One of the most frequently asked questions about BNPL revolves around its impact on credit scores. The answer is nuanced:

- Soft vs. Hard Inquiries: Most BNPL transactions involve a “soft” credit check to assess your eligibility. A soft inquiry does not affect your credit score. However, for larger purchases or longer-term plans, some providers may perform a “hard” inquiry, which can cause a slight, temporary dip in your score.

-

Reporting to Credit Bureaus: This is where the variability lies.

- Some BNPL providers are beginning to report on-time payments to major credit bureaus. For consumers with limited credit history, this can be an excellent way to build a positive credit profile, demonstrating responsible financial behavior.

- Other providers, or specific types of BNPL plans (like the shorter “pay-in-four” models), may not report positive payment history at all. In such cases, while you benefit from interest-free payments, you don’t build credit.

- Crucially, almost all BNPL providers will report negative activity. Missed payments, defaults, or accounts sent to collections will almost certainly be reported to credit bureaus, severely damaging your credit score. This negative mark can persist for several years, affecting your ability to secure future loans, rent apartments, or even get certain jobs.

- Credit Utilization and Debt-to-Income Ratio: Even if individual BNPL accounts aren’t always reported, the underlying debt can still indirectly impact your financial standing. Lenders reviewing your overall financial picture (e.g., for a mortgage) might consider all outstanding installment obligations, including BNPL, when assessing your debt-to-income ratio. A higher ratio can signal increased risk, potentially affecting loan approvals or interest rates.

Impact on Financial Stability and Budgeting

The cumulative effect of multiple BNPL plans can easily lead to financial strain, even for those with robust financial habits.

- Budgetary Overload: The ease of signing up for multiple BNPL agreements can quickly overwhelm even a well-structured budget. What starts as a convenient way to split one payment can morph into a complex web of bi-weekly debits that are difficult to track. This makes effective budgeting incredibly challenging. A key step in maintaining financial health is mastering How To Create A Monthly Budget, which includes meticulously tracking all incoming and outgoing funds, including BNPL installments. Without this, the illusion of affordability can lead to a real cash flow crisis.

- Reduced Emergency Savings: If a significant portion of your disposable income is allocated to BNPL payments, it leaves less room for building an emergency fund. Should an unexpected expense arise – a car repair, medical bill, or job loss – you might find yourself without a financial safety net, potentially forcing you into further debt or defaulting on BNPL payments.

- Delayed Financial Goals: Every dollar committed to a BNPL payment is a dollar that isn’t going towards savings, investments, or accelerating debt payoff. This can delay achieving long-term financial goals, such as saving for a down payment, retirement, or even building wealth through strategies like exploring Passive Income Ideas 2026.

The Risk of the Debt Spiral

For some, BNPL can be a slippery slope into a debt spiral. If one misses a payment, late fees accrue. To cover these, a consumer might use another BNPL service for a new purchase, or even resort to high-interest credit cards or payday loans, creating a vicious cycle of debt. This scenario underscores the importance of a clear debt management strategy. For those already grappling with various forms of debt, understanding methods like the Snowball Vs Avalanche Debt Payoff Method becomes critical. While BNPL debt might not always fit neatly into these categories due to its short-term nature, prioritizing its repayment, especially if late fees are accumulating, is paramount to prevent it from escalating into a larger problem.

Integrating BNPL into a Prudent Financial Strategy

While the risks associated with Buy Now, Pay Later are significant, it doesn’t mean BNPL should be entirely avoided. For financially disciplined individuals, BNPL can be a useful tool when integrated thoughtfully into a broader, prudent financial strategy. The key lies in conscious consumption and meticulous management.

1. Master Your Budget First

- Non-Negotiable Foundation: Before even considering a BNPL purchase, you must have a clear understanding of your income, expenses, and disposable cash flow. This means creating and sticking to a detailed monthly budget. Our guide on How To Create A Monthly Budget provides an excellent framework for this. Every BNPL payment, just like any other bill, must be accounted for within your budget.

- Allocate Funds: Treat BNPL installments as fixed expenses. Ensure you have the funds readily available for each payment date before committing to the purchase. If adding a BNPL payment stretches your budget thin, it’s a clear sign to reconsider the purchase.

2. Use BNPL Strategically and Sparingly

- For Planned, Essential Purchases: Reserve BNPL for necessary items or planned purchases that you know you can comfortably afford in the short term, but where splitting payments offers a temporary cash flow advantage. Avoid using it for impulse buys or discretionary spending.

- When You Have the Full Amount: A golden rule for using BNPL is to only use it when you already have the full purchase amount in your bank account. This way, if anything goes wrong (e.g., you forget a payment, or an unexpected expense arises), you have the funds to cover it, preventing late fees or credit score damage.

- One at a Time: Limit yourself to one active BNPL plan at a time. Juggling multiple payment schedules significantly increases the risk of missed payments and overspending.

3. Understand the Terms and Conditions

- Read the Fine Print: Always, without exception, read the specific terms and conditions of each BNPL provider and individual purchase agreement. Understand the payment schedule, late fees, any potential interest charges, and the policy for returns or disputes.

- Check Credit Reporting Practices: If building credit is a goal, choose BNPL providers that explicitly state they report positive payment history to credit bureaus. Be aware that most will report negative activity regardless.

4. Set Up Reminders and Automate Payments

- Never Miss a Payment: The primary risk of BNPL is missing a payment and incurring late fees or damaging your credit. Set up calendar reminders, use budgeting apps, or ideally, automate payments directly from your bank account to ensure all installments are made on time.

5. Prioritize BNPL in Debt Management

- High-Interest vs. BNPL: If you find yourself with multiple forms of debt, including BNPL, credit card debt, or personal loans, it’s crucial to have a clear debt payoff strategy. Methods like the Snowball Vs Avalanche Debt Payoff Method are excellent tools. While BNPL typically doesn’t have interest (if paid on time), late fees can be punitive. Consider prioritizing BNPL payments alongside high-interest debts to avoid these penalties and maintain a clean payment history. If late fees start to accumulate on BNPL, it quickly becomes a high-cost debt that should be addressed urgently.

The Future of BNPL and Personal Finance in 2026

The Buy Now, Pay Later industry is far from static. As it matures, we can anticipate significant shifts in its regulatory landscape, technological integration, and its role within the broader personal finance ecosystem. These changes will undoubtedly shape how consumers interact with BNPL in 2026 and beyond.

Evolving Regulatory Oversight

- Increased Scrutiny: Governments and financial regulators worldwide are increasingly scrutinizing BNPL services. Concerns around consumer debt, transparency, and consumer protection are prompting calls for stricter regulations. In 2026, we can expect to see more comprehensive frameworks introduced, potentially mirroring some of the protections afforded to traditional credit products. This could include clearer disclosure requirements, limits on late fees, and enhanced dispute resolution processes.

- Credit Reporting Standardization: The current inconsistency in how BNPL impacts credit scores is likely to be addressed. Regulators may push for more standardized reporting of BNPL activity (both positive and negative) to credit bureaus, making the financial implications clearer for both consumers and traditional lenders. This could lead to BNPL playing a more defined role in credit building or, conversely, having a more direct negative impact on those who default.

Technological Integration and Personalization

- AI and Machine Learning: BNPL providers will continue to leverage artificial intelligence and machine learning to refine their underwriting processes, offering more personalized payment plans and real-time risk assessments. This could lead to more dynamic eligibility criteria and more tailored offerings for different consumer segments.

- Embedded Finance: BNPL is a prime example of embedded finance, where financial services are seamlessly integrated into non-financial platforms. By 2026, we’ll likely see even deeper integration, with BNPL options becoming a standard feature across a wider array of digital touchpoints, from social commerce to subscription services.

- Consolidated Financial Views: As BNPL becomes more pervasive, there will be a greater need for tools that help consumers manage all their financial obligations in one place. Fintech innovations will likely emerge to provide consolidated views of all BNPL debts alongside traditional credit, helping individuals to better understand their overall financial picture and manage their budgets more effectively. This ties back into the importance of a comprehensive approach to How To Create A Monthly Budget, encompassing all forms of debt.

BNPL’s Role in a Holistic Financial Picture

- Complementary, Not Replacement: BNPL will likely settle into its role as a complementary payment tool rather than a wholesale replacement for credit cards. For consumers with strong financial literacy and discipline, it can remain a convenient, interest-free option for specific purchases. However, its limitations in terms of rewards, consumer protection, and credit building (in some cases) will keep traditional credit cards relevant for many.

- Emphasis on Financial Literacy: The growth of BNPL will further underscore the critical importance of financial literacy. Consumers will need to be savvier than ever about managing multiple credit lines, understanding terms and conditions, and budgeting effectively to avoid falling into debt traps.

- Long-Term Wealth Building: For those who master the art of integrating BNPL responsibly, the absence of interest on short-term purchases can free up capital that might otherwise go towards credit card interest. This capital, when managed wisely, can be redirected towards savings, investments, or accelerating debt payoff using strategies like the Snowball Vs Avalanche Debt Payoff Method. Looking ahead to 2026, a strong financial foundation built on responsible spending and smart investing (including exploring various Passive Income Ideas 2026) will be key to leveraging innovative payment solutions like BNPL without compromising long-term wealth creation. Passive income streams can provide an additional buffer, making consumers less reliant on short-term credit solutions and more resilient to financial shocks, further reducing the need for BNPL or making it an even safer option.

In conclusion, Buy Now, Pay Later is a powerful financial tool with both immense potential and significant risks. Its future in 2026 will be shaped by a balance of innovation, regulation, and evolving consumer behavior. For individuals, success with BNPL hinges on education, discipline, and its strategic integration into a well-defined personal finance plan.

Frequently Asked Questions

Recommended Resources

Check out How To Make Money While You Sleep on Trading Costs for a deeper dive.

Learn more about this topic in Best Buy Now Pay Later Apps 2026 at Gold Points.