Understanding the Imperative: Why an Emergency Fund Isn’t Optional

An emergency fund is a dedicated stash of readily accessible money, separate from your regular checking or savings accounts, specifically earmarked for unforeseen financial crises. It’s not for a spontaneous vacation, a new gadget, or holiday shopping. Its purpose is singular: to protect you from financial ruin when the unexpected occurs. Think of it as your personal financial insurance policy, one that pays out without premiums and that you fully control.

The importance of an emergency fund cannot be overstated. In a world where economic stability can shift rapidly and personal circumstances can change in an instant, having a financial buffer is paramount. Without one, many individuals find themselves resorting to high-interest credit cards, personal loans, or even dipping into retirement savings when an emergency strikes. These actions can quickly lead to a crippling cycle of debt, delaying financial independence and making it exponentially harder to achieve other financial milestones.

Consider these common scenarios where an emergency fund proves invaluable:

- Job Loss or Reduction in Income: The average job search can take several months. An emergency fund can cover your essential living expenses during this period, allowing you to focus on finding new employment without the added stress of immediate financial strain.

- Unexpected Medical Bills: Even with health insurance, deductibles, co-pays, and uncovered services can lead to significant out-of-pocket costs. An emergency fund ensures you can prioritize your health without compromising your financial well-being.

- Car Repairs: A sudden transmission failure or a blown tire can cost hundreds, if not thousands, of dollars. For many, a reliable vehicle is crucial for work and daily life. An emergency fund prevents you from being stranded or taking on debt to get back on the road.

- Home Repairs: A burst pipe, a leaking roof, or a broken HVAC system can be costly and require immediate attention. Deferring such repairs can lead to greater damage and expense down the line.

- Family Emergencies: Unforeseen travel expenses for a family emergency or the need to support a loved one can quickly deplete regular savings.

Beyond the practical applications, an emergency fund offers immense psychological benefits. It provides peace of mind, reduces stress, and grants you a greater sense of control over your financial life. Knowing you have a safety net empowers you to make decisions based on your best interests, rather than being forced into difficult choices due to immediate financial pressures. In essence, it’s the bedrock upon which all other financial goals, from investing for retirement to building generational wealth, must be built.

How Much Do You Really Need? Setting Your Emergency Fund Target

One of the most common questions individuals ask when starting their emergency fund journey is, “How much should I save?” While there’s no one-size-fits-all answer, a widely accepted guideline is to aim for three to six months’ worth of essential living expenses. However, for those with less stable income, significant dependents, or specific health concerns, a target of six to twelve months may be more appropriate.

Determining your personal target requires a clear understanding of your financial situation. Here’s how to calculate it:

- Identify Your Essential Monthly Expenses: This is where the practice of “How To Create A Monthly Budget” becomes indispensable. You need to differentiate between needs and wants. Essential expenses typically include:

- Housing (rent/mortgage)

- Utilities (electricity, gas, water, internet)

- Groceries (basic food items)

- Transportation (car payments, fuel, public transit, insurance)

- Minimum debt payments (credit cards, student loans, personal loans)

- Health insurance premiums and essential medical costs

- Childcare or essential dependent care

Exclude discretionary spending like dining out, entertainment, subscriptions you can live without, or luxury items. The goal is to determine the absolute minimum you need to survive comfortably each month if your income suddenly ceased.

- Calculate Your Total Essential Monthly Expenses: Sum up all the essential categories. For example, if your essential expenses total $3,000 per month.

- Determine Your Target Range:

- For a 3-month fund: $3,000 x 3 = $9,000

- For a 6-month fund: $3,000 x 6 = $18,000

- For a 12-month fund: $3,000 x 12 = $36,000

Factors Influencing Your Emergency Fund Target:

- Job Security: If you work in a volatile industry or have a less secure job, leaning towards a larger fund (6-12 months) is prudent. If you have a highly stable job with high demand for your skills, 3-6 months might suffice.

- Dependents: If you have children, elderly parents, or other dependents relying on your income, a larger fund provides a greater cushion for their well-being.

- Health and Insurance: Individuals with chronic health conditions or those with high-deductible health insurance plans might benefit from a larger fund to cover potential medical costs.

- Multiple Income Streams: If you have diversified income sources (e.g., a full-time job and a significant side hustle), you might feel comfortable with a smaller fund, as a loss in one area may not completely eliminate your income.

- Debt Load: While an emergency fund is crucial, a heavy burden of high-interest debt (like credit card debt) might warrant a slightly different approach. Some experts suggest building a mini-emergency fund ($1,000-$2,000) first, then aggressively paying down high-interest debt, and then returning to build the full fund. This balance is key to optimizing your financial health.

Remember, building an emergency fund is a journey, not a sprint. Don’t be discouraged if your target seems daunting. Start with a smaller, achievable goal, like $1,000, and build from there. The most important thing is to start.

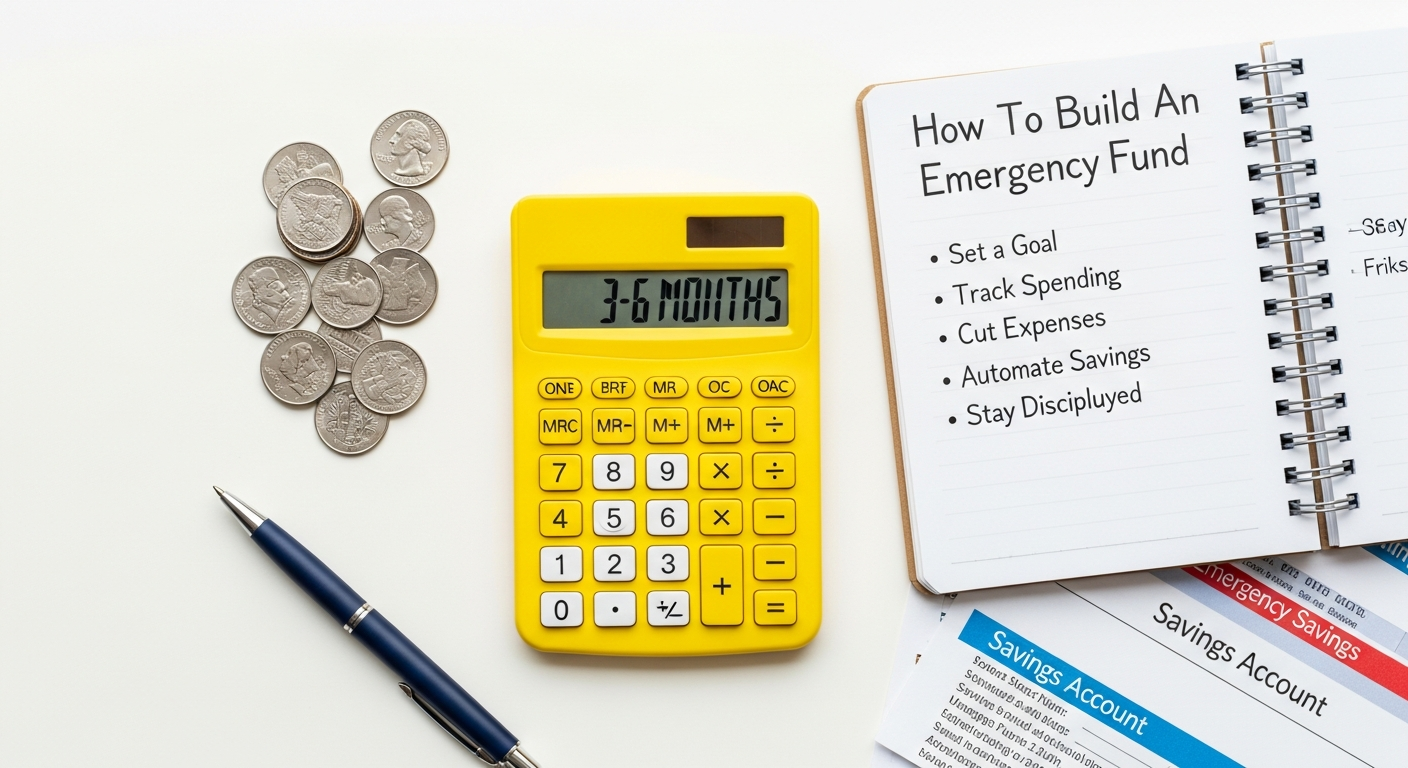

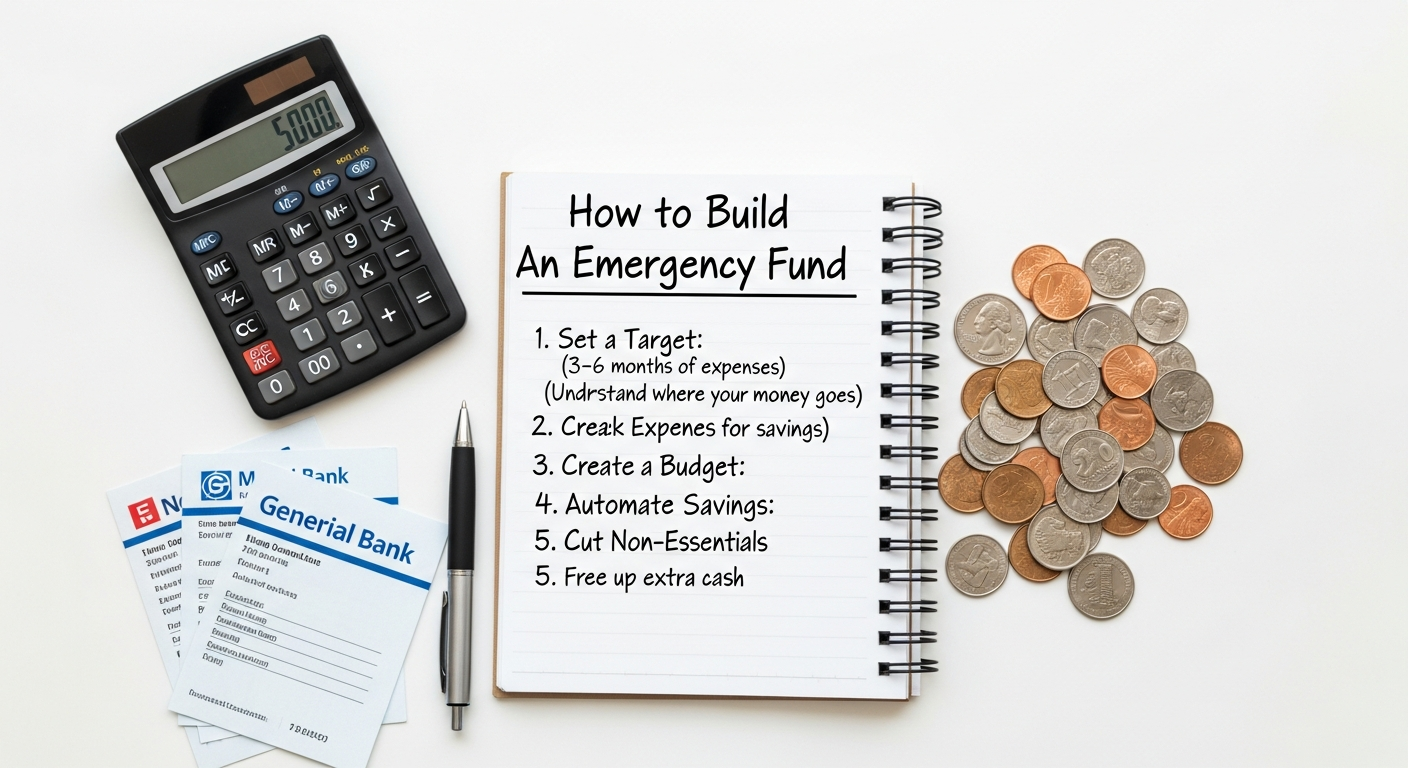

The Blueprint for Action: Practical Steps to Build Your Fund

Step 1: Assess Your Current Financial Standing with a Detailed Budget

Before you can save, you need to know where your money is going. This brings us back to the critical importance of “How To Create A Monthly Budget.”

- Track Your Income: List all sources of income, net of taxes and deductions.

- Track Your Expenses: Categorize every dollar you spend for at least a month, preferably two or three, to get an accurate picture. Use budgeting apps, spreadsheets, or even pen and paper.

- Identify Spending Habits: Where are you overspending? Where are there opportunities to cut back? This detailed analysis is the foundation for finding money to funnel into your emergency fund.

Step 2: Identify Areas for Cost Reduction and Optimize Your Spending

With a clear budget in hand, you can now pinpoint areas where you can free up cash. This is where the principles of “How To Negotiate Bills And Lower Expenses” come into play.

- Review Discretionary Spending: Cut back on non-essential items like dining out, entertainment, subscriptions, and impulse purchases. Even small cuts add up over time.

- Negotiate Bills: Call your service providers (internet, cable, cell phone, insurance) and ask for better rates. Research competitors’ offers and leverage them in your negotiation. Many companies are willing to reduce your bill to retain you as a customer.

- Reduce Fixed Costs: Can you refinance your mortgage or car loan? Are there cheaper insurance options? Explore ways to lower your recurring monthly obligations.

- Shop Smarter: Plan meals, use coupons, buy in bulk when appropriate, and avoid unnecessary trips to the grocery store.

- Temporary Frugality: For a period, embrace extreme frugality. Cook every meal at home, avoid all non-essential spending, and challenge yourself to live on as little as possible. This temporary sacrifice can fast-track your emergency fund growth.

Step 3: Boost Your Income (If Possible)

Cutting expenses is one side of the coin; increasing income is the other.

- Side Hustles: Explore opportunities to earn extra money outside your primary job. This could be freelancing, ride-sharing, dog walking, selling crafts online, or tutoring. Every extra dollar earned can go directly into your emergency fund.

- Sell Unused Items: Declutter your home and sell items you no longer need or use on platforms like eBay, Facebook Marketplace, or local consignment shops.

- Ask for a Raise: If you’ve been excelling at your job, consider asking for a raise. Document your achievements and present a strong case.

- Overtime: If available, pick up extra shifts or work overtime.

Step 4: Automate Your Savings

This is perhaps the most crucial step for consistent progress. Treat your emergency fund contribution like any other bill.

- Set Up Automatic Transfers: Schedule a recurring transfer from your checking account to your dedicated emergency savings account each payday. Even if it’s a small amount initially, consistency is key.

- Pay Yourself First: Make this transfer immediately after getting paid, before you have a chance to spend the money.

- Increase Contributions Gradually: As your financial situation improves or you find new ways to save/earn, incrementally increase the amount you automatically transfer.

Step 5: Choose the Right Account for Your Emergency Fund

Where you keep your emergency fund is almost as important as having one.

- High-Yield Savings Account (HYSA): This is generally the best option. HYSAs offer better interest rates than traditional savings accounts, allowing your money to grow (albeit modestly) while remaining liquid. Look for accounts with no monthly fees, easy access, and FDIC insurance.

- Separate Account: Keep your emergency fund separate from your everyday checking account to avoid accidental spending. Out of sight, out of mind often works best for savings.

- Accessibility vs. Friction: You want the money to be accessible in a true emergency (within a day or two), but not so easily accessible that you’re tempted to dip into it for non-emergencies. An HYSA strikes a good balance.

- Avoid Volatile Investments: Do not invest your emergency fund in the stock market or other volatile assets. The primary goal is preservation of capital and liquidity, not growth. You cannot risk your emergency money being down 20% when you suddenly need it.

Step 6: Strategically Manage Debt Alongside Your Fund

The relationship between debt and an emergency fund is nuanced.

- High-Interest Debt First (After a Starter Fund): If you have significant credit card debt with interest rates exceeding 15-20%, it often makes financial sense to build a small starter emergency fund ($1,000-$2,000) and then aggressively tackle that high-interest debt. The interest you save by paying off expensive debt will likely far outweigh the modest interest earned in a savings account.

- Maintain Momentum: Once high-interest debt is cleared, shift your focus back to fully funding your emergency reserve.

- Low-Interest Debt: For low-interest debts like mortgages or student loans, it’s generally advisable to fully fund your emergency account before making extra payments on these. The security of the fund typically outweighs the benefit of slightly accelerating low-interest debt repayment.

Maintaining Momentum: Growing and Replenishing Your Emergency Fund

Building an emergency fund is not a one-time event; it’s an ongoing process. Once you’ve reached your initial target, the work isn’t over. Life changes, and so should your financial safety net.

Regular Reviews and Adjustments

Your financial life is dynamic. Your income might increase or decrease, your essential expenses could change (e.g., a new baby, a different housing situation), or the cost of living might rise. It’s crucial to revisit your emergency fund target at least once a year, or whenever a significant life event occurs, to ensure it still adequately covers your needs. For instance, with inflation, what constituted three months of expenses in 2023 might only cover two and a half months in 2026. Adjust your target accordingly.

Replenishing After Use

The entire purpose of an emergency fund is to be used when a genuine emergency strikes. Do not feel guilty about using it for its intended purpose. However, once you’ve dipped into it, your absolute priority should be to replenish it as quickly as possible. Treat the depleted amount as a new, urgent financial goal. Re-evaluate your budget, temporarily increase your savings contributions, or find additional income sources until your fund is back to its full strength. This ensures you’re always prepared for the next unexpected event.

When to Stop Saving (For the Emergency Fund) and Start Investing

Once you’ve reached your target emergency fund (e.g., 3-6 months of essential expenses), the question often arises: should I keep adding to it, or should I shift my focus? For most people, once the initial target is met, it’s time to redirect excess savings towards other crucial financial goals, specifically investing for long-term growth. This includes contributing to retirement accounts (401k, IRA), saving for a down payment on a home, or investing in a diversified portfolio.

However, some may choose to build a slightly larger “buffer fund” (e.g., 9-12 months) if they have unique circumstances like a highly variable income, a family member with significant health issues, or a very high-cost-of-living area. The goal is to strike a balance: have enough to feel secure, but not so much that you’re losing out on potential investment returns by keeping too much cash idle. Remember, while cash is king for emergencies, inflation slowly erodes its purchasing power over time. Investing allows your money to work harder for you.

Thinking Beyond the Initial Target: Building Generational Wealth

An emergency fund is the foundational layer of financial security. Once firmly established, it frees you to think about loftier goals, such as “How To Build Generational Wealth.”

An emergency fund eliminates the need to derail your long-term investment plans when crises hit. You won’t have to sell stocks at a loss, withdraw from retirement accounts prematurely (and incur penalties), or take on high-interest debt that siphons away future wealth.

By protecting your current assets and preventing financial setbacks, your emergency fund indirectly contributes to your ability to accumulate wealth that can be passed down. It allows you to stay invested through market fluctuations, consistently contribute to retirement accounts, and pursue other wealth-building opportunities without the constant threat of financial disruption. It’s the invisible guardian of your financial legacy, ensuring that short-term problems don’t undermine your long-term vision for prosperity for yourself and future generations.

Common Pitfalls and How to Avoid Them

Even with the best intentions, individuals can stumble on their journey to building and maintaining an emergency fund. Awareness of these common pitfalls can help you navigate around them.

1. Using the Fund for Non-Emergencies

This is arguably the most common mistake. An emergency fund is not a slush fund for sales, vacations, or new gadgets. It’s for genuine, unforeseen financial crises.

- How to Avoid: Clearly define what constitutes an emergency for you and your family. Write it down if necessary. Examples: job loss, major medical issue, essential home/car repair. Examples of non-emergencies: concert tickets, new TV, holiday gifts, a “really good deal” on a non-essential item. Create separate sinking funds for planned expenses like vacations or holiday shopping.

2. Keeping It Too Accessible (or Not Accessible Enough)

Finding the right balance between accessibility and friction is crucial. If it’s too easy to access (e.g., in your primary checking account), you’re more likely to spend it. If it’s too difficult (e.g., locked in a CD with penalties for early withdrawal), it defeats the purpose of being an emergency fund.

- How to Avoid: A high-yield savings account separate from your checking account is ideal. It offers easy, quick transfers (usually within 1-2 business days) when needed, but the slight delay discourages impulsive spending. Avoid investing emergency funds in volatile assets like stocks or real estate, where liquidity and principal preservation are not guaranteed.

3. Allowing Inflation to Erode Purchasing Power

While an emergency fund shouldn’t be in volatile investments, keeping it in a zero-interest checking account means its purchasing power slowly diminishes over time.

- How to Avoid: Opt for a high-yield savings account. While the interest rate may not beat inflation entirely, it helps mitigate some of the erosion. The primary goal is safety and liquidity, not significant growth, but every bit helps. Review your fund’s target regularly, especially in years like 2026, to ensure it still covers your increased cost of living.

4. Procrastination and Overwhelm

The idea of saving several months’ worth of expenses can feel overwhelming, leading to procrastination.

- How to Avoid: Break down your goal into smaller, manageable chunks. Start with a mini-emergency fund ($500-$1,000). Celebrate small milestones. Focus on consistency over speed. Remember, even saving $50 a month is better than saving nothing. Automate your savings to remove the decision-making process.

5. Not Replenishing After Use

Once an emergency fund is used, some people fail to rebuild it, leaving themselves vulnerable to the next crisis.

- How to Avoid: Make replenishing your fund an immediate financial priority. Treat it with the same urgency as you did when initially building it. Adjust your budget, temporarily cut back on discretionary spending, or find extra income until your fund is back to its target level.

6. Lack of Flexibility in the Target Amount

Life circumstances change, but some people stick rigidly to an outdated emergency fund target.

- How to Avoid: Regularly review your financial situation, essential expenses, and risk factors (job stability, dependents, health). Adjust your target fund size as needed. A three-month fund might have been sufficient when you were single, but a year later, with a new mortgage and a child, six months (or more) might be more appropriate.

Beyond the Basics: Integrating Your Emergency Fund into a Holistic Financial Strategy

An emergency fund, while critical on its own, truly shines when viewed as an integral component of a larger, well-structured financial strategy. It’s not just a standalone savings account; it’s the bedrock that supports all other financial aspirations.

The Emergency Fund as a Foundation for Investing

Think of your emergency fund as the sturdy foundation of a house. You wouldn’t build a skyscraper on shaky ground. Similarly, attempting to invest for retirement, a down payment, or other significant goals without an emergency fund is inherently risky. When an unexpected expense arises, you’d be forced to pull money from your investments, potentially selling at a loss during a market downturn, or incurring taxes and penalties on early withdrawals from retirement accounts. This not only sets back your investment timeline but also undermines the power of compounding. By having your emergency fund in place, your investments can remain untouched, allowing them to grow consistently over the long term, regardless of life’s immediate challenges.

Connecting it to Broader Financial Goals

Every major financial goal, from buying a home to funding your children’s education or achieving financial independence, becomes more attainable and less stressful when an emergency fund is present.

- Homeownership: An emergency fund protects your ability to make mortgage payments if income is disrupted, preventing foreclosure. It also covers unexpected home repairs that could otherwise derail your homeownership dreams.

- Retirement: It ensures you won’t have to raid your 401(k) or IRA, preserving those funds for their intended purpose and allowing them to benefit from decades of growth.

- Debt Management: By preventing new debt accumulation during crises, an emergency fund allows you to focus on systematic debt reduction strategies, rather than being constantly pulled back into a cycle of high-interest borrowing.

- Entrepreneurship: For those dreaming of starting a business, a personal emergency fund provides a critical safety net, allowing them to take calculated risks without jeopardizing their entire household’s financial stability.

The Psychological Benefits Extend to Overall Well-being

The impact of an emergency fund goes beyond mere numbers on a spreadsheet. It profoundly affects your mental and emotional well-being. Financial stress is a leading cause of anxiety, relationship strain, and health problems. Knowing you have a substantial financial buffer provides:

- Reduced Stress: The nagging worry about “what if” significantly diminishes. You can sleep better at night.

- Greater Freedom: You’re less beholden to a job you dislike or a situation that’s not ideal because you have the financial runway to seek better opportunities.

- Improved Decision-Making: Without immediate financial pressure, you can make more rational, long-term-oriented decisions about your career, health, and lifestyle.

- Enhanced Resilience: Life will always present challenges. An emergency fund doesn’t prevent them, but it equips you with the financial resilience to bounce back faster and stronger.

In conclusion, building an emergency fund is not just about saving money; it’s about investing in your future self, your peace of mind, and your ability to pursue a life of greater financial freedom and security. It’s the essential first step on the path to financial mastery, making every other financial goal, including achieving significant milestones like “How To Build Generational Wealth,” not just a possibility, but a protected and more secure journey.

Frequently Asked Questions

Recommended Resources

Related reading: How To Write Product Descriptions That Sell (E-ComProfits).

You might also enjoy How To Scale A Small Business Fast from AssetBar.