The Comprehensive History of Fintech: From Ancient Times to Digital Dominance

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

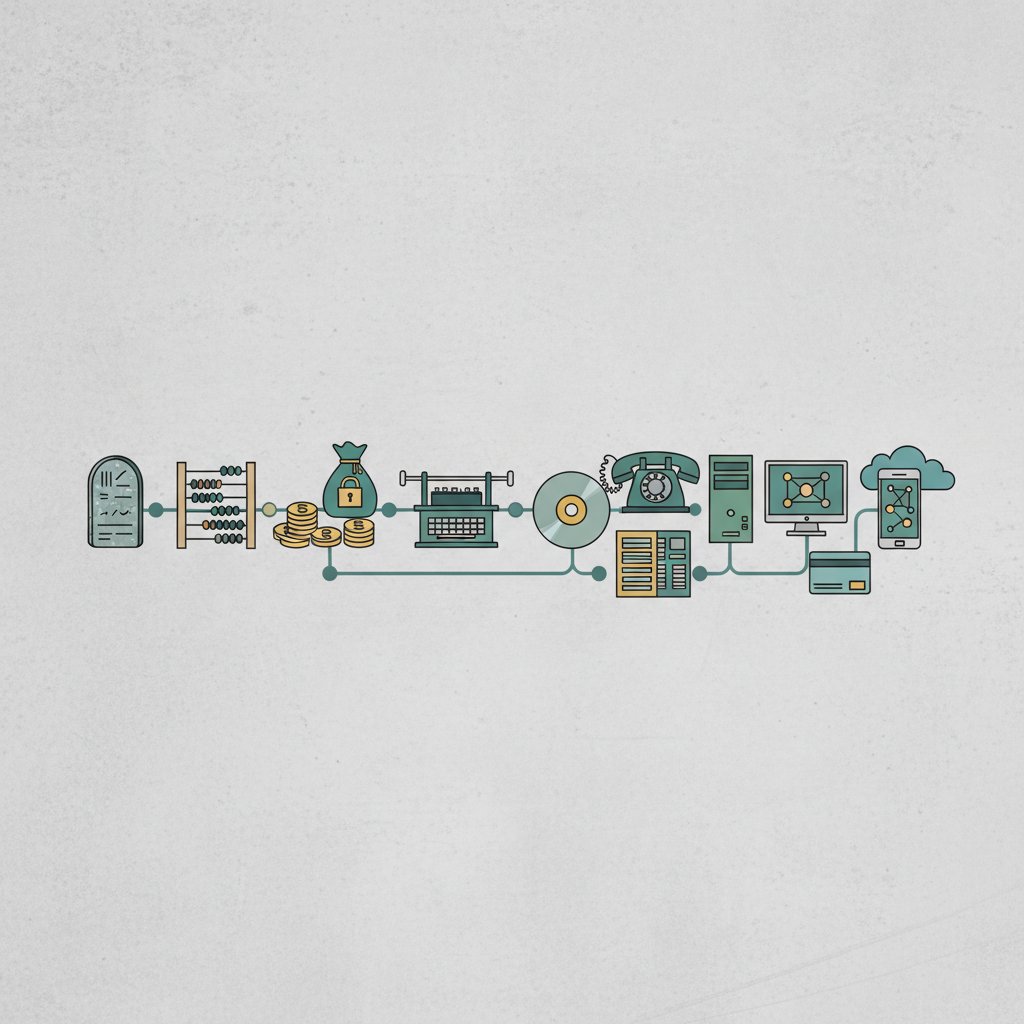

Understanding the Evolution of Financial Technology

The term “fintech” might sound like a modern buzzword, conjuring images of sleek financial apps and virtual currencies. However, the conceptual history of fintech stretches back much further than most realize. At its core, fintech is simply the application of technology to improve financial services. This broad definition allows us to trace its roots from the very beginnings of organized commerce and banking to the hyper-connected, real-time financial world we inhabit today.

From the first systems for currency exchange and credit to the development of sophisticated algorithms for algorithmic trading and artificial intelligence-driven financial advice, technology has consistently shaped and reshaped how we manage our money. This journey is not linear; it’s a tapestry woven with threads of innovation, societal changes, economic upheavals, and regulatory responses. Each era brought its own set of challenges and, crucially, technological solutions that pushed the boundaries of what was possible in finance.

At fin3go, we believe that understanding this historical context is crucial for anyone engaging with personal finance today. It provides perspective on why certain financial products exist, how they evolved, and what forces are currently driving the next wave of disruption. It helps us appreciate the intricate dance between human ingenuity and technological advancement that has defined our financial lives for centuries. This comprehensive look at the history of fintech will explore key milestones, pivotal inventions, and the overarching trends that have led us to the current landscape of digital banking, mobile payments, and sophisticated investment platforms.

Early Forms of Financial Innovation and Technology

While the term “fintech” is relatively new, the underlying concept of using advanced tools to manage money is ancient. Early civilizations, driven by the need for trade, record-keeping, and wealth management, developed rudimentary yet effective financial technologies. These early innovations laid the groundwork for complex financial systems thousands of years later.

Ancient Accounting and Currency Systems

The earliest forms of financial technology can be traced back to the dawn of civilization. In Mesopotamia, around 3500-3000 BCE, Sumerians developed cuneiform writing on clay tablets not just for literature, but extensively for keeping detailed records of agricultural transactions, loans, and taxes. This was a critical technological leap for managing economic activity and establishing rudimentary forms of credit.

- Clay Tablets and Cuneiform: Used for tracking debts, payments, and trade. Essential for the function of early economies and the tracking of communal resources.

- Barter Systems and Early Currencies: While not strictly “technology,” the standardization of certain commodities (like salt, shells, or metals) as a medium of exchange was a technological innovation in facilitating trade beyond direct barter.

- Weights and Measures: Standardized systems for weight and measurement were crucial for fair trade and the accurate valuation of goods, a fundamental precursor to standardized currency.

The Lydians, a kingdom in ancient Anatolia, are credited with inventing the first standardized coinage around the 7th century BCE. These electrum coins, stamped with official insignia, were a groundbreaking technological advancement. They offered a portable, durable, and verifiable medium of exchange, revolutionizing trade and wealth storage far beyond the limitations of bulk commodities.

The Birth of Banking and Commercial Instruments

During the medieval and Renaissance periods, especially in Italian city-states like Florence and Venice, banking began to take a more recognizable shape. Merchants and moneylenders developed sophisticated systems for managing large sums of money, facilitating international trade, and extending credit.

- Bills of Exchange: These instruments, essentially early forms of checks or promissory notes, allowed merchants to transfer funds across long distances without physically moving large quantities of gold or silver, mitigating risks of theft and simplifying cross-border transactions. This was an ingenious solution to a significant logistical and security challenge.

- Double-Entry Bookkeeping: Developed in Italy in the 14th century, this accounting method provided a comprehensive and error-checking system for tracking financial transactions. Luca Pacioli’s 1494 treatise codified these practices, which remain the foundation of modern accounting. This systematization dramatically increased transparency and accuracy in financial dealings.

- Goldsmiths as Early Banks: In England, goldsmiths, with their secure vaults, began offering storage for valuables and later issued promissory notes (early banknotes) against deposits. These notes circulated as currency, and the goldsmiths evolved into the first true banks, offering loans and managing accounts.

These developments, while mechanical rather than electronic, represent critical early iterations of financial technology, solving problems of security, efficiency, and scalability that continue to drive fintech innovation today. The need for faster, safer, and more reliable financial transactions has consistently been a catalyst for technological advancement in finance.

[INLINE IMAGE 1: place after second H2 | alt=”history of fintech concept illustration”]

The Industrial Age: Mechanization and Communication

The Industrial Revolution, beginning in the late 18th century, brought about profound changes in manufacturing, transportation, and communication. These advancements, while not directly financial, had a transformative impact on how financial services were conducted, making them faster, more integrated, and accessible to a wider populace. The mechanization of processes and the birth of rapid communication laid the groundwork for modern banking infrastructure.

Telegraphy and the Global Financial Markets

The invention and widespread adoption of the telegraph in the mid-19th century represented a seismic shift in financial communication. Before the telegraph, news of financial markets, stock prices, and economic events traveled at the speed of a ship or a horse. This meant significant delays and regional price discrepancies.

- Instantaneous Information Transfer: The telegraph allowed for near-instantaneous transmission of information across continents. Financial institutions could receive real-time stock quotes, commodity prices, and news from distant markets.

- Arbitrage Opportunities and Market Efficiency: This rapid information flow enabled arbitrage, where investors could profit from price differences in different markets. More importantly, it led to greater overall market efficiency, as information quickly disseminated and prices converged.

- Consolidation of Markets: The telegraph facilitated the integration of geographically disparate financial markets, paving the way for truly global financial systems. A crisis in London could almost immediately affect markets in New York.

The transatlantic telegraph cable, completed in 1866, was a monumental achievement that dramatically shrunk the world for finance, enabling business transactions and market updates between Europe and North America to occur within minutes rather than weeks. This was an early, powerful example of how communication technology drives financial interconnectedness.

Early Computing and Mechanical Accounting

As businesses grew in scale and complexity during the late 19th and early 20th centuries, manual accounting became increasingly cumbersome and prone to error. This spurred the development of mechanical and electro-mechanical devices designed to automate financial calculations and record-keeping.

- Adding Machines and Calculators: Mechanical adding machines became standard in banks and businesses for performing arithmetic operations quickly and accurately. These were indispensable for daily banking operations, such as tallying deposits and withdrawals.

- Punch Card Systems: Herman Hollerith’s tabulating machine, developed for the 1890 U.S. Census, utilized punch cards to process large datasets. This technology, later commercialized by IBM, revolutionized data processing for large organizations, including government agencies and insurance companies, making the handling of vast numbers of financial records feasible.

- Typewriters and Duplicators: While not strictly computational, the proliferation of typewriters and early duplicating machines significantly improved the efficiency of producing financial documents, contracts, and correspondence, speeding up administrative processes within financial institutions.

These early “fintech” tools, while crude by today’s standards, represented significant advancements in efficiency, accuracy, and scalability for managing financial information. They demonstrated a clear trend: as financial operations become more complex, the demand for technological solutions to manage that complexity inevitably follows. This era laid the groundwork for the digital revolution by proving the value of automating and systematizing financial processes.

The Dawn of Digital: Mainframes and Early Automation

The mid-20th century witnessed the birth of true electronic computing, ushering in an era of unprecedented automation potential for the financial industry. Mainframe computers, though massive and expensive, began to transform banking operations, moving beyond mechanical assistance to digital processing. This period marked the tangible beginnings of modern fintech.

Mainframe Computers in Banking

Starting in the 1950s and accelerating through the 1960s, mainframe computers began to be adopted by large banks and financial institutions. These powerful machines provided the capability to store, process, and manage vast quantities of financial data, something previously unimaginable. The transition from manual ledger books and punch cards to magnetic tapes and digital databases was revolutionary.

- Automated Transaction Processing: Mainframes enabled banks to automate the clearing and settlement of checks, manage customer accounts, and process loan applications with much greater speed and accuracy. This significantly reduced manual errors and processing times.

- Early Credit Card Systems: The rise of credit cards in the 1950s and 60s (e.g., Diners Club, BankAmericard, MasterCard) was heavily reliant on mainframe technology for transaction authorization, billing, and account management. Without mainframes, the scale and complexity of managing millions of credit accounts would have been impractical.

- Data Management and Reporting: Banks could now generate complex financial reports, analyze customer behavior, and manage their vast portfolios more effectively, leading to better risk management and strategic planning.

The development of industry standards like SWIFT (Society for Worldwide Interbank Financial Telecommunication) in 1973 further cemented the role of digital networks. SWIFT provided a standardized, secure messaging system for financial transactions between banks globally, creating a foundation for international payments and interbank connectivity that still operates today. This was a critical step in creating a global, interconnected financial infrastructure based on digital communication.

ATMs and Self-Service Banking

One of the most visible and impactful innovations of this digital dawn was the Automated Teller Machine (ATM). The first functional ATM was introduced in London in June 1967 by Barclays. It was a revolutionary concept: self-service banking that allowed customers to access their funds outside of traditional bank hours and without needing a human teller.

- Around-the-Clock Access: ATMs provided unprecedented convenience, liberating customers from the constraints of banking hours. This significantly improved customer experience and accessibility to funds.

- Reduced Branch Overhead: For banks, ATMs offered a way to reduce operational costs associated with manned teller stations and allowed for greater scalability without proportional increases in staffing.

- Network Expansion: The subsequent development of ATM networks (like Plus and Cirrus) allowed customers to withdraw cash from almost any bank, anywhere, further enhancing convenience and solidifying the concept of interconnected digital finance.

The ATM was a pioneer in self-service digital finance, foreshadowing the mobile banking apps and online platforms that would follow decades later. It taught consumers to trust machines with their money and paved the way for broader adoption of digital financial services, fundamentally changing the daily interaction people had with their banks. It was an early demonstration of how technology could empower individuals to manage their finances more independently.

[INLINE IMAGE 2: place after fourth H2 | alt=”history of fintech comparison illustration”]

The Internet Age: Online Banking and E-Commerce

The commercialization and widespread adoption of the internet in the 1990s marked another transformative era for fintech. The ability to connect millions of computers globally opened up entirely new avenues for financial services, moving from internal bank automation to direct-to-consumer digital offerings. This period saw the rise of online banking, e-commerce payment systems, and the initial foray into digital investment platforms.

The Rise of Online Banking

Initially hesitant due to security concerns, financial institutions gradually embraced the internet as a new channel for delivering services. Early online banking platforms, emerging in the mid-1990s, offered basic functionalities that were a revelation for customers accustomed to branch visits or phone calls.

- Remote Access: Customers could check account balances, view transaction history, and transfer funds between their accounts from the comfort of their homes or offices, at any time. This dramatically increased convenience and control over personal finances.

- Cost Efficiency for Banks: Online banking reduced the need for expensive physical branches and significantly lowered the operational costs associated with traditional customer service, as many routine inquiries could be handled digitally.

- Enhanced Financial Management: With transactional data readily available online, individuals gained better tools for budgeting and tracking their spending habits, albeit through static web interfaces initially.

Early pioneers like Stanford Federal Credit Union and Presidential Bank were among the first to offer internet banking in 1994 and 1995, respectively. Their success, combined with the growing dot-com enthusiasm, spurred broader adoption across the banking sector. The security protocols, while rudimentary by today’s standards, continually evolved to build user trust and enable wider acceptance.

E-commerce and Digital Payments

The internet made e-commerce possible, but for e-commerce to flourish, secure and efficient digital payment systems were essential. This need spurred the development of specialized fintech companies focused entirely on facilitating online transactions.

- PayPal and Online Payment Gateways: Companies like PayPal, founded in 1998, revolutionized peer-to-peer and merchant payments online. They provided a trusted intermediary between buyers and sellers, simplifying transactions and adding a layer of security. Payment gateways integrated with e-commerce websites became standard, allowing consumers to make purchases with credit cards or digital wallets without needing to re-enter details repeatedly.

- Increased Consumer Confidence: The development of secure socket layer (SSL) encryption and other security measures helped foster consumer confidence in online transactions, which was crucial for the growth of both e-commerce and digital finance.

- Early Digital Wallets: While not as sophisticated as today’s mobile wallets, early digital payment systems laid the groundwork for storing payment information and streamlining checkout processes, accelerating the adoption of online shopping.

This period also saw the emergence of online brokerages like E*TRADE and Charles Schwab, which democratized access to stock trading. Rather than relying on traditional brokers, individual investors could research and execute trades directly from their personal computers, often at significantly lower costs. This was a critical step in making investment services more accessible and empowering for the average person, further blurring the lines between traditional financial institutions and technology providers.

The Mobile Revolution and the Rise of “True” Fintech

The proliferation of smartphones and high-speed mobile internet connectivity starting in the late 2000s ushered in what many consider the true “fintech” era. This period is characterized by financial services being delivered directly to consumers’ pockets, enabling unprecedented access, convenience, and personalization. The mobile revolution redefined expectations for financial interactions and spurred a wave of disruptive innovation.

Smartphone Adoption and Mobile Banking

The launch of the iPhone in 2007, followed by Android devices, rapidly transformed the global technology landscape. With powerful computing capabilities and internet access in hand, consumers quickly embraced mobile applications for every aspect of their lives, including finance.

- Banking in Your Pocket: Mobile banking apps became standard offerings from traditional banks, allowing users to perform almost all functions previously reserved for online banking or ATMs: checking balances, transferring funds, paying bills, and even depositing checks via image capture (mobile check deposit).

- Enhanced User Experience: Mobile apps offered intuitive interfaces, biometric authentication (fingerprint, facial recognition), and personalized notifications, making financial management more engaging and secure.

- Location-Based Services: GPS capabilities enabled banks to offer features like ATM locators and personalized offers based on a user’s location, adding another layer of convenience.

The ease and immediacy of mobile banking quickly made it the preferred method of interaction for millions, significantly reducing branch visits and paving the way for truly branchless banking models. This shift empowered users with continuous access to their financial information and control.

Emergence of Fintech Startups and Niche Solutions

The mobile revolution, combined with the availability of cloud computing and open APIs, dramatically lowered the barrier to entry for new financial service providers. A new breed of “fintech” startups emerged, often focused on specific, underserved market segments or pain points that traditional banks had overlooked.

- Digital-Only Banks (Neobanks): Companies like Chime, N26, and Revolut emerged as entirely digital banking alternatives, offering streamlined accounts, fee-free services, and advanced mobile features without any physical branches. They leveraged technology to provide a superior, cost-effective customer experience.

- Peer-to-Peer (P2P) Payments: Apps like Venmo, Square Cash App, and Zelle made sending money between individuals as easy as sending a text message, eroding the dominance of traditional money transfer services.

- Personal Finance Management (PFM) Apps: Services like Mint and YNAB provided sophisticated tools for budgeting, expense tracking, and goal setting by aggregating data from multiple financial accounts, giving users a holistic view of their financial health.

- Specialized Lending Platforms: Online lenders (e.g., SoFi for student loan refinancing, LendingClub for P2P loans) leveraged data analytics and proprietary algorithms to offer faster, more personalized loan products outside traditional banking channels.

- Robo-Advisors: Services such as Betterment and Wealthfront automated investment management by using algorithms to build and manage diversified portfolios based on a user’s risk tolerance and financial goals, making sophisticated investment advice accessible to a broader audience at a lower cost.

This period cemented “fintech” as a distinct industry segment, characterized by agility, customer-centric design, and the clever application of technology to traditional financial challenges. The competition from these nimble startups forced traditional financial institutions to innovate more rapidly and adopt similar technologies, blurring the lines further between legacy players and new challengers. The mobile phone transformed from a communication device into a personal financial hub, marking an irreversible shift in how people interact with their money.

Key Technologies Driving Modern Fintech Disruption

The ongoing evolution of fintech is fueled by the relentless advance of several core technologies. These innovations are not just making existing financial services more efficient but are enabling entirely new paradigms of financial interaction, reshaping markets, and creating unprecedented opportunities. Understanding these technological pillars is crucial for comprehending the current and future landscape of finance.

Artificial Intelligence and Machine Learning

AI and ML are perhaps the most transformative technologies impacting fintech today. They enable machines to learn from data, identify patterns, make predictions, and automate complex decision-making processes that were once the exclusive domain of human expertise.

- Fraud Detection and Risk Assessment: ML algorithms can analyze vast datasets of transactions in real-time, identifying anomalous patterns indicative of fraud with much greater accuracy and speed than traditional rule-based systems. They also power sophisticated credit scoring models that can assess risk more dynamically and inclusively, potentially expanding access to credit.

- Personalized Financial Advice (Robo-Advisors): AI powers robo-advisors that offer automated, data-driven investment advice and portfolio management. These systems can tailor recommendations based on individual financial goals, risk tolerance, and market conditions, making sophisticated wealth management accessible and affordable.

- Chatbots and Customer Service: AI-powered chatbots and virtual assistants are increasingly handling routine customer inquiries, account management, and providing instant support, improving efficiency and customer satisfaction. Advanced AI can even handle complex queries, enhancing the overall customer experience.

- Algorithmic Trading: In capital markets, AI and ML are used to analyze market data, predict trends, and execute trades at high speeds, optimizing investment strategies and managing vast portfolios.

The ability of AI/ML to process and derive insights from massive amounts of data is fundamentally changing how financial institutions operate, from backend risk management to front-end customer engagement.

Blockchain and Distributed Ledger Technology (DLT)

Blockchain, the underlying technology behind cryptocurrencies like Bitcoin, represents a radical departure from traditional centralized databases. Distributed Ledger Technology (DLT) offers a secure, transparent, and immutable way to record transactions across a network of computers. Its implications for finance are profound.

- Cryptocurrencies: Bitcoin pioneered the concept of decentralized digital money, enabling peer-to-peer transactions without intermediaries. While volatile, cryptocurrencies are fostering innovation in the payment space and challenging traditional monetary systems.

- Enhanced Security and Transparency: DLT’s cryptographic security and immutable ledger entries offer a high degree of trust and transparency, reducing the risk of fraud and tampering. This is particularly appealing for cross-border payments, supply chain finance, and asset tokenization.

- Streamlined Settlements and Reduced Costs: By eliminating intermediaries and automating processes through smart contracts, DLT can significantly speed up settlement times for financial transactions (e.g., cross-border payments, securities trading) and reduce associated costs.

- Tokenization of Assets: DLT enables the “tokenization” of real-world assets (e.g., real estate, art, commodities) into digital tokens that can be easily traded and fractionalized, potentially democratizing investment and creating new liquidity in illiquid markets.

While still in relatively early stages of mainstream adoption for traditional finance, the potential of blockchain and DLT to revolutionize infrastructure, remove friction, and enhance trust in financial transactions is immense. Many large financial institutions are actively exploring and implementing DLT solutions for various applications.

Cloud Computing and Open APIs

Cloud computing and the widespread adoption of Application Programming Interfaces (APIs) are fundamental enablers of modern fintech, creating a more agile, interconnected, and innovative financial ecosystem.

- Scalability and Cost Efficiency: Cloud infrastructure allows fintech companies and traditional banks to scale their operations rapidly without massive upfront hardware investments. It provides flexible, on-demand computing resources, reducing operational costs and accelerating development cycles.

- Increased Collaboration and Innovation (Open Banking): Open APIs allow different financial platforms and applications to securely communicate and share data (with user consent). This is the foundation of “Open Banking,” where third-party developers can build new services on top of a bank’s data, leading to a surge of innovative personal finance apps, budgeting tools, and specialized lending solutions.

- Faster Time-to-Market: By leveraging cloud services and APIs, fintech startups can develop and deploy new products much faster than traditional institutions, driving rapid innovation and competition.

- Data Aggregation: APIs are critical for services that aggregate financial data from multiple sources (e.g., personal finance management apps), providing users with a comprehensive view of their financial health across different banks and investment accounts.

Cloud computing provides the flexible infrastructure, and open APIs are the connective tissue that enables the modern, interconnected fintech landscape. Together, they foster an environment of rapid innovation, allowing new services to be born quickly and integrated seamlessly into the broader financial ecosystem. This shift towards an open, interconnected financial world is fundamentally changing how consumers interact with their money and how financial services are delivered. Understanding fintech trends and technologies is crucial for staying competitive.

Regulatory Responses and Challenges in Fintech’s History

As fintech has evolved, so too has the need for regulatory frameworks to govern its operations, protect consumers, and ensure financial stability. The history of fintech is replete with instances where innovation outpaced regulation, leading to both opportunities and challenges. Regulators often find themselves playing catch-up, balancing the need to foster innovation with the imperative to mitigate risks.

Early Regulations and Consumer Protection

Even in the earliest days of financial innovation, rules were necessary. Laws regarding usury, contracts, and banking reserves emerged to provide order and protect participants. With the rise of modern banking, regulators focused on ensuring the solvency of institutions and preventing systemic risks.

- Banking Acts: Following financial crises, governments enacted comprehensive banking legislation (e.g., in the U.S., the Federal Reserve Act in 1913, Glass-Steagall Act in 1933) to stabilize the financial system, regulate money supply, and protect depositors. These laws primarily targeted traditional banks but set precedents for oversight.

- Consumer Credit Protection: As credit cards and consumer lending grew, regulations aimed at fair lending practices, disclosure of terms, and protection against predatory lending became crucial (e.g., Truth in Lending Act in 1968). These were broad mandates that later had to be adapted for digital credit.

- Anti-Money Laundering (AML) and Know Your Customer (KYC): Increased global financial flows led to the development of robust AML and KYC regulations to prevent illicit financial activities. These rules, initially designed for traditional banks, pose significant compliance challenges for nimble fintech startups.

Historically, regulation has been reactive, responding to past crises or emerging threats. This pattern largely continues in the fintech space, with regulators grappling with new technologies and business models.

Navigating the Digital Landscape: New Regulatory Frontiers

The rapid pace of fintech innovation in the internet and mobile eras has presented unprecedented challenges for regulators. New products and services often fall outside existing regulatory categories, creating ambiguity and potential risks.

- Data Privacy and Security: With vast amounts of personal financial data being handled by fintechs, paramount concerns include data breaches, misuse of information, and ensuring strong cybersecurity. Regulations like GDPR (Europe) and CCPA (California) have set new global standards for data protection, directly impacting fintech operations.

- Cryptocurrency Regulation: Cryptocurrencies, with their decentralized nature, have been a particularly difficult area to regulate. Governments worldwide are grappling with questions of classification (currency, commodity, security?), consumer protection, taxation, and their potential use in illicit activities. Responses vary widely, from outright bans in some countries to embrace as legal tender in others.

- Open Banking Directives: Initiatives like PSD2 (Payment Services Directive 2) in Europe have mandated open banking, requiring banks to provide third parties with access to customer data (with consent). This represents a proactive regulatory push to foster competition and innovation, but also creates new challenges around data governance and security of shared information.

- Regulatory Sandboxes: Recognizing the need to foster innovation while ensuring oversight, many regulators have introduced “regulatory sandboxes.” These allow fintech companies to test new products and services in a controlled environment with relaxed regulatory requirements, under the close supervision of authorities. This approach aims to accelerate innovation while managing risks.

The challenge for regulators in the fintech age is to strike a delicate balance: fostering an environment where innovation can thrive and benefit consumers, while simultaneously ensuring financial stability, preventing systemic risks, and protecting consumers from new forms of fraud or exploitation. This often requires new regulatory tools, greater international cooperation, and a willingness to adapt existing frameworks to fit rapidly evolving technological realities. The discussion around central bank digital currencies (CBDCs) is another key area illustrating regulatory attempts to proactively shape the future of digital money, rather than just reacting to private sector innovations.

The Future of Fintech: Trends and Predictions

The history of fintech shows a clear trajectory of increasing speed, accessibility, and personalization. Looking ahead, this momentum is set to continue, driven by ever-more sophisticated technologies and evolving consumer expectations. The future of fintech promises an even more integrated, intelligent, and potentially transformative financial landscape.

Hyper-Personalization and Embedded Finance

The era of generic financial products is rapidly fading. Fueled by AI and vast data analytics capabilities, financial services will become increasingly tailored to individual users, often integrated seamlessly into non-financial contexts.

- AI-Driven Financial Advisors: Beyond current robo-advisors, AI will offer proactive, real-time financial advice, anticipating needs and suggesting optimal financial actions based on spending patterns, income, and life events. Think of an AI that nudges you to save more for a specific goal or automatically adjusts your investment portfolio based on changing market conditions and your personal risk profile.

- Embedded Finance: Financial services will become “invisible,” integrated directly into the platforms and experiences where consumers already spend their time. For example, buying a car from an online marketplace might include instant financing options embedded directly into the checkout process, or a retail app offering “buy now, pay later” schemes seamlessly. This blurs the lines between finance and other industries, making financial decisions more convenient and contextual.

- Proactive Financial Wellness: Fintech will move beyond reactive problem-solving to proactive wellness. Apps will predict future cash flow issues, suggest alternative payment arrangements, or automatically optimize recurring expenses and subscriptions.

Web3, Metaverse, and Decentralized Finance (DeFi)

The emerging concepts of Web3, the Metaverse, and the expansion of Decentralized Finance (DeFi) are poised to create entirely new financial ecosystems and forms of value exchange.

- Decentralized Finance (DeFi): Built on blockchain technology, DeFi aims to recreate traditional financial services (lending, borrowing, trading, insurance) using smart contracts without central intermediaries. This promises greater transparency, accessibility, and potentially lower costs. While still nascent and volatile, DeFi’s potential to disintermediate traditional finance is significant.

- Metaverse Economy: As virtual worlds become more immersive and transactional, new economies will emerge within the Metaverse. This will require new forms of digital identity, payment systems, digital asset ownership (NFTs), and financial services tailored to virtual environments, including lending against virtual assets or insuring digital goods.

- Digital Asset Revolution: The tokenization of assets (both physical and digital) will continue to grow. This means fractional ownership of high-value assets and new forms of investment opportunities will become accessible to a wider range of investors, enhancing liquidity and opening new markets.

These trends suggest a shift towards a more fluid, interconnected, and user-empowered financial world, where traditional institutions will likely need to adapt or partner with innovative tech solutions to remain relevant.

Quantum Computing and Enhanced Security

While still primarily in the research phase, quantum computing holds revolutionary potential for fintech, particularly in areas of security and complex data analysis. However, it also presents significant challenges.

- Unbreakable Encryption: Quantum cryptography could lead to virtually unbreakable encryption methods, drastically improving the security of financial transactions and data protection, potentially rendering current encryption standards obsolete.

- Advanced Financial Modeling: Quantum computers’ ability to solve complex problems far beyond the scope of classical computers could revolutionize financial modeling, risk assessment, and algorithmic trading, leading to more accurate predictions and optimized strategies.

- New Security Threats: The same power that enables enhanced encryption could also be used to break existing cryptographic systems, posing a “quantum threat” to current digital security. This necessitates the development of “post-quantum cryptography” to protect financial data against future quantum attacks.

The interplay of these advanced technologies and the evolving regulatory landscape will shape the coming decades of fintech. The emphasis will increasingly be on seamless, secure, and personalized financial experiences, driven by intelligent automation and accessible through interconnected digital ecosystems. The importance of financial literacy will only grow as these tools become more sophisticated.

Comparative Overview of Fintech Eras

To fully appreciate the journey of financial technology, it’s helpful to consider how each era built upon the last, transforming the core aspects of financial services over time. This comparative table highlights the key characteristics, dominant technologies, and primary beneficiaries across different historical periods.

| Fintech Era | Key Characteristics | Dominant Technologies | Primary Beneficiaries | Impact on Accessibility |

|---|---|---|---|---|

| Ancient/Pre-Industrial (3500 BCE – 1700s) | Basic record-keeping, manual transfers, localized finance. | Clay tablets, coinage, bills of exchange, double-entry bookkeeping. | Merchants, monarchs, early bankers. | Limited, primarily for wealthy or mercantile class. |

| Industrial Age (1800s – 1950s) | Mechanized processes, rapid communication, national banking. | Telegraph, mechanical calculators, punch card systems, telephones. | Businesses, early mass markets, national economies. | Increased for urban populations and commerce. |

| Digital Dawn (1950s – 1990s) | Automated back office, self-service options, global interbank networks. | Mainframe computers, ATMs, SWIFT, early electronic funds transfer. | Large financial institutions, corporations, early adopters. | Enhanced convenience, 24/7 ATM access. |

| Internet Age (1990s – 2000s) | Online banking, e-commerce payments, digital trading. | World Wide Web, secure servers, payment gateways (e.g., PayPal), email. | Online consumers, early e-commerce businesses, day traders. | Widespread remote access, lower transaction costs. |

| Mobile Revolution (2000s – 2020s) | Mobile-first services, fintech startups, hyper-personalization. | Smartphones, mobile apps, cloud computing, APIs. | General consumers, underserved populations, agile startups. | Ubiquitous access, tailored solutions, financial inclusion. |

| Future Fintech (2026 and Beyond) | AI-driven intelligence, decentralized finance, embedded experiences, virtual economies. | AI/ML, Blockchain/DLT, Quantum Computing, IoT, Metaverse platforms. | Any user with internet access, autonomous systems, creators. | Seamless integration, proactive advice, global decentralized access. |

This table illustrates a clear progression from manual, localized, and exclusive financial services to automated, global, and increasingly inclusive ones. Each technological leap has democratized access to financial tools, reduced friction, and expanded the scope of what finance can achieve. The modern consumer benefits directly from centuries of cumulative innovation, often without even realizing the deep historical roots of the digital services they use daily.

Frequently Asked Questions

Q1: What is the primary definition of fintech?

A1: Fintech, short for financial technology, refers to the application of technology to improve and automate the delivery and use of financial services. This broad definition encompasses everything from ancient accounting methods to modern mobile banking apps and blockchain-based systems.

Q2: When did fintech truly begin, as a concept?

A2: While the term “fintech” gained prominence in the 2000s, the concept of using technology to enhance finance dates back to ancient times. Early forms include the use of cuneiform for financial records in Mesopotamia, standardized coinage, bills of exchange in medieval Europe, and double-entry bookkeeping. Anytime technology was applied to improve financial operations, it was a form of fintech.

Q3: How did the telegraph impact early financial markets?

A3: The telegraph, introduced in the mid-19th century, revolutionized financial markets by enabling near-instantaneous communication of financial information across long distances. This led to faster price discovery, more efficient markets, facilitated arbitrage opportunities, and began to integrate geographically disparate financial centers into a more cohesive global system.

Q4: What role did mainframes play in the history of fintech?

A4: In the mid-20th century, mainframe computers were pivotal in automating large-scale banking operations. They enabled banks to process massive volumes of transactions, manage customer accounts digitally, and run early credit card systems. Mainframes laid the essential digital infrastructure for modern banking and were crucial for scaling financial services beyond manual processes.

Q5: What are some key future trends in fintech?

A5: Key future trends in fintech include hyper-personalization of financial services driven by AI and machine learning, the increasing prevalence of embedded finance (financial services seamlessly integrated into non-financial platforms), the growth of decentralized finance (DeFi) on blockchain, the development of financial economies within the Metaverse, and advancements in secure transactions through technologies like quantum computing and post-quantum cryptography.

The Comprehensive History of Fintech: From Ancient Times to Digital Dominance

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

Understanding the Evolution of Financial Technology

The term “fintech” might sound like a modern buzzword, conjuring images of sleek financial apps and virtual currencies. However, the conceptual history of fintech stretches back much further than most realize. At its core, fintech is simply the application of technology to improve financial services. This broad definition allows us to trace its roots from the very beginnings of organized commerce and banking to the hyper-connected, real-time financial world we inhabit today.

From the first systems for currency exchange and credit to the development of sophisticated algorithms for algorithmic trading and artificial intelligence-driven financial advice, technology has consistently shaped and reshaped how we manage our money. This journey is not linear; it’s a tapestry woven with threads of innovation, societal changes, economic upheavals, and regulatory responses. Each era brought its own set of challenges and, crucially, technological solutions that pushed the boundaries of what was possible in finance.

At fin3go, we believe that understanding this historical context is crucial for anyone engaging with personal finance today. It provides perspective on why certain financial products exist, how they evolved, and what forces are currently driving the next wave of disruption. It helps us appreciate the intricate dance between human ingenuity and technological advancement that has defined our financial lives for centuries. This comprehensive look at the history of fintech will explore key milestones, pivotal inventions, and the overarching trends that have led us to the current landscape of digital banking, mobile payments, and sophisticated investment platforms.

Early Forms of Financial Innovation and Technology

While the term “fintech” is relatively new, the underlying concept of using advanced tools to manage money is ancient. Early civilizations, driven by the need for trade, record-keeping, and wealth management, developed rudimentary yet effective financial technologies. These early innovations laid the groundwork for complex financial systems thousands of years later.

Ancient Accounting and Currency Systems

The earliest forms of financial technology can be traced back to the dawn of civilization. In Mesopotamia, around 3500-3000 BCE, Sumerians developed cuneiform writing on clay tablets not just for literature, but extensively for keeping detailed records of agricultural transactions, loans, and taxes. This was a critical technological leap for managing economic activity and establishing rudimentary forms of credit.

- Clay Tablets and Cuneiform: Used for tracking debts, payments, and trade. Essential for the function of early economies and the tracking of communal resources.

- Barter Systems and Early Currencies: While not strictly “technology,” the standardization of certain commodities (like salt, shells, or metals) as a medium of exchange was a technological innovation in facilitating trade beyond direct barter.

- Weights and Measures: Standardized systems for weight and measurement were crucial for fair trade and the accurate valuation of goods, a fundamental precursor to standardized currency.

The Lydians, a kingdom in ancient Anatolia, are credited with inventing the first standardized coinage around the 7th century BCE. These electrum coins, stamped with official insignia, were a groundbreaking technological advancement. They offered a portable, durable, and verifiable medium of exchange, revolutionizing trade and wealth storage far beyond the limitations of bulk commodities.

The Birth of Banking and Commercial Instruments

During the medieval and Renaissance periods, especially in Italian city-states like Florence and Venice, banking began to take a more recognizable shape. Merchants and moneylenders developed sophisticated systems for managing large sums of money, facilitating international trade, and extending credit.

- Bills of Exchange: These instruments, essentially early forms of checks or promissory notes, allowed merchants to transfer funds across long distances without physically moving large quantities of gold or silver, mitigating risks of theft and simplifying cross-border transactions. This was an ingenious solution to a significant logistical and security challenge.

- Double-Entry Bookkeeping: Developed in Italy in the 14th century, this accounting method provided a comprehensive and error-checking system for tracking financial transactions. Luca Pacioli’s 1494 treatise codified these practices, which remain the foundation of modern accounting. This systematization dramatically increased transparency and accuracy in financial dealings.

- Goldsmiths as Early Banks: In England, goldsmiths, with their secure vaults, began offering storage for valuables and later issued promissory notes (early banknotes) against deposits. These notes circulated as currency, and the goldsmiths evolved into the first true banks, offering loans and managing accounts.

These developments, while mechanical rather than electronic, represent critical early iterations of financial technology, solving problems of security, efficiency, and scalability that continue to drive fintech innovation today. The need for faster, safer, and more reliable financial transactions has consistently been a catalyst for technological advancement in finance.

[INLINE IMAGE 1: place after second H2 | alt=”history of fintech concept illustration”]

The Industrial Age: Mechanization and Communication

The Industrial Revolution, beginning in the late 18th century, brought about profound changes in manufacturing, transportation, and communication. These advancements, while not directly financial, had a transformative impact on how financial services were conducted, making them faster, more integrated, and accessible to a wider populace. The mechanization of processes and the birth of rapid communication laid the groundwork for modern banking infrastructure.

Telegraphy and the Global Financial Markets

The invention and widespread adoption of the telegraph in the mid-19th century represented a seismic shift in financial communication. Before the telegraph, news of financial markets, stock prices, and economic events traveled at the speed of a ship or a horse. This meant significant delays and regional price discrepancies.

- Instantaneous Information Transfer: The telegraph allowed for near-instantaneous transmission of information across continents. Financial institutions could receive real-time stock quotes, commodity prices, and news from distant markets.

- Arbitrage Opportunities and Market Efficiency: This rapid information flow enabled arbitrage, where investors could profit from price differences in different markets. More importantly, it led to greater overall market efficiency, as information quickly disseminated and prices converged.

- Consolidation of Markets: The telegraph facilitated the integration of geographically disparate financial markets, paving the way for truly global financial systems. A crisis in London could almost immediately affect markets in New York.

The transatlantic telegraph cable, completed in 1866, was a monumental achievement that dramatically shrunk the world for finance, enabling business transactions and market updates between Europe and North America to occur within minutes rather than weeks. This was an early, powerful example of how communication technology drives financial interconnectedness.

Early Computing and Mechanical Accounting

As businesses grew in scale and complexity during the late 19th and early 20th centuries, manual accounting became increasingly cumbersome and prone to error. This spurred the development of mechanical and electro-mechanical devices designed to automate financial calculations and record-keeping.

- Adding Machines and Calculators: Mechanical adding machines became standard in banks and businesses for performing arithmetic operations quickly and accurately. These were indispensable for daily banking operations, such as tallying deposits and withdrawals.

- Punch Card Systems: Herman Hollerith’s tabulating machine, developed for the 1890 U.S. Census, utilized punch cards to process large datasets. This technology, later commercialized by IBM, revolutionized data processing for large organizations, including government agencies and insurance companies, making the handling of vast numbers of financial records feasible.

- Typewriters and Duplicators: While not strictly computational, the proliferation of typewriters and early duplicating machines significantly improved the efficiency of producing financial documents, contracts, and correspondence, speeding up administrative processes within financial institutions.

These early “fintech” tools, while crude by today’s standards, represented significant advancements in efficiency, accuracy, and scalability for managing financial information. They demonstrated a clear trend: as financial operations become more complex, the demand for technological solutions to manage that complexity inevitably follows. This era laid the groundwork for the digital revolution by proving the value of automating and systematizing financial processes.

The Dawn of Digital: Mainframes and Early Automation

The mid-20th century witnessed the birth of true electronic computing, ushering in an era of unprecedented automation potential for the financial industry. Mainframe computers, though massive and expensive, began to transform banking operations, moving beyond mechanical assistance to digital processing. This period marked the tangible beginnings of modern fintech.

Mainframe Computers in Banking

Starting in the 1950s and accelerating through the 1960s, mainframe computers began to be adopted by large banks and financial institutions. These powerful machines provided the capability to store, process, and manage vast quantities of financial data, something previously unimaginable. The transition from manual ledger books and punch cards to magnetic tapes and digital databases was revolutionary.

- Automated Transaction Processing: Mainframes enabled banks to automate the clearing and settlement of checks, manage customer accounts, and process loan applications with much greater speed and accuracy. This significantly reduced manual errors and processing times.

- Early Credit Card Systems: The rise of credit cards in the 1950s and 60s (e.g., Diners Club, BankAmericard, MasterCard) was heavily reliant on mainframe technology for transaction authorization, billing, and account management. Without mainframes, the scale and complexity of managing millions of credit accounts would have been impractical.

- Data Management and Reporting: Banks could now generate complex financial reports, analyze customer behavior, and manage their vast portfolios more effectively, leading to better risk management and strategic planning.

The development of industry standards like SWIFT (Society for Worldwide Interbank Financial Telecommunication) in 1973 further cemented the role of digital networks. SWIFT provided a standardized, secure messaging system for financial transactions between banks globally, creating a foundation for international payments and interbank connectivity that still operates today. This was a critical step in creating a global, interconnected financial infrastructure based on digital communication.

ATMs and Self-Service Banking

One of the most visible and impactful innovations of this digital dawn was the Automated Teller Machine (ATM). The first functional ATM was introduced in London in June 1967 by Barclays. It was a revolutionary concept: self-service banking that allowed customers to access their funds outside of traditional bank hours and without needing a human teller.

- Around-the-Clock Access: ATMs provided unprecedented convenience, liberating customers from the constraints of banking hours. This significantly improved customer experience and accessibility to funds.

- Reduced Branch Overhead: For banks, ATMs offered a way to reduce operational costs associated with manned teller stations and allowed for greater scalability without proportional increases in staffing.

- Network Expansion: The subsequent development of ATM networks (like Plus and Cirrus) allowed customers to withdraw cash from almost any bank, anywhere, further enhancing convenience and solidifying the concept of interconnected digital finance.

The ATM was a pioneer in self-service digital finance, foreshadowing the mobile banking apps and online platforms that would follow decades later. It taught consumers to trust machines with their money and paved the way for broader adoption of digital financial services, fundamentally changing the daily interaction people had with their banks. It was an early demonstration of how technology could empower individuals to manage their finances more independently.

[INLINE IMAGE 2: place after fourth H2 | alt=”history of fintech comparison illustration”]

The Internet Age: Online Banking and E-Commerce

The commercialization and widespread adoption of the internet in the 1990s marked another transformative era for fintech. The ability to connect millions of computers globally opened up entirely new avenues for financial services, moving from internal bank automation to direct-to-consumer digital offerings. This period saw the rise of online banking, e-commerce payment systems, and the initial foray into digital investment platforms.

The Rise of Online Banking

Initially hesitant due to security concerns, financial institutions gradually embraced the internet as a new channel for delivering services. Early online banking platforms, emerging in the mid-1990s, offered basic functionalities that were a revelation for customers accustomed to branch visits or phone calls.

- Remote Access: Customers could check account balances, view transaction history, and transfer funds between their accounts from the comfort of their homes or offices, at any time. This dramatically increased convenience and control over personal finances.

- Cost Efficiency for Banks: Online banking reduced the need for expensive physical branches and significantly lowered the operational costs associated with traditional customer service, as many routine inquiries could be handled digitally.

- Enhanced Financial Management: With transactional data readily available online, individuals gained better tools for budgeting and tracking their spending habits, albeit through static web interfaces initially.

Early pioneers like Stanford Federal Credit Union and Presidential Bank were among the first to offer internet banking in 1994 and 1995, respectively. Their success, combined with the growing dot-com enthusiasm, spurred broader adoption across the banking sector. The security protocols, while rudimentary by today’s standards, continually evolved to build user trust and enable wider acceptance.

E-commerce and Digital Payments

The internet made e-commerce possible, but for e-commerce to flourish, secure and efficient digital payment systems were essential. This need spurred the development of specialized fintech companies focused entirely on facilitating online transactions.

- PayPal and Online Payment Gateways: Companies like PayPal, founded in 1998, revolutionized peer-to-peer and merchant payments online. They provided a trusted intermediary between buyers and sellers, simplifying transactions and adding a layer of security. Payment gateways integrated with e-commerce websites became standard, allowing consumers to make purchases with credit cards or digital wallets without needing to re-enter details repeatedly.

- Increased Consumer Confidence: The development of secure socket layer (SSL) encryption and other security measures helped foster consumer confidence in online transactions, which was crucial for the growth of both e-commerce and digital finance.

- Early Digital Wallets: While not as sophisticated as today’s mobile wallets, early digital payment systems laid the groundwork for storing payment information and streamlining checkout processes, accelerating the adoption of online shopping.

This period also saw the emergence of online brokerages like E*TRADE and Charles Schwab, which democratized access to stock trading. Rather than relying on traditional brokers, individual investors could research and execute trades directly from their personal computers, often at significantly lower costs. This was a critical step in making investment services more accessible and empowering for the average person, further blurring the lines between traditional financial institutions and technology providers.

The Mobile Revolution and the Rise of “True” Fintech

The proliferation of smartphones and high-speed mobile internet connectivity starting in the late 2000s ushered in what many consider the true “fintech” era. This period is characterized by financial services being delivered directly to consumers’ pockets, enabling unprecedented access, convenience, and personalization. The mobile revolution redefined expectations for financial interactions and spurred a wave of disruptive innovation.

Smartphone Adoption and Mobile Banking

The launch of the iPhone in 2007, followed by Android devices, rapidly transformed the global technology landscape. With powerful computing capabilities and internet access in hand, consumers quickly embraced mobile applications for every aspect of their lives, including finance.

- Banking in Your Pocket: Mobile banking apps became standard offerings from traditional banks, allowing users to perform almost all functions previously reserved for online banking or ATMs: checking balances, transferring funds, paying bills, and even depositing checks via image capture (mobile check deposit).

- Enhanced User Experience: Mobile apps offered intuitive interfaces, biometric authentication (fingerprint, facial recognition), and personalized notifications, making financial management more engaging and secure.

- Location-Based Services: GPS capabilities enabled banks to offer features like ATM locators and personalized offers based on a user’s location, adding another layer of convenience.

The ease and immediacy of mobile banking quickly made it the preferred method of interaction for millions, significantly reducing branch visits and paving the way for truly branchless banking models. This shift empowered users with continuous access to their financial information and control.

Emergence of Fintech Startups and Niche Solutions

The mobile revolution, combined with the availability of cloud computing and open APIs, dramatically lowered the barrier to entry for new financial service providers. A new breed of “fintech” startups emerged, often focused on specific, underserved market segments or pain points that traditional banks had overlooked.

- Digital-Only Banks (Neobanks): Companies like Chime, N26, and Revolut emerged as entirely digital banking alternatives, offering streamlined accounts, fee-free services, and advanced mobile features without any physical branches. They leveraged technology to provide a superior, cost-effective customer experience.

- Peer-to-Peer (P2P) Payments: Apps like Venmo, Square Cash App, and Zelle made sending money between individuals as easy as sending a text message, eroding the dominance of traditional money transfer services.

- Personal Finance Management (PFM) Apps: Services like Mint and YNAB provided sophisticated tools for budgeting, expense tracking, and goal setting by aggregating data from multiple financial accounts, giving users a holistic view of their financial health.

- Specialized Lending Platforms: Online lenders (e.g., SoFi for student loan refinancing, LendingClub for P2P loans) leveraged data analytics and proprietary algorithms to offer faster, more personalized loan products outside traditional banking channels.

- Robo-Advisors: Services such as Betterment and Wealthfront automated investment management by using algorithms to build and manage diversified portfolios based on a user’s risk tolerance and financial goals, making sophisticated investment advice accessible to a broader audience at a lower cost.

This period cemented “fintech” as a distinct industry segment, characterized by agility, customer-centric design, and the clever application of technology to traditional financial challenges. The competition from these nimble startups forced traditional financial institutions to innovate more rapidly and adopt similar technologies, blurring the lines further between legacy players and new challengers. The mobile phone transformed from a communication device into a personal financial hub, marking an irreversible shift in how people interact with their money.

Key Technologies Driving Modern Fintech Disruption

The ongoing evolution of fintech is fueled by the relentless advance of several core technologies. These innovations are not just making existing financial services more efficient but are enabling entirely new paradigms of financial interaction, reshaping markets, and creating unprecedented opportunities. Understanding these technological pillars is crucial for comprehending the current and future landscape of finance.

Artificial Intelligence and Machine Learning

AI and ML are perhaps the most transformative technologies impacting fintech today. They enable machines to learn from data, identify patterns, make predictions, and automate complex decision-making processes that were once the exclusive domain of human expertise.

- Fraud Detection and Risk Assessment: ML algorithms can analyze vast datasets of transactions in real-time, identifying anomalous patterns indicative of fraud with much greater accuracy and speed than traditional rule-based systems. They also power sophisticated credit scoring models that can assess risk more dynamically and inclusively, potentially expanding access to credit.

- Personalized Financial Advice (Robo-Advisors): AI powers robo-advisors that offer automated, data-driven investment advice and portfolio management. These systems can tailor recommendations based on individual financial goals, risk tolerance, and market conditions, making sophisticated wealth management accessible and affordable.

- Chatbots and Customer Service: AI-powered chatbots and virtual assistants are increasingly handling routine customer inquiries, account management, and providing instant support, improving efficiency and customer satisfaction. Advanced AI can even handle complex queries, enhancing the overall customer experience.

- Algorithmic Trading: In capital markets, AI and ML are used to analyze market data, predict trends, and execute trades at high speeds, optimizing investment strategies and managing vast portfolios.

The ability of AI/ML to process and derive insights from massive amounts of data is fundamentally changing how financial institutions operate, from backend risk management to front-end customer engagement.

Blockchain and Distributed Ledger Technology (DLT)

Blockchain, the underlying technology behind cryptocurrencies like Bitcoin, represents a radical departure from traditional centralized databases. Distributed Ledger Technology (DLT) offers a secure, transparent, and immutable way to record transactions across a network of computers. Its implications for finance are profound.

- Cryptocurrencies: Bitcoin pioneered the concept of decentralized digital money, enabling peer-to-peer transactions without intermediaries. While volatile, cryptocurrencies are fostering innovation in the payment space and challenging traditional monetary systems.

- Enhanced Security and Transparency: DLT’s cryptographic security and immutable ledger entries offer a high degree of trust and transparency, reducing the risk of fraud and tampering. This is particularly appealing for cross-border payments, supply chain finance, and asset tokenization.

- Streamlined Settlements and Reduced Costs: By eliminating intermediaries and automating processes through smart contracts, DLT can significantly speed up settlement times for financial transactions (e.g., cross-border payments, securities trading) and reduce associated costs.

- Tokenization of Assets: DLT enables the “tokenization” of real-world assets (e.g., real estate, art, commodities) into digital tokens that can be easily traded and fractionalized, potentially democratizing investment and creating new liquidity in illiquid markets.

While still in relatively early stages of mainstream adoption for traditional finance, the potential of blockchain and DLT to revolutionize infrastructure, remove friction, and enhance trust in financial transactions is immense. Many large financial institutions are actively exploring and implementing DLT solutions for various applications.

Cloud Computing and Open APIs

Cloud computing and the widespread adoption of Application Programming Interfaces (APIs) are fundamental enablers of modern fintech, creating a more agile, interconnected, and innovative financial ecosystem.

- Scalability and Cost Efficiency: Cloud infrastructure allows fintech companies and traditional banks to scale their operations rapidly without massive upfront hardware investments. It provides flexible, on-demand computing resources, reducing operational costs and accelerating development cycles.

- Increased Collaboration and Innovation (Open Banking): Open APIs allow different financial platforms and applications to securely communicate and share data (with user consent). This is the foundation of “Open Banking,” where third-party developers can build new services on top of a bank’s data, leading to a surge of innovative personal finance apps, budgeting tools, and specialized lending solutions.

- Faster Time-to-Market: By leveraging cloud services and APIs, fintech startups can develop and deploy new products much faster than traditional institutions, driving rapid innovation and competition.

- Data Aggregation: APIs are critical for services that aggregate financial data from multiple sources (e.g., personal finance management apps), providing users with a comprehensive view of their financial health across different banks and investment accounts.

Cloud computing provides the flexible infrastructure, and open APIs are the connective tissue that enables the modern, interconnected fintech landscape. Together, they foster an environment of rapid innovation, allowing new services to be born quickly and integrated seamlessly into the broader financial ecosystem. This shift towards an open, interconnected financial world is fundamentally changing how consumers interact with their money and how financial services are delivered. Understanding fintech trends and technologies is crucial for staying competitive.

Regulatory Responses and Challenges in Fintech’s History

As fintech has evolved, so too has the need for regulatory frameworks to govern its operations, protect consumers, and ensure financial stability. The history of fintech is replete with instances where innovation outpaced regulation, leading to both opportunities and challenges. Regulators often find themselves playing catch-up, balancing the need to foster innovation with the imperative to mitigate risks.

Early Regulations and Consumer Protection

Even in the earliest days of financial innovation, rules were necessary. Laws regarding usury, contracts, and banking reserves emerged to provide order and protect participants. With the rise of modern banking, regulators focused on ensuring the solvency of institutions and preventing systemic risks.

- Banking Acts: Following financial crises, governments enacted comprehensive banking legislation (e.g., in the U.S., the Federal Reserve Act in 1913, Glass-Steagall Act in 1933) to stabilize the financial system, regulate money supply, and protect depositors. These laws primarily targeted traditional banks but set precedents for oversight.

- Consumer Credit Protection: As credit cards and consumer lending grew, regulations aimed at fair lending practices, disclosure of terms, and protection against predatory lending became crucial (e.g., Truth in Lending Act in 1968). These were broad mandates that later had to be adapted for digital credit.

- Anti-Money Laundering (AML) and Know Your Customer (KYC): Increased global financial flows led to the development of robust AML and KYC regulations to prevent illicit financial activities. These rules, initially designed for traditional banks, pose significant compliance challenges for nimble fintech startups.

Historically, regulation has been reactive, responding to past crises or emerging threats. This pattern largely continues in the fintech space, with regulators grappling with new technologies and business models.

Navigating the Digital Landscape: New Regulatory Frontiers

The rapid pace of fintech innovation in the internet and mobile eras has presented unprecedented challenges for regulators. New products and services often fall outside existing regulatory categories, creating ambiguity and potential risks.

- Data Privacy and Security: With vast amounts of personal financial data being handled by fintechs, paramount concerns include data breaches, misuse of information, and ensuring strong cybersecurity. Regulations like GDPR (Europe) and CCPA (California) have set new global standards for data protection, directly impacting fintech operations.

- Cryptocurrency Regulation: Cryptocurrencies, with their decentralized nature, have been a particularly difficult area to regulate. Governments worldwide are grappling with questions of classification (currency, commodity, security?), consumer protection, taxation, and their potential use in illicit activities. Responses vary widely, from outright bans in some countries to embrace as legal tender in others.

- Open Banking Directives: Initiatives like PSD2 (Payment Services Directive 2) in Europe have mandated open banking, requiring banks to provide third parties with access to customer data (with consent). This represents a proactive regulatory push to foster competition and innovation, but also creates new challenges around data governance and security of shared information.

- Regulatory Sandboxes: Recognizing the need to foster innovation while ensuring oversight, many regulators have introduced “regulatory sandboxes.” These allow fintech companies to test new products and services in a controlled environment with relaxed regulatory requirements, under the close supervision of authorities. This approach aims to accelerate innovation while managing risks.

The challenge for regulators in the fintech age is to strike a delicate balance: fostering an environment where innovation can thrive and benefit consumers, while simultaneously ensuring financial stability, preventing systemic risks, and protecting consumers from new forms of fraud or exploitation. This often requires new regulatory tools, greater international cooperation, and a willingness to adapt existing frameworks to fit rapidly evolving technological realities. The discussion around central bank digital currencies (CBDCs) is another key area illustrating regulatory attempts to proactively shape the future of digital money, rather than just reacting to private sector innovations.

The Future of Fintech: Trends and Predictions

The history of fintech shows a clear trajectory of increasing speed, accessibility, and personalization. Looking ahead, this momentum is set to continue, driven by ever-more sophisticated technologies and evolving consumer expectations. The future of fintech promises an even more integrated, intelligent, and potentially transformative financial landscape.

Hyper-Personalization and Embedded Finance

The era of generic financial products is rapidly fading. Fueled by AI and vast data analytics capabilities, financial services will become increasingly tailored to individual users, often integrated seamlessly into non-financial contexts.

- AI-Driven Financial Advisors: Beyond current robo-advisors, AI will offer proactive, real-time financial advice, anticipating needs and suggesting optimal financial actions based on spending patterns, income, and life events. Think of an AI that nudges you to save more for a specific goal or automatically adjusts your investment portfolio based on changing market conditions and your personal risk profile.

- Embedded Finance: Financial services will become “invisible,” integrated directly into the platforms and experiences where consumers already spend their time. For example, buying a car from an online marketplace might include instant financing options embedded directly into the checkout process, or a retail app offering “buy now, pay later” schemes seamlessly. This blurs the lines between finance and other industries, making financial decisions more convenient and contextual.

- Proactive Financial Wellness: Fintech will move beyond reactive problem-solving to proactive wellness. Apps will predict future cash flow issues, suggest alternative payment arrangements, or automatically optimize recurring expenses and subscriptions.

Web3, Metaverse, and Decentralized Finance (DeFi)

The emerging concepts of Web3, the Metaverse, and the expansion of Decentralized Finance (DeFi) are poised to create entirely new financial ecosystems and forms of value exchange.

- Decentralized Finance (DeFi): Built on blockchain technology, DeFi aims to recreate traditional financial services (lending, borrowing, trading, insurance) using smart contracts without central intermediaries. This promises greater transparency, accessibility, and potentially lower costs. While still nascent and volatile, DeFi’s potential to disintermediate traditional finance is significant.

- Metaverse Economy: As virtual worlds become more immersive and transactional, new economies will emerge within the Metaverse. This will require new forms of digital identity, payment systems, digital asset ownership (NFTs), and financial services tailored to virtual environments, including lending against virtual assets or insuring digital goods.

- Digital Asset Revolution: The tokenization of assets (both physical and digital) will continue to grow. This means fractional ownership of high-value assets and new forms of investment opportunities will become accessible to a wider range of investors, enhancing liquidity and opening new markets.

These trends suggest a shift towards a more fluid, interconnected, and user-empowered financial world, where traditional institutions will likely need to adapt or partner with innovative tech solutions to remain relevant.

Quantum Computing and Enhanced Security

While still primarily in the research phase, quantum computing holds revolutionary potential for fintech, particularly in areas of security and complex data analysis. However, it also presents significant challenges.

- Unbreakable Encryption: Quantum cryptography could lead to virtually unbreakable encryption methods, drastically improving the security of financial transactions and data protection, potentially rendering current encryption standards obsolete.

- Advanced Financial Modeling: Quantum computers’ ability to solve complex problems far beyond the scope of classical computers could revolutionize financial modeling, risk assessment, and algorithmic trading, leading to more accurate predictions and optimized strategies.

- New Security Threats: The same power that enables enhanced encryption could also be used to break existing cryptographic systems, posing a “quantum threat” to current digital security. This necessitates the development of “post-quantum cryptography” to protect financial data against future quantum attacks.

The interplay of these advanced technologies and the evolving regulatory landscape will shape the coming decades of fintech. The emphasis will increasingly be on seamless, secure, and personalized financial experiences, driven by intelligent automation and accessible through interconnected digital ecosystems. The importance of financial literacy will only grow as these tools become more sophisticated.

Comparative Overview of Fintech Eras

To fully appreciate the journey of financial technology, it’s helpful to consider how each era built upon the last, transforming the core aspects of financial services over time. This comparative table highlights the key characteristics, dominant technologies, and primary beneficiaries across different historical periods.

| Fintech Era | Key Characteristics | Dominant Technologies | Primary Beneficiaries | Impact on Accessibility |

|---|---|---|---|---|

| Ancient/Pre-Industrial (3500 BCE – 1700s) | Basic record-keeping, manual transfers, localized finance. | Clay tablets, coinage, bills of exchange, double-entry bookkeeping. | Merchants, monarchs, early bankers. | Limited, primarily for wealthy or mercantile class. |