Understanding the Fundamentals: What is a Regular Savings Account?

A regular savings account, often referred to as a traditional savings account, is the most common and foundational type of savings vehicle offered by brick-and-mortar banks and credit unions. It’s typically the first account many people open after a checking account, serving as a safe and accessible place to store money that isn’t immediately needed for daily expenses.

Core Characteristics of Regular Savings Accounts

- Low Interest Rates: The defining feature of a regular savings account is its relatively low Annual Percentage Yield (APY). While you do earn interest on your deposits, the rates are often minimal, sometimes barely keeping pace with inflation, and occasionally even below 0.10% APY. This means your money grows very slowly, if at all, in real terms.

- Easy Accessibility: Traditional banks prioritize convenience. Regular savings accounts usually offer unparalleled access to your funds through various channels:

- Physical branches for in-person deposits and withdrawals.

- ATMs for cash access.

- Online banking platforms and mobile apps for transfers and balance inquiries.

- Linked to checking accounts for seamless transfers.

This high level of accessibility makes them ideal for funds that might need to be accessed quickly, though federal regulations (Regulation D) historically limited certain transfers and withdrawals to six per month, a rule that was temporarily suspended during the COVID-19 pandemic but remains a consideration for some institutions.

- Low or No Minimum Balance Requirements: Many regular savings accounts, especially those offered by large retail banks, come with very low or no minimum balance requirements to open or maintain the account. This makes them accessible to a broad spectrum of savers, including those just starting their financial journey.

- Fee Structures: While some accounts are entirely free, others may charge monthly maintenance fees if certain conditions aren’t met, such as maintaining a minimum balance, setting up direct deposit, or linking to a checking account. It’s crucial to review the fee schedule carefully.

- FDIC or NCUA Insurance: A critical safety net, regular savings accounts at FDIC-insured banks or NCUA-insured credit unions protect your deposits up to $250,000 per depositor, per institution, per ownership category. This federal insurance provides peace of mind, ensuring your money is safe even if the financial institution fails.

Common Uses for Regular Savings Accounts

Given their characteristics, regular savings accounts are well-suited for specific financial needs:

- Emergency Funds: While a high-yield option is often better, a regular savings account can serve as a basic emergency fund, especially if immediate, in-person access to cash might be a priority for some individuals.

- Short-Term Goals: Funds earmarked for very short-term goals, such as a vacation planned for next month or a small purchase within a few weeks, might be stored here due to instant access.

- Holding Place for Surplus Cash: For individuals who frequently transfer money between checking and savings, the seamless integration of traditional accounts can be appealing.

- Convenience for Children/Teens: Often the first banking product for younger individuals, helping them learn basic money management with easy parental oversight.

While safe and convenient, the primary drawback of a regular savings account is its inability to significantly grow your money over time, making it less effective for long-term savings strategies or combating inflation.

Unveiling the Potential: What is a High-Yield Savings Account (HYSA)?

A high-yield savings account (HYSA) fundamentally serves the same purpose as a regular savings account – a place to store liquid cash and earn interest. However, the “high-yield” differentiator is precisely what sets it apart, offering significantly more attractive interest rates than traditional options. HYSAs have gained immense popularity, particularly with the rise of online-only banks and fintech innovations.

Key Differentiators and Characteristics of HYSAs

- Significantly Higher Interest Rates (APY): This is the hallmark of an HYSA. They typically offer APYs that are anywhere from 10 to 20 times, or even more, higher than the national average for regular savings accounts. While rates fluctuate with the broader economic environment and the Federal Reserve’s policies, an HYSA consistently aims to provide a much better return on your idle cash. For instance, if a regular savings account offers 0.05% APY, an HYSA might offer 0.50% to 5.00% APY or even higher, depending on market conditions in 2026. This higher yield allows your money to grow more substantially through the power of compounding.

- Predominantly Online-Only or Digital First: The vast majority of HYSAs are offered by online-only banks, neo-banks, or the online divisions of traditional banks. This digital-first model allows these institutions to operate with lower overhead costs (no physical branches, fewer staff, etc.), which they then pass on to consumers in the form of higher interest rates.

- Limited Physical Branches: While some HYSAs are offered by traditional banks, their high-yield versions often function primarily online. This means in-person transactions are rare or non-existent.

- Robust Digital Tools: Online banks typically excel in digital user experience, offering intuitive websites, powerful mobile apps, and features like goal-setting tools, budgeting interfaces, and easy integration with other financial apps.

- Competitive Fee Structures: Many HYSAs boast minimal to no monthly maintenance fees, especially if you opt for purely online banking. Minimum balance requirements to open an account can vary, with some requiring a modest initial deposit and others having no minimum at all. However, some might require a certain balance to earn the advertised top-tier APY.

- FDIC or NCUA Insurance: Crucially, just like regular savings accounts, legitimate HYSAs are FDIC-insured (for banks) or NCUA-insured (for credit unions) up to the standard $250,000 per depositor, per institution, per ownership category. This means your money is just as safe as it would be in a traditional account, dispelling any myths that higher yields equate to higher risk for your principal.

- Ease of Fund Transfers: While direct cash deposits might require an extra step (depositing into a linked checking account first), transferring funds to and from an HYSA is typically straightforward. You can link your HYSA to your external checking accounts via ACH transfers, which usually take 1-3 business days.

Optimal Uses for High-Yield Savings Accounts

Given their superior interest-earning potential and liquidity, HYSAs are ideally suited for:

- Emergency Funds: This is arguably the most common and recommended use for an HYSA. Your emergency fund should be easily accessible but also working for you. An HYSA allows your emergency cash to grow, helping to offset inflation and potentially increase your safety net.

- Medium-Term Savings Goals: Whether you’re saving for a down payment on a house, a new car, a significant vacation, or a child’s education fund that you don’t want exposed to market volatility yet, an HYSA is an excellent choice. It provides growth without the risk associated with investments.

- Large Purchases: Accumulating funds for a significant expense, like a home renovation, can be accelerated with the higher interest an HYSA provides.

- Capital for Future Investments: If you’re accumulating a lump sum for a future investment (e.g., waiting for a market dip, or reaching a minimum threshold for a specific investment vehicle), an HYSA can hold that cash and earn a decent return in the interim.

An HYSA represents a smart financial move for anyone looking to make their idle cash work harder without sacrificing safety or liquidity. It bridges the gap between low-return traditional savings and higher-risk investments, providing an optimal solution for short-to-medium term financial objectives.

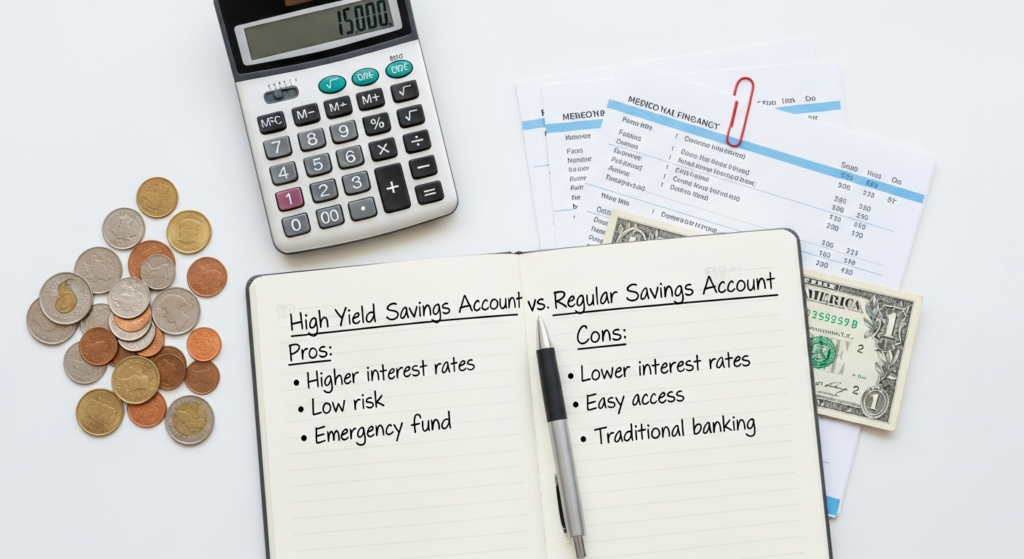

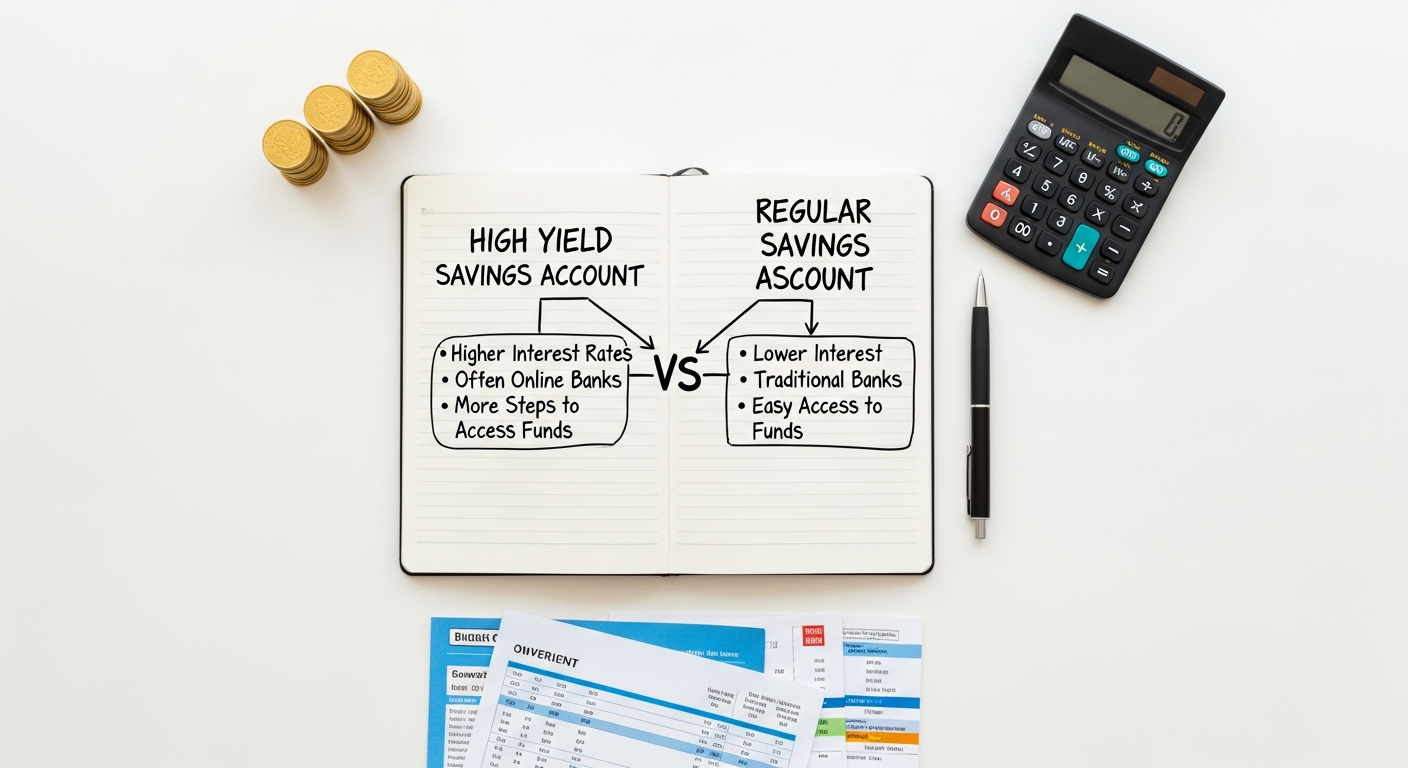

The Core Comparison: High-Yield vs. Regular Savings – Key Differences

1. Interest Rates (APY) – The Primary Differentiator

- Regular Savings Account: Typically offers very low Annual Percentage Yields (APYs), often ranging from 0.01% to 0.10%. In some periods, these rates might be so low they barely register, meaning your money grows at a negligible pace, if at all, when considering inflation.

- High-Yield Savings Account (HYSA): Provides significantly higher APYs, often 10 to 50 times (or more) greater than regular savings accounts. Depending on the economic climate and the Federal Reserve’s benchmark rates, HYSAs can offer APYs from 0.50% to over 5.00%. This difference is the most compelling reason to choose an HYSA, as it allows your money to combat inflation more effectively and compound growth over time.

2. Accessibility and Convenience

- Regular Savings Account: Excels in immediate, multi-channel accessibility. Users benefit from:

- Extensive networks of physical branches for in-person deposits, withdrawals, and customer service.

- Widespread ATM access.

- Seamless integration with other accounts at the same institution (e.g., instant transfers to checking).

- Convenience for cash transactions.

- High-Yield Savings Account (HYSA): Primarily operates online. While highly convenient for digital banking, it typically lacks:

- Physical branch access.

- Direct ATM access (though many provide debit cards for linked checking or offer ATM fee reimbursements for withdrawals from other networks).

- Cash deposits usually require an intermediate step (deposit into a linked traditional checking account, then transfer to HYSA).

Transfers to external accounts usually occur via ACH, taking 1-3 business days. This slight delay in immediate cash access is a trade-off for higher returns.

3. Fees and Minimum Balances

- Regular Savings Account: May have monthly maintenance fees that can be waived by meeting certain conditions (e.g., minimum balance, direct deposit). Minimum balance requirements to open can be very low, sometimes just a few dollars.

- High-Yield Savings Account (HYSA): Often boasts fewer fees, with many online banks offering no monthly maintenance fees at all. Minimum balance requirements to open an account can vary widely; some require no minimum, while others might ask for an initial deposit of $100 or more. Some HYSAs might have a minimum balance to earn the highest advertised APY.

4. Digital Tools and User Experience

- Regular Savings Account: Online banking platforms and mobile apps have improved significantly across traditional banks, but their core focus remains broader financial services.

- High-Yield Savings Account (HYSA): Online banks often lead the way in user-friendly digital interfaces, intuitive mobile apps, and advanced features like goal-setting tools, automatic savings transfers, and robust budgeting integrations. Their entire operation is built around a digital-first customer experience.

5. FDIC/NCUA Insurance

- Both: This is a crucial point of commonality. As long as you choose an HYSA from an FDIC-insured bank or an NCUA-insured credit union (which virtually all reputable ones are), your deposits are protected up to $250,000 per depositor, per institution, per ownership category. The higher yield of an HYSA does NOT imply higher risk to your principal; it merely reflects the bank’s operational cost structure and competitive strategy.

6. Liquidity

- Both: Both account types are highly liquid, meaning you can access your funds relatively easily without penalties for withdrawal (unlike CDs or some investment accounts). The difference lies more in the speed and method of access, as discussed under convenience.

In essence, the choice boils down to your priorities: if immediate, in-person cash access and a full suite of traditional banking services are paramount, a regular savings account might suffice. However, if your primary goal is to make your money work harder through higher interest rates, and you’re comfortable with predominantly online banking, an HYSA is the clear winner.

When to Choose Which: Tailoring Your Savings Strategy

The decision between a high-yield and a regular savings account isn’t about one being inherently “better” than the other in all circumstances. It’s about aligning the account type with your specific financial needs, habits, and goals. A well-rounded personal finance strategy might even incorporate both.

When a Regular Savings Account Might Be the Right Choice

Despite the allure of higher yields, a regular savings account still holds relevance for certain scenarios:

- Immediate Cash Access is Critical: If you frequently need to deposit or withdraw physical cash, or require instant, in-person access to your funds, a traditional bank with branches and ATMs may be more convenient. This could be relevant for small business owners who handle cash daily or individuals who prefer tangible banking interactions.

- Comfort with Traditional Banking: Some individuals simply prefer the familiarity and established presence of a brick-and-mortar bank. They might value having a specific banker, consistent customer service, or the ability to handle all their financial needs (checking, savings, loans, investments) under one roof.

- Very Small Balances: If you’re just starting to save and only have a few dollars to put aside, the difference in interest earned between a regular and high-yield account might be negligible. In this case, convenience and ease of use might outweigh the marginal interest gain.

- Linked Services and Convenience: If your checking account, loans, and other financial products are all with one traditional bank, keeping a regular savings account there can simplify transfers and account management within the same ecosystem.

When a High-Yield Savings Account (HYSA) Shines

For most individuals focused on growing their savings, the HYSA is the superior option, especially for key financial objectives:

- Building an Emergency Fund: This is arguably the most crucial application for an HYSA. Your emergency fund needs to be liquid (easily accessible) and safe (FDIC-insured), but it should also work for you. An HYSA allows your 3-6 months (or more) of living expenses to earn a meaningful return, helping it grow and maintain its purchasing power against inflation. This is a foundational step for anyone implementing a strategy for How To Build Generational Wealth, as a robust emergency fund prevents unexpected expenses from derailing long-term plans.

- Saving for Medium-Term Goals (1-5 Years): If you’re saving for a down payment on a house, a new car, a significant vacation, home renovations, or a child’s education fund that’s still a few years away, an HYSA is ideal. It provides growth without the market volatility risks associated with investments, ensuring your principal is safe and growing steadily.

- Maximizing Passive Income: For those with substantial cash reserves that aren’t immediately invested, an HYSA provides an excellent way to earn passive income. Even small interest gains add up over time, contributing to your overall financial well-being.

- Budgeting and Financial Planning: Incorporating an HYSA into your financial plan is a smart move. As part of How To Create A Monthly Budget, you should identify surplus funds after covering expenses. Instead of letting these funds sit idly in a low-interest checking or regular savings account, transferring them to an HYSA allows them to contribute meaningfully to your financial growth. Automated transfers from your checking to your HYSA after each paycheck are a powerful strategy.

- Comfort with Digital Banking: If you’re comfortable managing your finances primarily online or through mobile apps, the digital-first nature of HYSAs will be a natural fit.

A Hybrid Approach for Optimal Results

Many financially savvy individuals adopt a hybrid strategy:

- Maintain a regular checking account (and perhaps a linked regular savings account for immediate, minor transfers) at a traditional bank for daily transactions, bill payments, and easy cash access.

- Keep the bulk of their emergency fund and medium-term savings in a separate high-yield savings account at an online institution, maximizing interest earnings.

This approach combines the best of both worlds: the convenience of traditional banking for day-to-day needs and the superior growth potential of an HYSA for strategic savings.

Maximizing Your Savings: Strategies Beyond the Account Type

Choosing between a high-yield and a regular savings account is a critical first step, but it’s just one piece of the puzzle. To truly maximize your savings and accelerate your financial goals, you need to implement disciplined strategies that go beyond merely selecting the right account. These strategies are integral to building a robust financial foundation and are key components in broader objectives like How To Build Generational Wealth.

1. Automate Your Savings

The simplest yet most powerful strategy is to “pay yourself first.” Set up automatic transfers from your checking account to your high-yield savings account immediately after you get paid.

- Consistency is Key: Automation removes the temptation to spend the money and ensures consistent contributions. Even small, regular contributions compound significantly over time.

- Budget Integration: When you How To Create A Monthly Budget, designate a specific amount for savings as a non-negotiable “expense.” This makes savings a priority, not an afterthought.

- Multiple Savings Goals: Many HYSAs allow you to create sub-accounts or “buckets” within your main account. You can automate transfers to specific goals like “Emergency Fund,” “Down Payment,” or “Vacation Fund,” helping you visualize progress.

2. Regularly Review and Adjust Your Savings Rate

Don’t just set it and forget it. Periodically (e.g., quarterly or annually) review your income, expenses, and savings contributions.

- Increase Contributions with Income: As your income grows (raises, bonuses, side hustles), increase your automated savings contributions proportionally. Don’t fall victim to lifestyle creep.

- Reallocate Found Money: Direct windfalls like tax refunds, work bonuses, or unexpected gifts directly into your HYSA.

- Leverage Expense Reduction: Actively look for ways to cut down on unnecessary spending. Techniques like How To Negotiate Bills And Lower Expenses (e.g., calling your internet provider, reviewing insurance policies, canceling unused subscriptions) can free up significant amounts of money that can then be redirected to your savings.

3. Understand and Harness Compounding Interest

The magic of an HYSA truly shines with compounding interest. This is interest earned not only on your initial deposit but also on the accumulated interest from previous periods.

- Time is Your Ally: The longer your money sits in an HYSA, the more powerful compounding becomes. Even seemingly small differences in APY can lead to substantial differences over years.

- Frequency Matters: While most HYSAs compound interest monthly or daily, the APY already accounts for this, so focus on comparing the APY directly.

4. Shop Around for the Best Rates (Periodically)

The high-yield savings market is competitive, and rates can fluctuate.

- Stay Informed: Keep an eye on the leading HYSA rates. What was the best rate a year ago might not be today.

- Don’t Be Afraid to Switch: Transferring funds between HYSAs is relatively easy. If another institution offers a significantly better, consistent rate with comparable features and FDIC insurance, consider moving your money. The small effort can lead to hundreds or thousands of dollars in extra interest over time.

5. Differentiate Savings Goals

Not all savings are created equal. Use your HYSA to segment your goals.

- Emergency Fund: Keep this sacrosanct and separate from other goals.

- Short-to-Medium Term Goals: Use separate “buckets” or even different HYSAs for goals like a down payment, a new car, or a child’s college fund if it’s within a 5-year horizon.

By implementing these strategies, your savings won’t just sit there; they will actively contribute to your financial growth, providing a solid foundation for achieving both immediate objectives and long-term aspirations, including the ambitious goal of How To Build Generational Wealth.

The Future of Savings: Trends and Considerations for 2026

The financial landscape is in a constant state of flux, driven by technological innovation, economic shifts, and evolving consumer preferences. As we look towards 2026, several trends and considerations will continue to shape the world of savings accounts, particularly high-yield options.

1. Continued Dominance of Digital-First Banking

- Enhanced User Experience: Online banks and fintech platforms will likely continue to invest heavily in their digital interfaces, offering more intuitive apps, personalized financial insights, and seamless integration with other financial tools (e.g., budgeting apps, investment platforms).

- AI and Personalization: Expect more AI-driven features, such as automated savings recommendations based on spending habits, predictive analytics for financial goal achievement, and personalized nudges to optimize savings behavior.

- Embedded Finance: Savings features might become more deeply embedded within non-traditional platforms, meaning you could potentially save directly from apps you use for shopping, ride-sharing, or other services, blurring the lines between different financial activities.

2. Dynamic Interest Rate Environment

- Federal Reserve Influence: High-yield savings rates are closely tied to the Federal Reserve’s federal funds rate. Economic conditions, inflation targets, and geopolitical factors will continue to influence central bank decisions, leading to potential fluctuations in HYSA APYs. Savers in 2026 will need to remain vigilant and proactive in monitoring rates.

- Competitive Market: The competition among online banks and fintechs for deposits will likely remain fierce. This competition is generally beneficial for consumers, as it pushes institutions to offer attractive rates and features to stand out.

3. Evolution of Savings Products

- Hybrid Accounts: We may see more hybrid accounts that blend features of checking and savings, offering higher yields on checking balances or seamless integration of spending and saving within a single account, simplifying financial management.

- Gamified Savings: To encourage better savings habits, more platforms might incorporate gamification elements, challenges, and rewards to make saving more engaging and motivate users to reach their financial goals.

- Focus on Financial Wellness: Beyond just offering interest, banks will increasingly provide tools and resources focused on overall financial wellness, including access to financial advisors, educational content (like Fin3go’s guides on How To Create A Monthly Budget or How To Negotiate Bills And Lower Expenses), and pathways to more complex wealth-building strategies.

4. Enhanced Security Measures

- Cybersecurity Advancements: As banking becomes more digital, the focus on robust cybersecurity will intensify. Expect advanced encryption, multi-factor authentication, and AI-powered fraud detection to become even more sophisticated, ensuring the safety of your deposits and personal information.

- Regulatory Oversight: Regulators will continue to adapt to the rapidly changing fintech landscape, ensuring consumer protection and financial stability across all digital banking products, including HYSAs.

5. Integration with Broader Financial Goals

- Seamless Investment Pathways: HYSAs will increasingly serve as a natural bridge to investment accounts. Platforms may offer easier transitions from saving for a down payment to then investing in real estate, or moving accumulated cash into brokerage accounts for long-term growth as part of a strategy for How To Build Generational Wealth.

- Holistic Financial Planning: The trend is towards integrated platforms that provide a holistic view of your financial life, combining savings, investments, debt management, and budgeting into one cohesive experience.

For savers in 2026, the key will be to stay informed, remain flexible, and actively engage with the best tools and products available. The landscape will offer unprecedented opportunities to make your money work harder, but it will also require a proactive approach to managing your finances effectively.

Frequently Asked Questions About Savings Accounts

What is the primary difference between a high-yield savings account and a regular savings account?

The primary difference lies in the interest rate (APY) offered. High-yield savings accounts (HYSAs) typically offer significantly higher interest rates than regular savings accounts, often 10 to 50 times more. This means your money grows much faster in an HYSA. Regular savings accounts are usually offered by traditional banks with physical branches and very low rates, while HYSAs are predominantly offered by online-only banks with higher rates due to lower overheads.

Is my money safe in a high-yield savings account?

Yes, absolutely. Reputable high-yield savings accounts are FDIC-insured (if it’s a bank) or NCUA-insured (if it’s a credit union) up to the standard limit of $250,000 per depositor, per institution, per ownership category. This means your principal is just as safe as it would be in a traditional savings account, even if the bank were to fail. Always verify the FDIC or NCUA insurance status before opening an account.

Are there any downsides to a high-yield savings account?

While the benefits generally outweigh the drawbacks for most savers, potential downsides of HYSAs can include: limited or no physical branch access, which might be inconvenient for frequent cash transactions; slightly slower access to funds via ACH transfers (typically 1-3 business days); and the requirement for a separate checking account for immediate cash needs. Some HYSAs might also have minimum balance requirements to earn the highest APY, though many do not.

How often do high-yield savings account interest rates change?

High-yield savings account interest rates are variable and can change frequently. They are largely influenced by the Federal Reserve’s federal funds rate and the broader economic environment. When the Fed raises or lowers its benchmark rate, HYSAs typically adjust their APYs in response, though not always immediately or by the same margin. It’s wise to monitor rates periodically, perhaps every six months or so in 2026, to ensure you’re still getting a competitive return.

Can I link my high-yield savings account to my regular checking account?

Yes, you can almost always link your high-yield savings account to your external checking account, even if they are at different financial institutions. This is typically done through ACH (Automated Clearing House) transfers, which allow you to move money between accounts. You’ll usually need to provide your checking account’s routing and account numbers to set up the link, which often involves small test deposits for verification.

Do I pay taxes on the interest earned from a high-yield savings account?

Yes, the interest you earn from both high-yield and regular savings accounts is considered taxable income by the IRS. The financial institution will typically send you a Form 1099-INT if you earn $10 or more in interest during the year. You will need to report this income on your federal (and often state) tax return. While not a “downside” unique to HYSAs, it’s an important factor to consider when calculating your net returns.

Recommended Resources

For more on high yield savings, see How To Build Email List For Online Store on E-ComProfits.

Check out How To Open A Brokerage Account Guide on Trading Costs for a deeper dive.