Understanding Dollar-Cost Averaging: A Foundation for Prudent Investing

At its core, dollar-cost averaging (DCA) is an investment strategy where an investor commits to investing a fixed amount of money at regular intervals, regardless of the asset’s price fluctuations. This systematic approach means you buy more shares when prices are low and fewer shares when prices are high, effectively averaging out your purchase price over time. Instead of attempting to predict market peaks and troughs, DCA embraces the inherent volatility of the market, turning it into an advantage rather than a source of anxiety.

Imagine the stock market as a roller coaster – full of ups and downs. A market timer tries to jump on just before a big climb and get off right at the peak. A dollar-cost averager, however, simply buckles in for the entire ride, making consistent contributions throughout the journey. This strategy is particularly powerful because it removes the temptation to time the market, a feat that academic research and historical data consistently show is incredibly difficult, if not impossible, to achieve consistently. By automating your investments, DCA transforms market volatility from a source of fear into an opportunity to accumulate more assets at potentially lower average prices.

The beauty of DCA lies in its simplicity and its psychological benefits. It promotes a disciplined investment habit, encouraging regular savings and a long-term perspective. This systematic approach helps investors avoid the common pitfalls of emotional investing, such as buying high out of euphoria or selling low out of fear. Instead, it fosters a steady, unwavering commitment to growth, making it a cornerstone strategy for individuals and families aiming to How To Build Generational Wealth over decades. In essence, dollar-cost averaging is not about getting rich quickly; it’s about getting rich reliably and sustainably.

The Mechanics of Dollar-Cost Averaging: How It Works in Practice

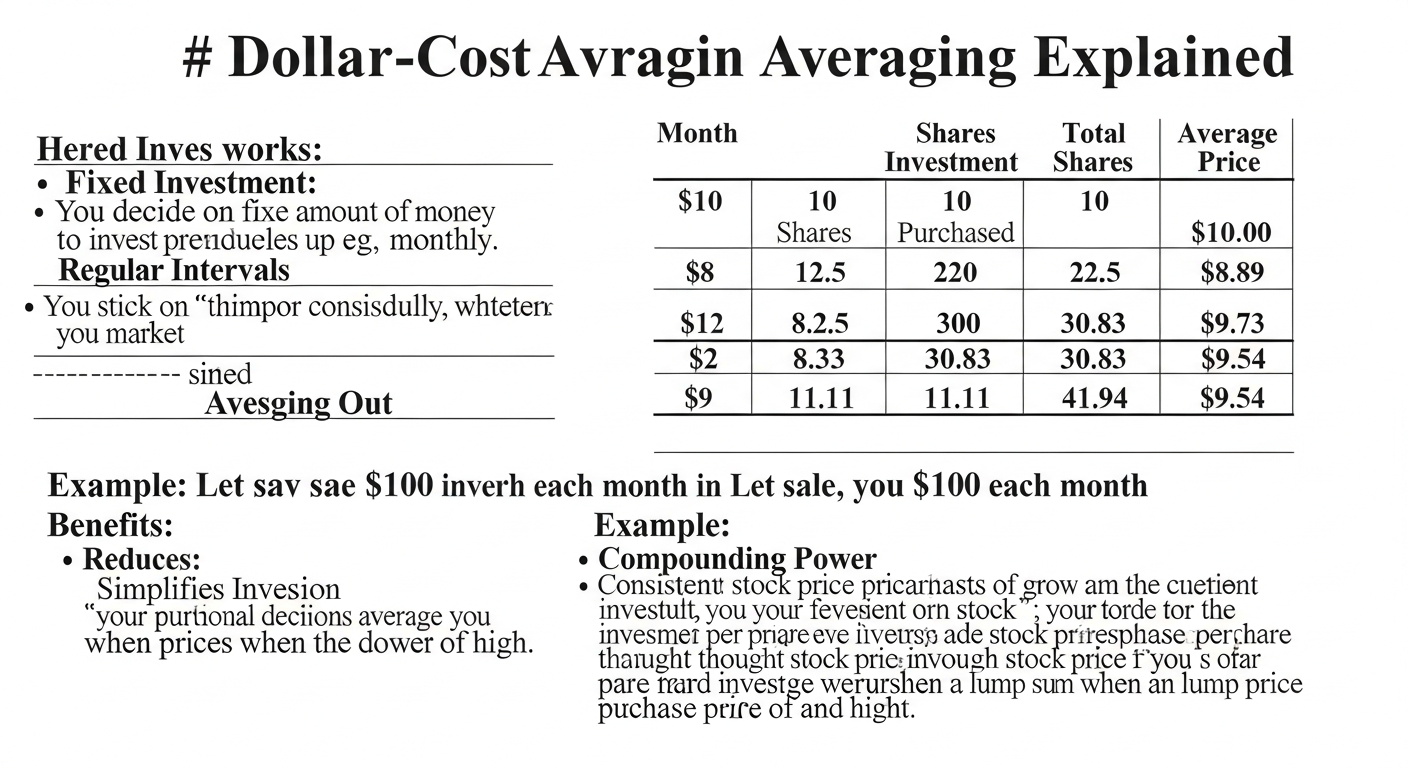

To truly grasp the power of dollar-cost averaging, it’s helpful to walk through a practical example. Let’s consider an investor, Sarah, who decides to invest $200 every month into a specific exchange-traded fund (ETF) over a six-month period, starting in January 2026. The price of this ETF fluctuates as follows:

- January 2026: ETF price is $10 per share. Sarah invests $200, buying 20 shares ($200 / $10).

- February 2026: ETF price drops to $8 per share. Sarah invests $200, buying 25 shares ($200 / $8).

- March 2026: ETF price rises to $12 per share. Sarah invests $200, buying 16.67 shares ($200 / $12).

- April 2026: ETF price drops again to $9 per share. Sarah invests $200, buying 22.22 shares ($200 / $9).

- May 2026: ETF price recovers to $11 per share. Sarah invests $200, buying 18.18 shares ($200 / $11).

- June 2026: ETF price is $10.50 per share. Sarah invests $200, buying 19.05 shares ($200 / $10.50).

After six months, let’s analyze Sarah’s investment:

- Total Invested: $200/month x 6 months = $1,200

- Total Shares Purchased: 20 + 25 + 16.67 + 22.22 + 18.18 + 19.05 = 121.12 shares

- Average Cost Per Share: $1,200 / 121.12 shares = $9.91 per share

Now, let’s compare this to the simple average of the share prices over the same period: ($10 + $8 + $12 + $9 + $11 + $10.50) / 6 = $10.08 per share. Notice that Sarah’s average cost per share ($9.91) is lower than the average market price ($10.08). This is the core benefit of dollar-cost averaging: by consistently investing a fixed amount, you naturally buy more shares when prices are lower, thereby reducing your overall average purchase price. This effect, often referred to as “averaging down,” significantly enhances potential returns when the market eventually recovers and grows.

This systematic approach works across various investment vehicles, from individual stocks and exchange-traded funds (ETFs) to mutual funds and retirement accounts like 401(k)s and IRAs. The key is setting up automatic contributions, which ensures discipline and consistency. This consistency is intrinsically linked to effective personal finance management. To successfully implement DCA, an investor must first have a clear understanding of their financial inflows and outflows. This highlights the critical importance of knowing How To Create A Monthly Budget. A well-structured budget allows you to identify a fixed amount you can realistically commit to investing each month, ensuring that your DCA strategy is sustainable and doesn’t strain your finances. Without a budget, consistent contributions can become a challenge, undermining the very principle of DCA.

The Psychological Edge: Taming Emotional Investing with DCA

Dollar-cost averaging offers a powerful antidote to this emotional volatility. By automating regular investments, DCA effectively removes the human element of decision-making from the equation. You are no longer tasked with the stressful and often futile exercise of trying to predict market movements. Instead, your investment strategy is governed by a predetermined schedule and amount, regardless of whether the market is up, down, or flat. This disciplined approach insulates investors from the urge to make impulsive decisions based on daily news headlines or short-term market fluctuations.

Consider the typical investor’s dilemma: a market dip often feels like a crisis, prompting many to pull their money out. However, for the dollar-cost averager, a dip is simply an opportunity to acquire more shares at a lower price, knowing that these additional shares will contribute significantly to long-term gains when the market inevitably recovers. This psychological reframe is invaluable. It transforms periods of market uncertainty, which typically induce anxiety, into moments of strategic advantage. Rather than feeling the stress of “losing money,” a DCA investor can take comfort in the knowledge that their systematic contributions are accumulating assets at a discount.

Moreover, DCA fosters a long-term mindset. It encourages investors to focus on the compounding power of their investments over years and decades, rather than fixating on short-term gains or losses. This perspective is crucial for building substantial wealth and achieving significant financial milestones, such as retirement or even How To Build Generational Wealth. By consistently investing, you allow your money to work for you over time, benefiting from market growth without the psychological burden of trying to outsmart it. This steadfast approach mirrors the discipline required in other areas of personal finance, such as diligently paying down debt using methods like the Snowball Vs Avalanche Debt Payoff Method, where consistent, unemotional execution is key to success.

Weighing the Scales: Advantages and Potential Limitations of Dollar-Cost Averaging

While dollar-cost averaging is lauded for its simplicity and psychological benefits, it’s crucial to understand both its strengths and its potential drawbacks to determine if it aligns with your personal financial strategy for 2026 and beyond.

Key Advantages of Dollar-Cost Averaging:

- Mitigates Risk of Investing at a Peak: The primary benefit is reducing the risk of investing a large sum just before a market downturn. By spreading out your investments, you avoid the potential devastation of putting all your capital in at the highest point.

- Capitalizes on Volatility: DCA thrives in volatile markets. When prices are low, your fixed investment buys more shares; when prices are high, it buys fewer. Over time, this averages out your purchase price, often resulting in a lower average cost per share than the average market price.

- Promotes Investment Discipline: Automating regular investments instills a consistent savings habit. This passive approach removes the need for active decision-making, ensuring you stick to your investment plan even when market sentiment is negative.

- Reduces Emotional Decision-Making: As discussed, DCA acts as a powerful barrier against fear and greed, preventing impulsive buying or selling that typically harms long-term returns.

- Accessible to All Investors: You don’t need a large lump sum to start. Even small, regular contributions can grow significantly over time thanks to the power of compounding and DCA. This makes it an ideal strategy for beginners or those with limited disposable income.

- Simplicity: It’s easy to understand and implement, making it a favorite for set-it-and-forget-it investors.

Potential Limitations of Dollar-Cost Averaging:

- Potential Underperformance in Consistently Rising Markets: In a prolonged bull market where prices steadily increase, a lump-sum investment made at the beginning would typically outperform DCA. By waiting and spreading out investments, a DCA strategy might miss out on some early gains in an upward trend. This is often cited as the main argument against DCA in certain market conditions.

- Higher Transaction Costs (Historically): In the past, frequent trades associated with DCA could accumulate significant transaction fees. However, with the rise of commission-free trading platforms for stocks, ETFs, and many mutual funds, this limitation has largely diminished for most retail investors.

- Requires Discipline: While it helps prevent emotional decisions, the investor still needs the discipline to commit to the regular contributions, especially during prolonged downturns when the temptation to stop investing is strongest.

- Does Not Guarantee Profits: DCA is a risk management strategy, not a profit guarantee. While it aims to reduce average purchase price, the overall market still needs to perform well for your investments to grow. If an asset consistently declines over a very long period, DCA will not prevent losses, though it may mitigate their severity compared to a lump-sum investment.

Ultimately, the effectiveness of dollar-cost averaging depends on market conditions and individual investor psychology. For the average investor seeking a straightforward, stress-reducing path to long-term wealth accumulation, its advantages often outweigh its potential drawbacks, especially when viewed through the lens of behavioral finance.

Implementing Dollar-Cost Averaging: Integrating DCA into Your Financial Blueprint

Successfully integrating dollar-cost averaging into your financial strategy for 2026 and beyond requires more than just understanding the concept; it demands practical implementation within a broader financial plan. DCA works best when it’s a consistent, automated component of your overall wealth-building journey.

Practical Steps for Implementing DCA:

- Determine Your Investment Amount: The first step is to figure out how much you can comfortably invest regularly. This is where the discipline of How To Create A Monthly Budget becomes indispensable. A detailed budget helps you identify surplus income after covering essential expenses and debt obligations. By knowing your financial capacity, you can commit to a realistic and sustainable investment amount, whether it’s $50, $200, or $1,000 per month.

- Choose Your Investment Vehicle: Decide what you want to invest in. Common choices for DCA include broad-market index funds (ETFs or mutual funds) that track major indices like the S&P 500, individual stocks (though diversification is key here), or target-date funds within retirement accounts. Diversification is crucial to reduce specific asset risk.

- Select an Investment Platform: Open an account with a brokerage firm (e.g., Fidelity, Vanguard, Charles Schwab, Robinhood, M1 Finance) or utilize your employer-sponsored retirement plan (401(k), 403(b)). Many platforms offer commission-free trading for ETFs and stocks, making DCA more cost-effective.

- Set Up Automatic Investments: This is the cornerstone of DCA. Configure your account to automatically transfer your predetermined investment amount from your bank account to your investment account on a specific date each month or pay period. This automation ensures consistency and removes the psychological hurdle of manually initiating transfers.

- Review and Adjust Periodically: While DCA is largely passive, it’s wise to review your strategy annually. As your income grows, consider increasing your monthly contribution. Also, ensure your chosen investments still align with your risk tolerance and long-term goals.

Contextualizing DCA within Your Broader Financial Plan:

DCA is a powerful tool, but it’s part of a larger financial ecosystem. Before aggressively pursuing investments, ensure you have a solid financial foundation:

- Emergency Fund First: Always prioritize building an emergency fund of 3-6 months’ worth of living expenses. This provides a financial safety net, preventing you from having to sell investments prematurely during unforeseen circumstances.

- Debt Management: High-interest debt can quickly erode any investment gains. Before or alongside your DCA strategy, address high-interest consumer debt. Understanding and implementing debt payoff methods like the Snowball Vs Avalanche Debt Payoff Method can free up significant capital that can then be redirected towards consistent investing. For example, if you have credit card debt at 20% interest, paying that off is a guaranteed 20% return, which is hard to beat in the market.

- Long-Term Goals: DCA is particularly effective for long-term goals such as retirement planning, saving for a down payment on a house, or contributing to a child’s education fund. It’s a foundational strategy for anyone aspiring to How To Build Generational Wealth. By consistently investing over decades, the compounding effect of returns on your average-cost shares can lead to substantial wealth accumulation that can be passed down. Think of it as planting a tree; consistent watering (DCA) over many years leads to a mighty oak.

By thoughtfully integrating dollar-cost averaging into a comprehensive financial blueprint, you harness its power for consistent growth while ensuring other critical financial bases are covered. This holistic approach sets the stage for enduring financial success.

DCA vs. Lump Sum: A Strategic Comparison for Different Market Realities

When an investor has a significant sum of money available for investment—perhaps from an inheritance, a bonus, or the sale of an asset—a common dilemma arises: should they invest it all at once (lump sum investing) or spread it out over time using dollar-cost averaging? This is a critical strategic decision, and the “best” approach often depends on market conditions, an investor’s risk tolerance, and their personal financial situation.

Understanding Lump Sum Investing:

Lump sum investing involves deploying all available capital into the market at a single point in time. The primary argument in favor of lump-sum investing is based on the principle of “time in the market beats timing the market.” Historically, equity markets have tended to trend upwards over the long term. Therefore, the sooner your money is invested, the longer it has to compound and generate returns. Numerous studies, including those by Vanguard, have shown that over various historical periods, lump-sum investing has statistically outperformed dollar-cost averaging approximately two-thirds of the time when markets are generally rising.

The reasoning is straightforward: if the market generally goes up, then investing all your money immediately allows it to capture those upward movements from the earliest possible point. Any waiting period (as with DCA) means potentially missing out on gains.

When DCA Shines:

While historical data often favors lump sum, DCA isn’t without its merits, particularly for certain investor profiles and market conditions:

- Volatile or Bear Markets: In periods of high market volatility or during a bear market, DCA truly shines. By spreading out investments, you reduce the risk of deploying a large sum right before a significant downturn. During a bear market, DCA allows you to buy more shares at progressively lower prices, setting you up for substantial gains when the market eventually recovers. The psychological comfort of not having to worry about market timing is immense during these stressful periods.

- Risk Aversion: For investors who are particularly risk-averse or those who struggle with the emotional impact of market fluctuations, DCA provides a sense of security. It lessens the anxiety of potentially investing at a market peak, making the investment journey more palatable.

- Gradual Accumulation of Funds: For most individuals, funds become available gradually through regular paychecks. In such cases, DCA is the natural and practical approach, as a large lump sum isn’t available. This is the default mode for 401(k) contributions, for example.

The Strategic Balance:

The choice between DCA and lump sum is not always black and white. Here’s a nuanced perspective:

- Behavioral Aspect: Even if lump sum investing has a historical edge, many investors simply cannot stomach the risk of deploying a massive sum into a volatile market. The psychological comfort and discipline offered by DCA can lead to better adherence to an investment plan, which in itself is a critical factor for long-term success. An investor who sticks to a DCA plan is likely to fare better than one who attempts a lump sum, panics during a dip, and sells prematurely.

- Hybrid Approaches: For those with a large sum but high risk aversion, a hybrid approach might be considered. This involves investing a significant portion as a lump sum and then dollar-cost averaging the remainder over a shorter period (e.g., 3-6 months) to capture some early gains while mitigating the immediate downside risk.

- Long-Term Horizon: Over very long investment horizons (20+ years), the difference in returns between DCA and lump sum tends to diminish. The power of compounding over decades often smooths out the initial entry point differences. This makes DCA a robust strategy for long-term goals like How To Build Generational Wealth, where consistency and compounding are paramount.

In summary, while historical data might lean towards lump sum in consistently rising markets, dollar-cost averaging remains a powerful, psychologically sound, and practical strategy for most investors, particularly those building wealth over time, navigating volatile markets, or prioritizing peace of mind over potentially marginal statistical outperformance.

Optimizing Your DCA Strategy: Maximizing Long-Term Growth with Informed Decisions

Implementing dollar-cost averaging is an excellent start, but optimizing your strategy can further enhance its effectiveness and align it more closely with your long-term financial objectives. It’s about making informed decisions within the DCA framework to maximize growth and ensure resilience, especially as we look towards 2026 and beyond.

Frequency of Investment:

The most common DCA frequency is monthly, aligning with typical pay cycles. However, some investors opt for bi-weekly or even weekly contributions. While more frequent investments might slightly refine your average purchase price by capturing more subtle market fluctuations, the difference in long-term returns compared to monthly contributions is often negligible for most investors. The key is consistency and what is practical for your budget and investment platform. For instance, if your platform has per-trade fees (though less common now), very frequent small trades might eat into returns. For most, a monthly cadence is ideal, easily managed alongside a well-structured How To Create A Monthly Budget.

Investment Selection and Diversification:

DCA is a strategy for investing, not a guarantee of returns from any specific asset. Therefore, what you invest in is just as important as how you invest. Avoid dollar-cost averaging into a single, highly speculative stock. Instead, focus on a diversified portfolio. Broad-market index funds (ETFs or mutual funds) that track major indices (like the S&P 500 or a total world stock market index) are excellent choices. They offer instant diversification across hundreds or thousands of companies, reducing the risk associated with individual stock performance. For those aiming to How To Build Generational Wealth, a diversified, low-cost portfolio is paramount, as it provides stable, long-term growth potential.

Adjusting Contributions as Income Grows:

Your financial situation is not static. As your career progresses and your income increases, make it a habit to revisit and increase your regular DCA contributions. This simple act can significantly accelerate your wealth accumulation through the power of compounding. Many employer-sponsored plans allow for automatic increases in contribution percentages each year, which is an excellent way to “set it and forget it” for growth. Regular budget reviews (as part of your How To Create A Monthly Budget process) should include an assessment of whether you can allocate more to investments.

Rebalancing Your Portfolio:

Even with a consistent DCA strategy, your portfolio’s asset allocation can drift over time due to differing returns from various asset classes. For example, if stocks significantly outperform bonds, your portfolio might become overweighted in stocks, increasing its risk profile. Periodically (e.g., annually or semi-annually), consider rebalancing your portfolio to bring it back to your target asset allocation. This might involve selling some of your outperforming assets and buying more of your underperforming ones, or simply directing your new DCA contributions towards the underweighted assets. Rebalancing ensures your portfolio’s risk level remains consistent with your comfort level.

Staying the Course During Downturns:

The true test of a dollar-cost averaging strategy comes during market downturns. It is precisely when the market is falling that DCA is most effective, as you are buying more shares at lower prices. The temptation to stop investing or, worse, to sell, will be strong. Resist this urge. Remember the psychological benefits of DCA: it removes emotion. Sticking to your plan during bear markets is critical for capturing the subsequent recovery and maximizing your long-term returns. This resilience is a hallmark of successful investors aiming for substantial, generational wealth.

By thoughtfully applying these optimization techniques, your dollar-cost averaging strategy will evolve from a simple investment method into a sophisticated engine for sustained financial growth, making it a cornerstone of your journey towards financial independence and lasting prosperity in 2026 and beyond.

Frequently Asked Questions

Is dollar-cost averaging always the best strategy?▾

How often should I dollar-cost average?▾

Can dollar-cost averaging be used for retirement accounts?▾

What are the risks associated with dollar-cost averaging?▾

Does dollar-cost averaging work in a bear market?▾

Is dollar-cost averaging suitable for large sums of money?▾

Recommended Resources

Related reading: Inbound Marketing Vs Outbound Marketing Which Is Better (Kacerr).

You might also enjoy How To Invest In Etfs For Beginners from Trading Costs.