Understanding the Fundamentals: What Are Mutual Funds?

At their core, mutual funds represent a pooled investment vehicle managed by professional fund managers. When you invest in a mutual fund, you are essentially buying shares of a portfolio that typically includes stocks, bonds, and other securities. The money from thousands of investors is combined, allowing the fund to invest in a much broader and more diversified range of assets than an individual investor could typically achieve on their own. This inherent diversification is one of the most compelling advantages of mutual funds, as it helps to spread risk across various companies and sectors.

The operational structure of mutual funds is quite distinct. Unlike individual stocks that trade throughout the day, mutual fund shares are priced only once per day, after the market closes. This price is known as the Net Asset Value (NAV), which is calculated by taking the total value of all assets in the fund, subtracting liabilities, and dividing by the number of outstanding shares. When you buy or sell mutual fund shares, the transaction is executed at that day’s closing NAV. This means you won’t know the exact price of your purchase or sale until after the market has closed.

Types of Mutual Funds

- Equity Funds: These primarily invest in stocks and are categorized further by company size (large-cap, mid-cap, small-cap), growth potential (growth funds, value funds), or geographic focus (international, emerging markets).

- Bond Funds: Investing in fixed-income securities, bond funds aim to provide income and stability. They vary by bond type (government, corporate, municipal), maturity (short-term, intermediate-term, long-term), and credit quality.

- Money Market Funds: Designed for liquidity and capital preservation, these funds invest in short-term, low-risk debt instruments. They are often used as a cash management tool.

- Balanced Funds: These funds invest in a mix of stocks and bonds, aiming for a balance of growth and income. The asset allocation typically remains relatively stable.

- Index Funds: A specific type of mutual fund that tracks a particular market index, such as the S&P 500. These are passively managed and aim to replicate the performance of their benchmark.

Pros of Mutual Funds

- Professional Management: For investors who prefer a hands-off approach, mutual funds offer the expertise of professional fund managers who conduct research, make investment decisions, and monitor the portfolio.

- Diversification: By pooling money, mutual funds can invest in a wide array of securities, reducing the impact of any single poorly performing asset on the overall portfolio.

- Convenience: They simplify investing by providing a ready-made portfolio, saving investors the time and effort of researching and selecting individual securities. Many offer automatic investment plans.

- Accessibility: With relatively low minimum initial investments for some funds, they are accessible to a broad range of investors.

Cons of Mutual Funds

- Higher Fees: Especially actively managed funds, mutual funds often come with higher expense ratios (annual fees) compared to their passively managed counterparts. They may also levy sales charges (loads) or other administrative fees.

- Lack of Trading Flexibility: Transactions only occur once per day at NAV, meaning investors cannot react to intra-day market fluctuations.

- Tax Inefficiency: Actively managed funds often have high portfolio turnover, which can lead to frequent capital gains distributions. These distributions are taxable to investors, even if they don’t sell their shares, potentially creating an unexpected tax liability.

- Potential for Underperformance: While professional management is a pro, it’s also true that many actively managed funds fail to consistently outperform their benchmark indexes after fees.

Mutual funds have long been a cornerstone of retirement planning and long-term investing, particularly for those who value professional oversight and broad market exposure without the need for active trading. They represent a straightforward path to diversification, making them a suitable option for investors building their wealth over decades, much like those planning to How To Build Generational Wealth.

Understanding the Fundamentals: What Are Exchange-Traded Funds (ETFs)?

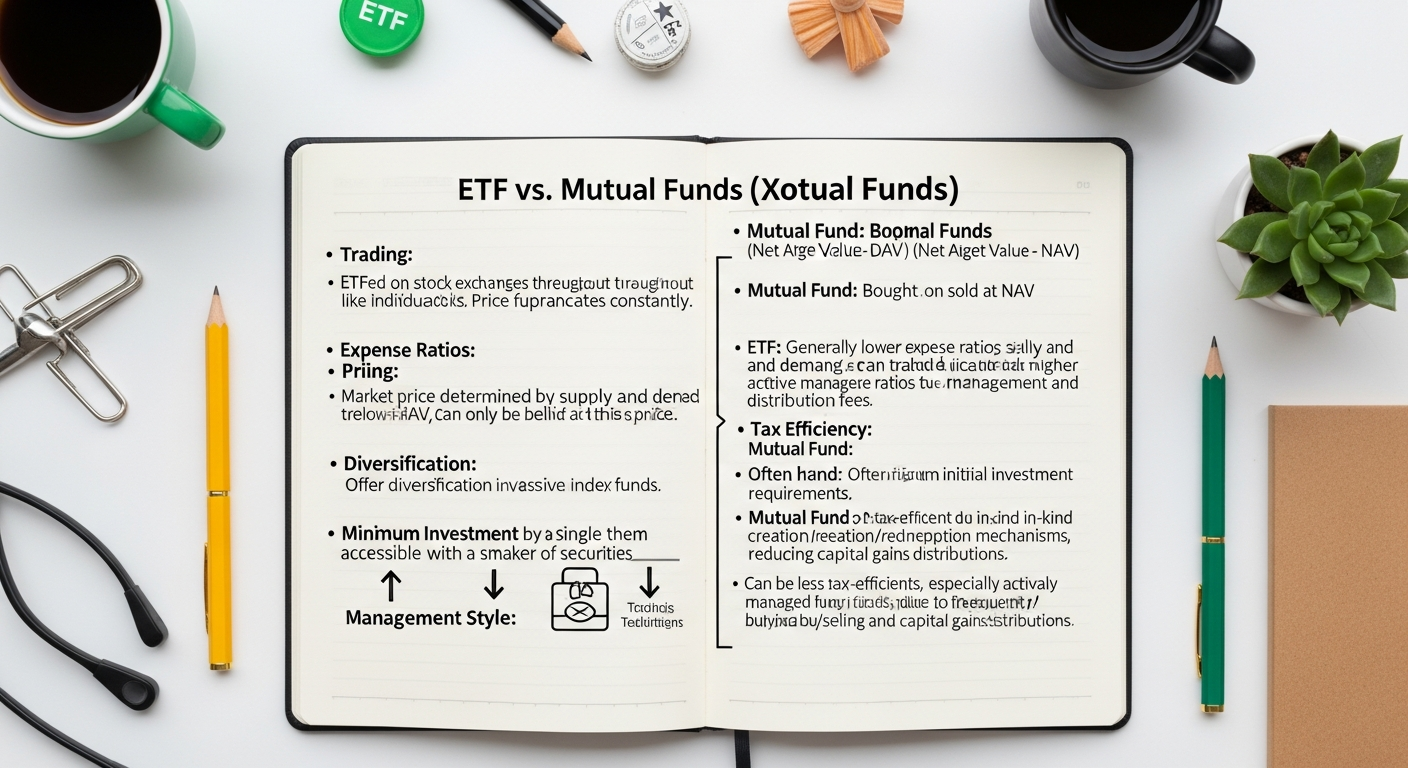

Exchange-Traded Funds (ETFs) emerged as a revolutionary investment product, combining features of both mutual funds and individual stocks. Like mutual funds, ETFs pool money from investors to build a diversified portfolio of securities. However, their key distinguishing feature is their ability to be bought and sold on stock exchanges throughout the trading day, much like individual stocks. This real-time trading flexibility is a significant departure from the once-a-day pricing of mutual funds.

ETFs typically track an underlying index, such as the S&P 500, a specific industry sector, a commodity, or even a foreign market. This makes most ETFs passively managed, meaning their objective is simply to mirror the performance of their chosen benchmark, rather than trying to beat it. Because they don’t require extensive research and frequent trading decisions by a fund manager, their operational costs are generally lower than those of actively managed mutual funds.

When you buy an ETF, you are purchasing shares on an exchange from another investor, or potentially from a market maker who facilitates trading. The price of an ETF share fluctuates throughout the day based on supply and demand, and it may trade at a slight premium or discount to its underlying Net Asset Value (NAV). This difference, known as the bid-ask spread, is typically very small for highly liquid ETFs.

Types of ETFs

- Index ETFs: The most common type, these track broad market indexes (e.g., S&P 500), specific sectors (e.g., technology, healthcare), or international markets.

- Bond ETFs: Provide exposure to various types of bonds, similar to bond mutual funds, but with the added trading flexibility.

- Commodity ETFs: Invest in physical commodities (like gold or oil) or commodity futures contracts.

- Currency ETFs: Track the performance of individual currencies or baskets of currencies.

- Actively Managed ETFs: While less common than index ETFs, these funds employ a fund manager to make active investment decisions, similar to actively managed mutual funds, but still trade on an exchange.

- Leveraged/Inverse ETFs: Designed for short-term trading, these use derivatives to amplify returns (leveraged) or profit from market declines (inverse). They carry significantly higher risk and are not suitable for most long-term investors.

Pros of ETFs

- Lower Costs: Due to their generally passive management style, ETFs typically have significantly lower expense ratios compared to actively managed mutual funds. Many brokerages also offer commission-free trading for a wide selection of ETFs, further reducing costs.

- Trading Flexibility: ETFs can be bought and sold throughout the trading day at market prices, allowing investors to react quickly to market news or adjust their portfolios. This makes them attractive for both long-term investors and those with a more tactical approach.

- Tax Efficiency: ETFs are generally more tax-efficient than mutual funds due to their unique “in-kind” creation and redemption mechanism. This often allows them to avoid distributing capital gains to shareholders, reducing taxable events for investors.

- Diversification: Like mutual funds, ETFs offer instant diversification across a basket of securities with a single purchase.

- Transparency: Most ETFs disclose their portfolio holdings daily, providing investors with a clear view of what they own.

Cons of ETFs

- Trading Costs: While many are commission-free, some ETFs may still incur brokerage commissions, especially for less common funds. The bid-ask spread also represents a small transaction cost. Frequent trading can accumulate these costs.

- No Professional Management (for index ETFs): For investors seeking active oversight and stock-picking expertise, most index ETFs will not provide this. Their goal is merely to track an index.

- Potential for Over-Trading: The ease of buying and selling can tempt some investors into excessive trading, which can lead to higher transaction costs and potentially poorer performance due to market timing attempts.

- Complexity of Certain Types: Leveraged and inverse ETFs are highly complex and risky, often leading to significant losses for inexperienced investors.

ETFs have rapidly grown in popularity, offering a versatile tool for investors seeking low-cost, diversified exposure to various markets with the flexibility of stock trading. They are particularly favored by those implementing strategies focused on cost efficiency and market-tracking, forming a core component of many long-term investment plans aimed at building substantial wealth over time.

The Core Differences: Trading and Liquidity

Mutual Funds: End-of-Day Pricing and Direct Transactions

When you decide to buy or sell shares of a mutual fund, your transaction is executed directly with the fund company (or through an intermediary like a brokerage firm that acts on behalf of the fund). This means there’s no secondary market where investors trade shares among themselves. Instead, new shares are created when investors buy, and existing shares are redeemed (destroyed) when investors sell.

- Once-a-Day Pricing: As discussed, mutual fund shares are priced only once per day, after the close of the major stock exchanges. The price you pay or receive is the fund’s Net Asset Value (NAV) per share, calculated based on the closing prices of all the securities held within the fund’s portfolio.

- Order Execution: If you place an order to buy or sell a mutual fund at 10 AM, you won’t know the exact price until after 4 PM ET. All buy and sell orders placed during a given trading day are executed at the same NAV. This structure prevents investors from trying to profit from intra-day market fluctuations.

- Liquidity: Mutual funds are generally highly liquid in the sense that you can always redeem your shares at the current NAV. However, this redemption process can take a day or two to settle, meaning the cash may not be immediately available.

- Market Impact: Individual purchases or sales of mutual fund shares directly impact the fund’s cash flows and portfolio management. Large redemptions, for example, might force a fund manager to sell securities, potentially at an inopportune time.

ETFs: Real-Time Trading and Exchange-Based Transactions

ETFs, by contrast, behave much like individual stocks. They are listed on major stock exchanges and can be bought and sold throughout the trading day whenever the markets are open. This characteristic brings with it a host of implications for investors.

- Real-Time Pricing: The price of an ETF share fluctuates constantly throughout the day, driven by supply and demand dynamics, just like any stock. You can see the current market price and execute trades at that price in real-time.

- Order Execution: When you place an order for an ETF, it is executed almost immediately at the prevailing market price. This allows investors to react swiftly to news, economic data, or changes in their personal financial situation. This flexibility can be particularly appealing for those who regularly monitor their investments or have specific market timing strategies.

- Liquidity: ETF liquidity is determined by two factors: the liquidity of the underlying securities and the activity of market makers. For popular ETFs, the bid-ask spread (the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept) is often very narrow, indicating high liquidity. Less popular ETFs might have wider spreads, leading to higher implicit transaction costs.

- Market Makers and Arbitrage: A unique aspect of ETFs is the role of “authorized participants” (APs) and market makers. These entities create and redeem large blocks of ETF shares directly with the fund provider, a process known as “in-kind” creation/redemption. This mechanism helps keep an ETF’s market price closely aligned with its underlying NAV through an arbitrage process. If an ETF trades significantly above its NAV, APs can buy the underlying securities, create new ETF shares, and sell them on the open market for a profit, bringing the price back down. Conversely, if it trades below NAV, APs can buy ETF shares, redeem them for the underlying securities, and sell those securities, pushing the ETF’s price up. This mechanism is crucial for the efficient functioning and pricing of ETFs.

Implications for Investors

The difference in trading mechanisms dictates vastly different investor experiences:

- For investors who prefer a hands-off approach, setting up regular contributions (e.g., monthly How To Create A Monthly Budget for investing) and not worrying about daily market swings, the end-of-day pricing of mutual funds can be simpler. You commit to a specific dollar amount, and you receive shares based on the day’s closing NAV. This is ideal for dollar-cost averaging.

- For those who value precision in entry and exit points, or who wish to implement tactical trading strategies, ETFs offer superior flexibility. You can place limit orders, stop-loss orders, and other advanced order types, giving you more control over the price at which your trades are executed.

- It’s also worth noting that the ability to trade ETFs like stocks can be a double-edged sword. While it offers flexibility, it can also tempt some investors into excessive trading, which often leads to higher transaction costs and potentially suboptimal returns over the long run. Investors need discipline to use this flexibility wisely.

Ultimately, the choice between the two often comes down to an investor’s preferred level of engagement and their investment strategy. Do you prefer to set it and forget it, or do you want the option to be more active in managing your portfolio throughout the day?

Cost Structures and Fees: A Critical Comparison

When evaluating any investment vehicle, understanding its cost structure is paramount. Fees, even seemingly small ones, can significantly erode your returns over time. The differences in fees between mutual funds and ETFs are often stark and represent one of the primary reasons investors choose one over the other.

Mutual Fund Fees

Mutual funds, particularly actively managed ones, are notorious for having a more complex and generally higher fee structure. These fees can be broadly categorized into two main types:

- Sales Charges (Loads):

- Front-End Load (Class A Shares): A commission paid at the time of purchase, typically ranging from 3% to 5.75% of your investment. If you invest $10,000 with a 5% front-end load, only $9,500 is actually invested.

- Back-End Load (Class B Shares): Also known as a contingent deferred sales charge (CDSC), this is a fee paid when you sell your shares, usually within a certain period (e.g., 5-7 years). The fee typically declines over time until it disappears.

- Level Load (Class C Shares): These funds often have no front-end or back-end load but charge a higher annual 12b-1 fee and sometimes a small redemption fee.

- No-Load Funds: These funds do not charge any sales commissions. They are generally preferred by cost-conscious investors, though they still have ongoing operating expenses.

- Operating Expenses (Expense Ratio):

This is the most critical ongoing fee and is expressed as a percentage of the fund’s assets each year. The expense ratio includes:

- Management Fees: Paid to the fund manager for their investment expertise and services. This is typically the largest component.

- Administrative Fees: For record-keeping, shareholder services, and other operational costs.

- 12b-1 Fees: Annual fees used to cover marketing and distribution costs. These are typically associated with loaded funds or Class C shares.

Actively managed mutual funds often have expense ratios ranging from 0.50% to over 2.00% annually. Index mutual funds, being passively managed, typically have much lower expense ratios, often below 0.20%.

- Other Potential Fees:

- Redemption Fees: A small fee charged if you sell shares too quickly after purchasing them, designed to deter short-term trading.

- Exchange Fees: For switching between funds within the same family.

ETF Fees

ETFs generally boast a simpler and significantly lower fee structure, which is a major draw for many investors.

- Expense Ratio:

This is the primary ongoing cost for an ETF. Because most ETFs are passively managed (tracking an index), they don’t incur the high research and management costs of actively managed mutual funds. Consequently, their expense ratios are often remarkably low, frequently ranging from 0.03% to 0.25% for broad market index ETFs. Even some specialized or actively managed ETFs tend to have lower expense ratios than their mutual fund counterparts.

- Brokerage Commissions:

Since ETFs trade like stocks, you traditionally paid a brokerage commission for each buy or sell order. However, in recent years, many major brokerage firms have eliminated commissions for a vast selection of ETFs, making them even more cost-effective for frequent traders or small transactions. For ETFs that still incur commissions, these are typically flat fees per trade (e.g., $0 to $7).

- Bid-Ask Spread:

This is an implicit transaction cost. When you buy an ETF, you pay the “ask” price, which is slightly higher than the “bid” price you receive when you sell. The difference is the bid-ask spread. For highly liquid ETFs, this spread is usually fractions of a penny, making it negligible. For less frequently traded ETFs, the spread can be wider, adding a small cost to each transaction.

The Long-Term Impact of Fees

The seemingly small percentage differences in expense ratios can have a dramatic impact on your investment returns over decades. Consider two funds, both returning 7% annually before fees. Fund A has a 1.5% expense ratio, while Fund B has a 0.15% expense ratio. Over 30 years, an initial $10,000 investment would grow substantially more in Fund B. The difference compounds, meaning a higher fee not only reduces your annual return but also reduces the base on which future returns are calculated. This principle underscores the importance of being mindful of costs as you plan your monthly budget for investments.

For investors focused on long-term growth and building generational wealth, minimizing fees is a powerful strategy. The lower costs associated with most ETFs mean more of your money remains invested and working for you, leading to greater compounding over time. This aligns perfectly with a disciplined approach to personal finance, much like strategically tackling debt using the Snowball Vs Avalanche Debt Payoff Method – both require a clear understanding of financial mechanics to achieve optimal outcomes.

Management Style and Investment Strategy

The approach a fund takes to manage its portfolio is another crucial differentiator between mutual funds and ETFs, influencing everything from potential returns to overall costs and tax efficiency. This distinction primarily revolves around active management versus passive management.

Actively Managed Funds

Traditionally, most mutual funds have been actively managed. In an actively managed fund, a team of professional fund managers and analysts constantly researches, buys, and sells securities with the goal of outperforming a specific market benchmark (e.g., the S&P 500). Their objective is to generate “alpha,” or excess returns above the market, by making strategic investment decisions based on their expertise, market outlook, and proprietary research.

- Human Expertise: Investors in actively managed funds are essentially paying for the skill and judgment of the fund manager. The hope is that this expertise will lead to superior risk-adjusted returns compared to simply tracking the market.

- Flexibility: Active managers have the flexibility to adjust their portfolios in response to changing market conditions, economic shifts, or new information about individual companies. They can choose to overweight certain sectors, underweight others, or move into cash during periods of high volatility.

- Potential for Outperformance: While difficult to achieve consistently, a skilled active manager can outperform the market over specific periods.

- Higher Turnover: Active management typically involves more frequent buying and selling of securities, leading to higher portfolio turnover rates. This can result in increased transaction costs within the fund and, as we’ll discuss, significant tax implications for investors.

- Higher Fees: The extensive research, analysis, and trading required for active management translate into higher operating expenses and, consequently, higher expense ratios for investors.

While the allure of beating the market is strong, numerous studies have shown that a significant percentage of actively managed funds fail to consistently outperform their benchmark indexes after accounting for fees over the long term. This has led many investors to question the value proposition of active management, especially given its higher costs.

Passively Managed Funds (Index Funds)

In contrast, passively managed funds, often referred to as index funds, aim to replicate the performance of a specific market index rather than trying to beat it. These funds simply buy and hold the securities that make up their target index in the same proportions. They do not rely on a fund manager’s ability to pick winning stocks or time the market.

- Benchmark Tracking: The primary goal is to match the returns of the chosen index as closely as possible, minimizing “tracking error.”

- Lower Turnover: Since the fund only buys or sells securities when the underlying index rebalances, portfolio turnover is generally very low. This reduces internal transaction costs.

- Lower Fees: The lack of extensive research and active trading means significantly lower operating costs, translating into much lower expense ratios for investors.

- Market Returns: By definition, a passively managed fund will not significantly outperform its benchmark, but it also won’t significantly underperform it (before fees). It guarantees you receive the market’s return for that specific segment.

Most ETFs fall into the passively managed category, closely tracking various indexes. This is a major reason for their widespread appeal and low-cost structure. However, it’s important to note that the lines are blurring:

- There are actively managed ETFs that employ a fund manager to make investment decisions, similar to active mutual funds, but still trade on an exchange.

- Conversely, there are passively managed mutual funds (index mutual funds) that track an index and have very low expense ratios, similar to index ETFs.

Diversification Benefits

Both actively and passively managed funds (whether mutual funds or ETFs) inherently offer diversification benefits compared to investing in individual stocks. By holding a basket of securities, they reduce the impact of any single company’s poor performance on your overall portfolio. This is a crucial element for risk management and a cornerstone of any sound investment strategy, especially when considering long-term goals like How To Build Generational Wealth, where consistent growth and risk mitigation are paramount.

The choice between active and passive management often reflects an investor’s belief in market efficiency. Those who believe markets are generally efficient and difficult to beat after costs often favor passive strategies. Those who believe skilled managers can consistently identify undervalued assets or market opportunities may opt for active management, willing to pay the higher fees for that potential edge.

Tax Implications and Efficiency

The tax efficiency of an investment vehicle can have a substantial impact on your net returns, particularly for investments held in taxable accounts. While both mutual funds and ETFs generate taxable events, their operational structures lead to significant differences in how and when these taxes are incurred.

Mutual Funds and Taxable Distributions

Mutual funds, especially actively managed ones, are generally considered less tax-efficient than ETFs. This is primarily due to two factors:

- Capital Gains Distributions:

When an actively managed mutual fund sells securities within its portfolio for a profit, it realizes a capital gain. If these gains are not offset by losses, the fund is typically required to distribute them to its shareholders at least once a year. These are known as capital gains distributions. Crucially, investors are liable for taxes on these distributions in the year they are received, even if they reinvest the distribution or haven’t sold any of their own fund shares. This can create an unexpected tax bill, especially if a fund has high turnover or is forced to sell assets due to large investor redemptions.

For example, if a fund manager sells a highly appreciated stock they’ve held for years to rebalance the portfolio, any capital gains realized will be passed on to shareholders. This means you could receive a taxable distribution even in a year when the fund’s overall value declined, or if you only recently purchased the fund.

- High Portfolio Turnover:

Actively managed mutual funds often have high portfolio turnover rates, meaning they frequently buy and sell securities. This constant trading increases the likelihood of realizing capital gains, leading to more frequent and potentially larger capital gains distributions to shareholders.

- Dividend and Interest Distributions:

Like ETFs, mutual funds also distribute dividends (from stocks) and interest (from bonds) received from their underlying holdings. These distributions are also taxable in the year they are received, unless held in a tax-advantaged account.

The tax inefficiency of mutual funds is less of a concern for investments held within tax-advantaged accounts like 401(k)s, IRAs, or 529 plans, where taxes are deferred until withdrawal or entirely exempt. However, for investments in a standard brokerage account, the tax drag from capital gains distributions can significantly reduce your compounding returns over the long term.

ETFs and Tax Efficiency

ETFs are generally praised for their superior tax efficiency, primarily due to their unique “in-kind” creation and redemption mechanism:

- The “In-Kind” Redemption Mechanism:

When an authorized participant (AP) wants to redeem ETF shares, they don’t receive cash. Instead, they receive a basket of the underlying securities from the ETF portfolio. When the ETF needs to raise cash to meet redemptions, the fund manager typically gives the AP the lowest-cost-basis shares (i.e., shares that have appreciated the most) in exchange for the ETF units. By transferring these highly appreciated shares out of the fund without selling them, the ETF avoids realizing capital gains. This process effectively flushes out capital gains from the fund, leaving a portfolio with a higher average cost basis. This is a significant advantage over mutual funds, which typically have to sell securities to meet redemptions, thereby realizing taxable capital gains.

- Low Portfolio Turnover (for Index ETFs):

Since most ETFs are passively managed index funds, they have very low portfolio turnover. They only trade when the underlying index rebalances, which is typically infrequent. This minimal trading activity means fewer realized capital gains within the fund’s portfolio, further reducing the likelihood of capital gains distributions to shareholders.

- Dividend and Interest Distributions:

Similar to mutual funds, ETFs also distribute dividends and interest received from their underlying holdings, which are taxable in the year received in a taxable account.

The combined effect of the in-kind redemption mechanism and generally low turnover makes ETFs highly tax-efficient in taxable accounts. Investors holding ETFs are less likely to receive taxable capital gains distributions from the fund itself. Their primary taxable event will be when they choose to sell their own ETF shares for a profit.

Implications for Long-Term Investors

For investors planning to hold assets for many years, especially those focused on strategies like How To Build Generational Wealth, the tax efficiency of ETFs can be a powerful advantage. Over decades, minimizing annual tax liabilities means more of your investment capital remains invested and continues to compound. The difference in tax drag between a high-turnover mutual fund and a low-turnover ETF can translate into hundreds of thousands, if not millions, of dollars in additional wealth over a long investment horizon.

Therefore, when building a diversified portfolio, particularly in taxable accounts, the tax efficiency of ETFs often makes them a preferred choice for core holdings designed for long-term growth. This doesn’t mean mutual funds are always unsuitable; rather, it highlights the importance of considering the tax implications of each vehicle within your overall financial plan for 2026 and beyond.

Choosing the Right Vehicle for Your Financial Goals

Deciding between an ETF and a mutual fund is not

Recommended Resources

Check out Best Cashback Credit Cards 2026 on Gold Points for a deeper dive.

For more on ETF vs mutual, see How To Register An Llc For Online Business on E-ComProfits.