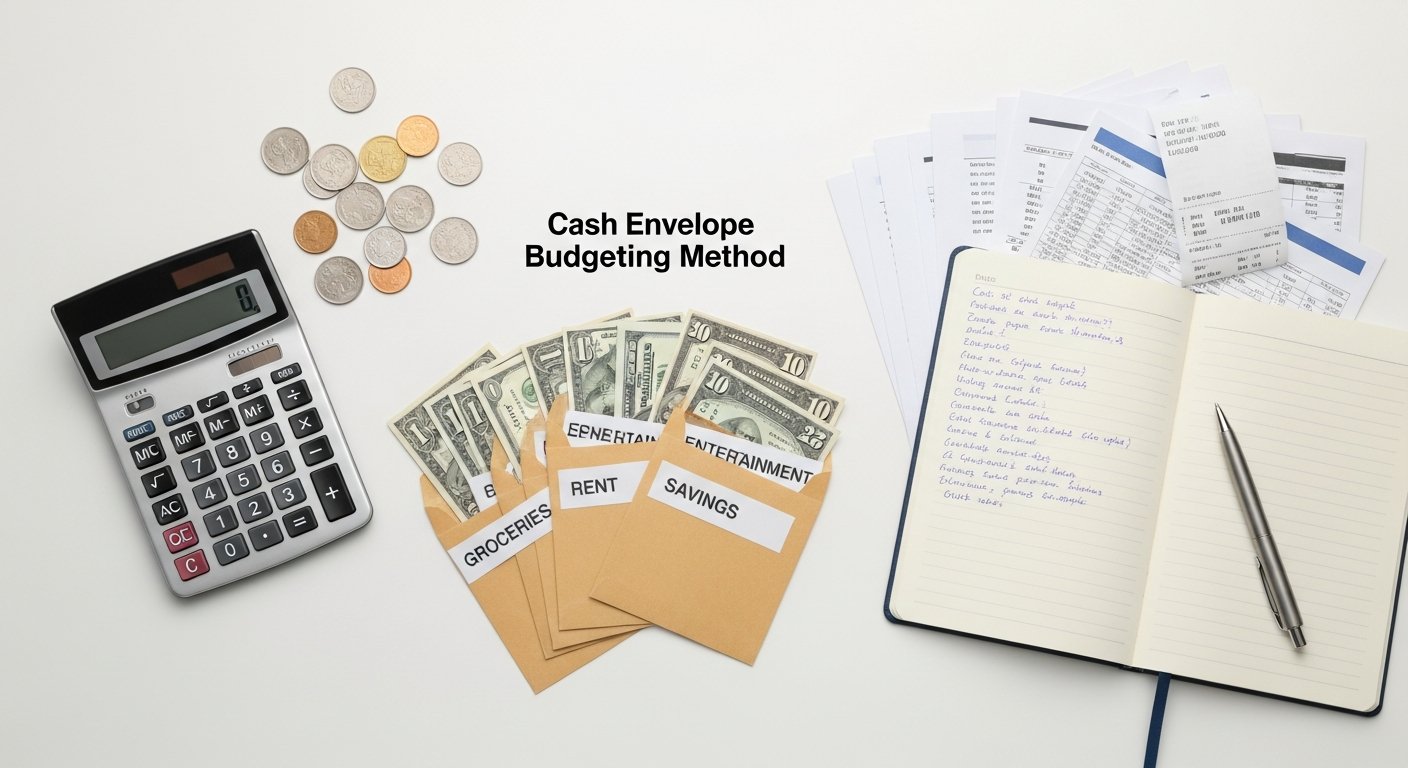

What is the Cash Envelope Budgeting Method?

At its core, the cash envelope budgeting method is a straightforward, tactile approach to managing your discretionary spending. It involves allocating specific amounts of physical cash into designated envelopes for various spending categories each month. Once the cash in an envelope is depleted, spending in that category must cease until the next budgeting period. This method serves as a powerful visual and physical barrier to overspending, forcing a direct confrontation with the reality of your financial limits.

The concept itself is not new; variations of it have been used for generations by households looking to live within their means. However, its resurgence in popularity in the digital age speaks volumes about its enduring effectiveness. While modern apps and digital spreadsheets offer convenience, they often lack the visceral connection that physical cash provides. When you hand over a twenty-dollar bill, there’s a tangible sense of loss that simply doesn’t accompany a swipe of a card or a tap on a screen. This psychological “pain of paying” is a key component of the cash envelope system’s success, making you more mindful of each transaction and encouraging more deliberate purchasing decisions.

Consider it a hands-on extension of your broader financial plan. Instead of merely tracking expenses after they’ve occurred, the cash envelope method proactively limits them. It’s a system that doesn’t just tell you how much you can spend; it physically prevents you from spending more than you’ve allotted. This distinction is crucial for those who struggle with impulse buys or find themselves consistently over budget in variable spending categories like dining out, entertainment, or groceries. By compartmentalizing your funds into physical envelopes, you create a clear, unmistakable boundary for each area of your financial life, fostering a discipline that many digital tools struggle to replicate.

The Tangible Benefits of Going Cash-Only for Spending

While the digital age offers unparalleled convenience, it often comes at the cost of financial awareness. The cash envelope method, by contrast, reintroduces a tangible element that can profoundly impact your spending habits and overall financial health. The benefits extend far beyond simply sticking to a budget; they cultivate a deeper understanding and appreciation for your money.

Eliminating Overspending and Curbing Impulse Buys

This is arguably the most immediate and profound benefit. When you pay with a debit or credit card, the transaction often feels abstract. There’s no physical representation of the money leaving your possession. With cash, every dollar spent is a dollar physically removed from your envelope, and once an envelope is empty, that’s it. This hard stop prevents you from dipping into funds allocated for other purposes or, worse, accumulating debt. It forces you to pause and consider if a purchase is truly necessary or just an impulse, a stark contrast to the frictionless experience of card payments.

Increasing Financial Awareness and Mindful Spending

The act of physically counting, allocating, and spending cash fosters a heightened sense of financial awareness. You become intimately familiar with how much money you have for each category and how quickly it diminishes. This daily interaction with your funds makes you more conscious of where your money is going. You might find yourself asking, “Is this meal worth emptying my dining out envelope for the week?” or “Do I really need this item, or can I wait?” This mindfulness translates into more deliberate and value-driven spending decisions, aligning your expenditures with your financial goals rather than your fleeting desires.

Simplifying Budget Tracking and Reducing Financial Stress

While a comprehensive digital budget is essential, the cash envelope system simplifies tracking for variable expenses. Instead of meticulously logging every transaction, a quick glance at your envelopes tells you exactly how much you have left in each category. This can significantly reduce the mental load and stress associated with budgeting, especially for those who find traditional expense tracking overwhelming. The clarity and simplicity of the system mean less time spent on reconciliation and more time focusing on your financial objectives.

Accelerating Debt Reduction and Building Savings

By preventing overspending, the cash envelope method naturally frees up funds that might otherwise have been spent unnecessarily. This surplus can then be directed towards accelerating debt repayment or bolstering your savings. Imagine if you consistently saved just $50-$100 each month by curbing impulse buys – over a year, that’s $600-$1200 that could go towards a credit card balance or an emergency fund. This disciplined approach is a powerful ally in your journey towards financial freedom. Furthermore, by actively managing your spending, you create a stronger foundation for building wealth, as discussed in Fin3go’s guide on How To Build Generational Wealth, which emphasizes the importance of disciplined financial habits from the ground up.

Empowering You with a Sense of Control

In a world where many feel like their finances are spiraling out of control, the cash envelope method offers a tangible sense of empowerment. You are actively making choices about where every dollar goes, rather than reactively responding to bills and statements. This proactive stance can be incredibly motivating, transforming budgeting from a chore into a rewarding exercise in self-mastery. It reinforces the principle that you are the architect of your financial future, capable of making conscious decisions that align with your long-term aspirations. This level of control is a critical component of establishing a robust and sustainable financial plan, as highlighted in our comprehensive guide on How To Create A Monthly Budget, where the cash envelope system can serve as a potent tool for managing the variable spending components of that budget.

A Step-by-Step Guide to Mastering the Cash Envelope System

Step 1: Assess Your Current Financial Situation

Before you can allocate funds, you need to understand what funds you have and where they currently go. Gather all your financial statements: pay stubs, bank statements, credit card statements, and utility bills. List all your sources of income and all your fixed expenses (rent/mortgage, loan payments, insurance premiums, subscriptions, etc.). This initial audit provides the crucial baseline for your budgeting efforts. Don’t skip this step; it’s the foundation upon which your entire budget will be built.

Step 2: Create a Comprehensive Monthly Budget

This step is paramount and directly ties into Fin3go’s extensive advice on How To Create A Monthly Budget. You need to know exactly how much you can afford to spend in total before you can divide it into envelopes. Subtract your total fixed expenses from your total net income. The remaining amount is what you have available for variable spending and savings. Within this variable spending, you will identify your cash envelope categories. Be realistic and honest about your past spending habits, but also ambitious about where you want to cut back. This is where you decide your financial goals – whether it’s reducing debt, saving for a down payment, or investing for retirement. Every dollar needs a job.

Step 3: Identify Your Cash Envelope Categories

Not every expense needs a cash envelope. Fixed expenses like rent or loan payments are typically paid electronically. The cash envelope method shines brightest for variable expenses where overspending is common. Common categories include:

- Groceries: Often a major budget buster.

- Dining Out/Takeaway: A notorious area for impulse spending.

- Entertainment: Movies, concerts, hobbies, nights out.

- Personal Care: Haircuts, toiletries, cosmetics.

- Fuel/Transportation: If you use cash for gas.

- Miscellaneous/Flex Spending: For unexpected small purchases.

- Clothing: For occasional purchases.

List all the categories where you tend to overspend or where you want to exercise more control. Assign a specific, realistic budget amount to each category based on your comprehensive monthly budget from Step 2.

Step 4: Withdraw and Allocate Cash

At the beginning of each budget period (usually monthly or bi-weekly, depending on your pay schedule), withdraw the exact total amount of cash needed for all your variable spending categories. Then, physically place the designated amount of cash into its respective envelope. Label each envelope clearly with the category name and the allocated amount. This physical act of distributing the cash is critical; it makes your budget tangible and immediate.

Fin3go Tip: When withdrawing, try to get a mix of denominations. It’s easier to make exact change and less tempting to break a large bill for a small purchase if you have smaller bills readily available.

Step 5: Spend Wisely and Track

This is where the rubber meets the road. When you need to make a purchase in a specific category, take the money from that envelope. Only use the cash from the relevant envelope. When the cash in an envelope is gone, you stop spending in that category until the next budgeting cycle. There are no exceptions, no borrowing from other envelopes (unless it’s an agreed-upon, rare emergency transfer, carefully noted). This strict adherence is what makes the system so effective. It’s important to understand that if your “dining out” envelope is empty mid-month, you’ll be eating at home.

While the beauty of the system is its simplicity, it can still be helpful to keep a small ledger or note inside each envelope for larger purchases, just to track the remaining balance more accurately, especially if you’re dealing with many small transactions.

Step 6: Review and Adjust

At the end of each budgeting period, review your envelopes. Did you have money left over in some categories? Did you run out too quickly in others? This feedback is invaluable. Adjust your allocations for the next month based on your experiences. The first few months might involve some trial and error, and that’s perfectly normal. The goal is to create a sustainable system that works for you, not against you. Be flexible enough to learn but firm enough to stick to your limits. This iterative process of budgeting and adjustment is a cornerstone of long-term financial success, continuously refining your approach towards achieving your financial goals for 2026 and beyond.

Overcoming Common Hurdles and Maximizing Your Cash Envelope Success

While the cash envelope method is powerful, it’s not without its challenges in a predominantly digital economy. Successfully integrating it into your life requires anticipating these hurdles and developing strategies to overcome them.

Dealing with Online Purchases and Digital Transactions

One of the most frequent questions is: “How do I use cash envelopes for online shopping?” The purest form of the method involves only cash, but a hybrid approach is often necessary. For online purchases within a cash envelope category (e.g., clothing), you would still deduct the amount from the physical envelope. Then, either leave an IOU note in the envelope for the amount spent or immediately transfer that exact amount from your checking account into savings, effectively “reimbursing” your physical cash budget. Alternatively, you can use a single debit card for all online purchases and, at the end of the week, reconcile those purchases by removing the corresponding cash from the relevant envelopes and depositing it back into your bank account. This ensures your digital spending mirrors your physical budget allocation.

Security Concerns of Carrying Cash

Carrying large sums of cash can present security risks. To mitigate this, consider:

- Weekly Withdrawals: Instead of withdrawing a full month’s worth of cash, opt for weekly withdrawals. This reduces the amount of cash you carry at any given time.

- Limiting High-Value Categories: For very large variable expenses (e.g., a planned electronics purchase), you might keep those funds in your bank account and only withdraw when needed, still ensuring it comes out of a budgeted category.

- Secure Storage: At home, keep your envelopes in a safe, discreet location. When out, carry only the envelopes you anticipate needing and only the amount necessary for planned purchases.

The Temptation to “Borrow” from Other Envelopes

This is a major pitfall. The integrity of the cash envelope system relies on strict adherence to category limits. If you run out of money in your “dining out” envelope, you don’t take from “groceries.” If you find yourself constantly tempted to borrow, it’s a sign that:

- Your initial budget allocations might be unrealistic: Revisit Step 2 and adjust your category amounts for the next month.

- You lack discipline: Reinforce your commitment to the system. Remember, the “pain of paying” and the hard stop are what make this method effective.

If an absolute emergency arises and you must borrow, make it a conscious decision. Note the transfer clearly on both envelopes, and make a plan to replenish the “borrowed from” envelope as soon as possible, perhaps by temporarily cutting back on another non-essential category next month.

Handling Unexpected Expenses

The cash envelope system primarily manages discretionary spending, not emergencies. It’s crucial to have a separate emergency fund for unexpected events (car repairs, medical bills, etc.). This fund should be kept in a separate, easily accessible savings account, not in an envelope. If you find yourself constantly needing to dip into your envelopes for “unexpected” expenses that aren’t true emergencies, it suggests a need to refine your budget to include a small buffer or a dedicated “miscellaneous” envelope for minor unforeseen costs.

The Discipline Required

The cash envelope method demands discipline and consistency. It’s not a set-it-and-forget-it system. Regular review, adherence to rules, and willingness to adapt are key. The initial learning curve can be challenging, especially for those accustomed to swiping cards without much thought. However, the more consistently you apply the method, the more natural and rewarding it becomes, transforming financial management from a burden into an empowering habit.

Integrating Cash Envelopes with a Holistic Financial Strategy

While powerful for managing variable spending, the cash envelope method is most effective when integrated into a broader, holistic financial strategy. It’s a critical tool in your financial toolbox, but not the only one. Fin3go advocates for a comprehensive approach that leverages various strategies for maximum impact on your financial well-being.

Complementing Digital Tools for Fixed Expenses

The beauty of the cash envelope system lies in its tactile nature for variable spending. For fixed expenses (rent, mortgage, utilities, loan payments, insurance premiums, streaming services), digital automation is usually far more efficient and secure. Set up automatic payments for these predictable bills from your checking account. Your cash envelopes then manage the remaining discretionary income, creating a powerful synergy: automation for stability, cash for control. This dual approach ensures both your essential commitments are met effortlessly and your flexible spending is kept in check, preventing overspending that could jeopardize your fixed payments.

Its Role in Debt Repayment Plans

For those actively working to reduce debt, the cash envelope method can be a game-changer. By dramatically reducing impulse and unnecessary spending, it frees up more money to allocate towards debt repayment. Imagine if your “dining out” envelope consistently had $50 left over each month, or your “entertainment” budget was consistently underspent by $30. That $80 extra can be channeled directly into an avalanche or snowball debt repayment plan. This direct redirection of saved funds accelerates your journey to becoming debt-free, creating a positive feedback loop where discipline in one area fuels progress in another.

Leveraging Saved Funds from Bill Negotiations

Fin3go consistently emphasizes proactive steps to optimize your finances, including strategies outlined in our guide on How To Negotiate Bills And Lower Expenses. When you successfully negotiate lower rates for internet, insurance, or subscription services, you create additional disposable income. This newfound cash can be strategically allocated. Rather than letting it disappear into general spending, you can choose to:

- Increase an Envelope Allocation: If a specific category consistently runs short, you can slightly boost its budget.

- Bolster Savings: Direct the savings into your emergency fund, investment accounts, or a specific savings goal.

- Accelerate Debt Repayment: Funnel the extra funds into high-interest debt.

The cash envelope method ensures that these savings are consciously managed and directed towards your financial goals, rather than simply absorbed by increased spending.

Contributing to Savings and Investment Goals

Ultimately, the discipline cultivated by the cash envelope method is a foundational skill for building wealth. By gaining granular control over your spending, you create predictable surpluses. These surpluses are the fuel for your savings and investment vehicles. Whether you’re saving for a down payment on a house, funding a child’s education, or building a robust retirement portfolio for 2026 and beyond, consistent saving is non-negotiable. The cash envelope method helps you identify and free up those critical dollars that might otherwise have been frittered away. It instills the habit of living below your means, a cornerstone principle for long-term financial prosperity.

Its Contribution to Building Generational Wealth

The principles learned through cash envelope budgeting contribute directly to the broader objective of How To Build Generational Wealth. Generational wealth isn’t just about large inheritances; it’s about instilling strong financial literacy, discipline, and responsible money management habits across generations. By demonstrating and practicing intentional spending with the cash envelope method, you set a powerful example for your children and future descendants. They learn the value of a dollar, the importance of living within one’s means, and the power of conscious financial decision-making. These are the intangible assets that truly create a legacy of financial security and freedom for generations to come, far more impactful than merely accumulating assets without the wisdom to manage them.

Is the Cash Envelope Method the Right Fit for Your Financial Journey?

Deciding whether the cash envelope budgeting method is suitable for your financial journey involves an honest assessment of your spending habits, personality, and current financial challenges. While it offers profound benefits, it’s not a one-size-fits-all solution. Fin3go encourages you to consider the following points to determine if this powerful tool aligns with your financial aspirations.

Who Benefits Most from the Cash Envelope System?

- Impulsive Spenders: If you frequently find yourself making unplanned purchases or wondering where your money went, the tangible nature of cash envelopes provides the immediate feedback and hard stop needed to break these habits.

- Individuals New to Budgeting: For those overwhelmed by complex spreadsheets or budgeting apps, the simplicity and directness of cash envelopes offer an accessible entry point into financial management. It’s a great way to learn the fundamentals of allocation and adherence.

- Those Struggling with Credit Card Debt: By shifting spending away from credit cards, the system helps prevent further debt accumulation and can free up funds to pay down existing balances more aggressively.

- Visual and Kinesthetic Learners: If you learn best by doing and seeing, the physical act of handling money and watching envelopes empty can be incredibly effective for internalizing financial concepts.

- Families Teaching Financial Literacy: It’s an excellent method for teaching children about money management, limits, and choices in a concrete way. Giving them an allowance in an envelope for their spending categories can be a powerful lesson.

Who Might Find It Challenging?

- Heavy Online Shoppers: While hybrid methods exist, a purely cash-based system can feel cumbersome for those who primarily shop online. It requires extra steps to reconcile digital purchases with physical cash.

- Individuals Uncomfortable Carrying Cash: Security concerns or a general preference for cashless transactions might make this method less appealing.

- Those Lacking Discipline: The system’s effectiveness hinges on strict adherence. If you consistently “borrow” from envelopes or fail to track, the method loses its power. It requires commitment.

- People with Highly Irregular Income: While adaptable, highly fluctuating income can make monthly allocation challenging, requiring more frequent adjustments and careful planning.

Personalization and Flexibility

It’s crucial to remember that the cash envelope method is a framework, not a rigid dogma. You can personalize it to fit your lifestyle:

- Hybrid Approach: Combine cash for variable spending with digital payments for fixed bills.

- Limited Categories: Start with just 2-3 categories where you struggle most, rather than trying to cash-budget everything at once.

- Weekly vs. Monthly: Adjust your withdrawal and allocation schedule to match your pay cycle or comfort level with carrying cash.

- Digital Envelopes: Some apps now mimic the envelope system digitally, offering a compromise if physical cash is a non-starter, though they often lack the same psychological impact.

Ultimately, the cash envelope method is a powerful tool for gaining control over your spending, fostering financial awareness, and accelerating your journey towards financial freedom. If you’re seeking a tangible, straightforward way to transform your relationship with money in 2026, it’s certainly worth exploring. Give it a try for a few months, remain open to adjusting your approach, and observe the profound impact it can have on your financial discipline and peace of mind. Fin3go believes in empowering you with practical strategies, and the cash envelope system is a prime example of a simple solution yielding extraordinary results.

Frequently Asked Questions

Recommended Resources

Related reading: Best Ways To Save Money In 2026 (Trading Costs).

Related reading: How To Use Instagram For Ecommerce Sales (E-ComProfits).