Defined Benefit vs. Defined Contribution Plans Explained: Your 2026 Guide to Retirement Security

By Fin3go Editorial Team — Financial writers covering personal finance, banking, and consumer protection.

The landscape of American retirement has shifted seismically over the last four decades, moving away from the paternalistic “pension era” and into the “age of self-reliance.” As we navigate 2026, the distinction between a Defined Benefit (DB) plan and a Defined Contribution (DC) plan is no longer just HR jargon—it is the single most important factor determining when, where, and how you will retire. For many workers, the choice isn’t just about how much money they save, but who carries the risk if the stock market tumbles or inflation spikes. Understanding these two pillars of retirement planning is essential because the “default” settings of your workplace plan may not be enough to sustain your lifestyle in an increasingly expensive world. Whether you are a public sector employee with a traditional pension or a corporate climber managing a 401(k), the strategies you employ today will dictate your financial freedom tomorrow. This guide breaks down the mechanics, the risks, and the actionable steps you need to take in 2026 to ensure your golden years are actually golden.

1. The Core Mechanics: “The Paycheck” vs. “The Piggy Bank”

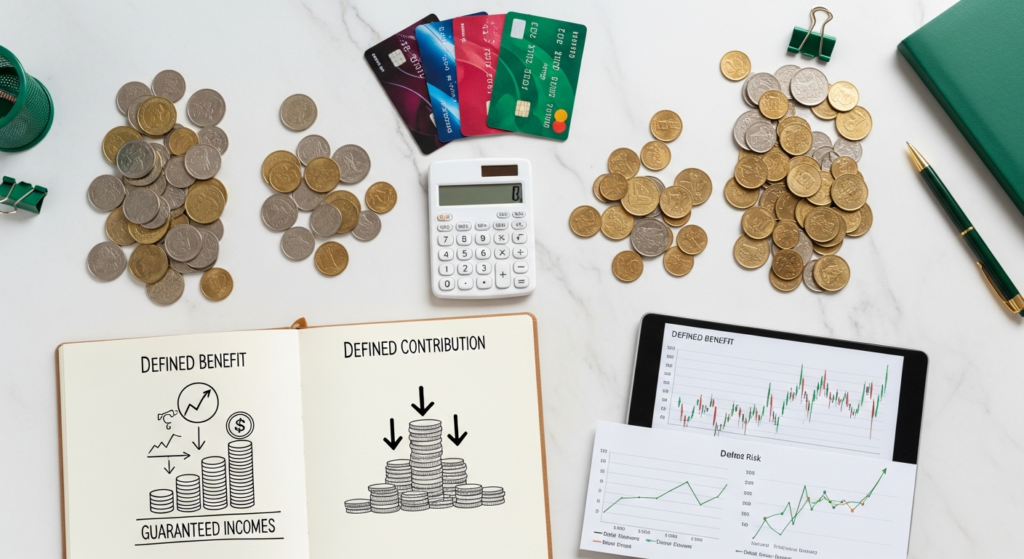

At its most fundamental level, the difference between these two plans lies in what is being “defined.”

**Defined Benefit (DB) Plans**, commonly known as traditional pensions, promise a specific monthly benefit at retirement. The “benefit” is defined by a formula, usually based on your salary history and years of service. For example, a teacher might be promised 2% of their average final salary multiplied by their 30 years of service. In this scenario, the employer bears the investment risk. If the pension fund underperforms, the employer (or the taxpayer, in public plans) must make up the difference.

**Defined Contribution (DC) Plans**, such as 401(k)s, 403(b)s, and 457 plans, define the “contribution” going into the account today, but they make no promises about the future balance. You (and often your employer via a match) put money into an individual account. You choose the investments, and your eventual retirement income depends entirely on how much you contributed and how those investments performed. In this model, the “piggy bank” belongs to you, but so does the risk of it running dry.

**Actionable Tip:** Check your latest benefits statement. If you see a “Projected Monthly Benefit,” you likely have a DB plan. If you see a “Total Account Balance,” you have a DC plan. Knowing which one you have is the first step in calculating your “Retirement Gap.”

2. The Pros and Cons of the Traditional Pension (Defined Benefit)

In 2026, defined benefit plans are increasingly rare in the private sector but remain a staple for government employees, military personnel, and some unionized industries.

**The Advantages:**

* **Lifetime Income:** You cannot outlive a pension. It provides a steady “paycheck” for as long as you live, and often offers survivor benefits for a spouse.

* **Professional Management:** You don’t have to worry about asset allocation or market timing; professional fund managers handle the investments.

* **Stability:** Your retirement income isn’t tied to the daily fluctuations of the S&P 500.

**The Drawbacks:**

* **Lack of Portability:** Pensions often have long “vesting” periods (sometimes 5 to 10 years). If you leave the job early, you might leave with nothing.

* **Inflation Risk:** While some public pensions have Cost-of-Living Adjustments (COLAs), many private pensions do not. A $3,000 monthly check might feel substantial in 2026, but its purchasing power will be significantly lower by 2046.

* **Employer Solvency:** While protected by the Pension Benefit Guaranty Corporation (PBGC), if a private company goes bankrupt, your pension could be at risk of being capped or reduced.

3. Mastering the Defined Contribution Plan (401k/403b)

The Defined Contribution plan is the engine of the modern American retirement strategy. It offers unparalleled flexibility, but it requires active management to be successful.

**The Advantages:**

* **Portability:** Your 401(k) is yours. If you change jobs, you can roll the balance into an IRA or your new employer’s plan.

* **Ownership and Legacy:** Unlike a pension, which typically ends when you and your spouse pass away, the remaining balance in a DC plan can be left to your heirs.

* **Tax Control:** You can choose between “Traditional” (tax-deductible now, taxed later) or “Roth” (taxed now, tax-free later) contributions.

**The Drawbacks:**

* **Longevity Risk:** The greatest fear in a DC plan is “running out of money.” If you live to 95 but your money only lasts until 85, you face a significant crisis.

* **Investment Risk:** A market crash the year before you retire can erase years of gains, a phenomenon known as “sequence of returns risk.”

* **The “Human” Element:** Many people under-contribute or make emotional decisions, like selling during a market dip, which can derail their progress.

**2026 Strategy:** For 2026, the IRS has adjusted contribution limits to account for inflation. Ensure you are taking full advantage of the updated limits ($24,000+ for individuals, with significantly higher catch-up limits for those over 50).

4. Maximizing SECURE 2.0 Provisions in 2026

By 2026, several key provisions of the SECURE 2.0 Act will be in full swing, fundamentally changing how you should interact with your retirement plans.

**Increased Catch-Up Limits:** If you are aged 60, 61, 62, or 63 in 2026, you can now take advantage of “super catch-up” contributions. For 2026, this limit is projected to be the greater of $10,000 or 150% of the standard catch-up amount. This is a critical window for those nearing retirement to bridge their savings gap.

**Automatic Enrollment and Escalation:** Most new 401(k) and 403(b) plans established after 2023 are required to automatically enroll employees. In 2026, check to see if your “automatic” contribution rate is high enough. Most experts suggest a total savings rate (including employer match) of 15% of your gross income.

**Emergency Savings Linked Accounts:** Many employers in 2026 now offer a “side-car” emergency fund within the 401(k). You can contribute up to $2,500 (indexed) on a Roth basis to this account, which remains accessible for emergencies without the usual 10% early withdrawal penalty. This allows you to save for retirement and emergencies simultaneously without fear of locking your money away.

5. The Hybrid Approach: Creating Your Own Pension

Many savvy investors in 2026 are using their Defined Contribution plans to “replicate” the security of a Defined Benefit plan. This is often necessary because the average Social Security check covers only about 40% of pre-retirement income.

**Step 1: The “Floor” Strategy.** Use your Social Security and any small pension you might have to cover your non-negotiable expenses (housing, utilities, food).

**Step 2: The Annuity Option.** Many 401(k) plans now offer “in-plan annuities.” You can move a portion of your DC balance into an annuity product that guarantees a lifetime income stream, essentially turning a piece of your 401(k) into a private pension.

**Step 3: The Bucket Method.** Keep 2-3 years of living expenses in cash or short-term bonds (the “Safety Bucket”) within your DC plan. This prevents you from having to sell stocks during a market downturn, providing the “stability” that a DB plan usually offers.

**Real-World Example:** Consider “Sarah,” a 45-year-old marketing manager. She has a 401(k) (DC plan) but misses the security of a pension. She decides to maximize her 401(k) match and then contributes to a Roth IRA. In 2026, she uses the new “catch-up” rules to accelerate her savings, planning to purchase a low-cost immediate annuity at age 67 to cover her base living costs. She has created a “synthetic pension” using a DC framework.

6. Calculating the “Retirement Gap” in 2026

To determine if your plan is sufficient, you must perform a gap analysis. With the cost of healthcare and housing remaining high in 2026, the old “80% of income” rule may be outdated.

1. **Estimate Expenses:** In 2026 dollars, what will your life cost? Factor in travel, healthcare (Medicare premiums and out-of-pocket costs), and taxes.

2. **Inventory Guaranteed Income:** Sum up your projected Social Security and any Defined Benefit pension amounts.

3. **Identify the Gap:** If your expenses are $8,000/month and your guaranteed income is $5,000/month, you have a $3,000 “gap.”

4. **The 4% Rule (Adjusted):** To fill a $3,000 monthly gap ($36,000/year), you would typically need a Defined Contribution balance of approximately $900,000 (based on the 4% withdrawal rule).

**Actionable Advice:** If your 2026 projection shows a gap that your current DC plan cannot fill, you must either increase contributions, delay retirement to increase your DB/Social Security payout, or reduce your retirement lifestyle expectations.

FAQ: Navigating the Nuances

**Q: Can I have both a Defined Benefit and a Defined Contribution plan?**

**A:** Yes! Many public sector employees have a pension (DB) and an optional 457(b) or 403(b) (DC). This is the “gold standard” of retirement security, as it provides both a guaranteed floor and growth potential.

**Q: What happens to my 401(k) if my company goes out of business?**

**A:** Your DC plan assets are held in a trust, separate from the company’s creditors. Your money is safe. For a DB pension, if the company goes under, the PBGC usually steps in to pay your benefits, though there are limits on the maximum amount they will cover.

**Q: Is “Vesting” different for DB and DC plans?**

**A:** Yes. In DC plans, your own contributions are always 100% yours. Employer matches often vest over 3 to 5 years. DB plans usually have a “cliff” vesting schedule, where you get nothing if you leave before 5 years, but 100% of the earned benefit once you hit that mark.

**Q: Which plan is better for inflation protection?**

**A:** Generally, a DC plan is better because you can invest in equities (stocks), which historically outpace inflation. DB plans are often fixed, meaning the “real” value of your check drops every year unless your plan includes a COLA.

**Q: Should I take a “Lump Sum” if my pension offers it?**

**A:** This is a major decision in 2026. A lump sum gives you control and a legacy for heirs (like a DC plan), but you lose the lifetime guarantee. If you are in poor health, a lump sum might be better. If you expect to live to 100, the monthly annuity is usually superior.

Conclusion: Taking Control of Your Financial Timeline

The debate between Defined Benefit and Defined Contribution plans isn’t about which one is “better” in a vacuum; it’s about which one empowers you to meet your specific life goals. In 2026, the reality is that the majority of the burden for retirement success has shifted to the individual. If you are fortunate enough to have a Defined Benefit pension, view it as the foundation of your house—stable and reliable. If you rely on a Defined Contribution plan, view it as the engine—capable of high performance but requiring regular maintenance and fuel.

To thrive in this environment, you must be proactive. Audit your plans today: ensure you are meeting your employer match, take advantage of the 2026 “super catch-up” limits if eligible, and always account for the eroding power of inflation. Retirement security in 2026 isn’t a result of luck; it’s a result of understanding the tools at your disposal and using them with discipline. Whether you are building a “piggy bank” or waiting for a “paycheck,” the time to optimize your strategy is now.