Simplify Investing: Your Beginner’s Guide to Building a Powerful Three-Fund Portfolio for 2026 and Beyond

Navigating the world of investing can feel like an intimidating journey, especially for beginners. With countless stocks, funds, and strategies vying for your attention, it’s easy to become overwhelmed and fall into analysis paralysis. But what if we told you there’s a proven, elegant, and surprisingly simple strategy that has empowered millions of investors to build substantial long-term wealth?

Welcome to the three-fund portfolio. At Fin3go, we believe in making sophisticated financial concepts accessible, and this strategy is a cornerstone of smart, hands-off investing. This comprehensive guide will demystify the three-fund portfolio, showing you how to construct a robust, diversified, and low-cost investment foundation using just three types of funds. Whether you’re planning for retirement, a down payment, or simply aiming to grow your wealth, understanding this approach in 2026 is an invaluable step towards achieving your financial goals. Get ready to simplify your investing journey and set yourself on a path to financial freedom.

What Exactly is a Three-Fund Portfolio? The Elegant Simplicity

At its core, a three-fund portfolio is a minimalist investment strategy designed to provide broad market exposure, comprehensive diversification, and low maintenance, all while keeping costs to a minimum. It achieves this by using just three types of low-cost, broadly diversified index funds or Exchange Traded Funds (ETFs).

The genius of this approach lies in its simplicity and effectiveness. Instead of trying to pick individual winning stocks or navigate complex sector-specific funds, you invest in funds that collectively own thousands of companies and government bonds, essentially buying “the entire market” – both domestically and globally. This strategy is championed by renowned investors and financial educators for its ability to deliver competitive returns over the long term without requiring constant monitoring or active management.

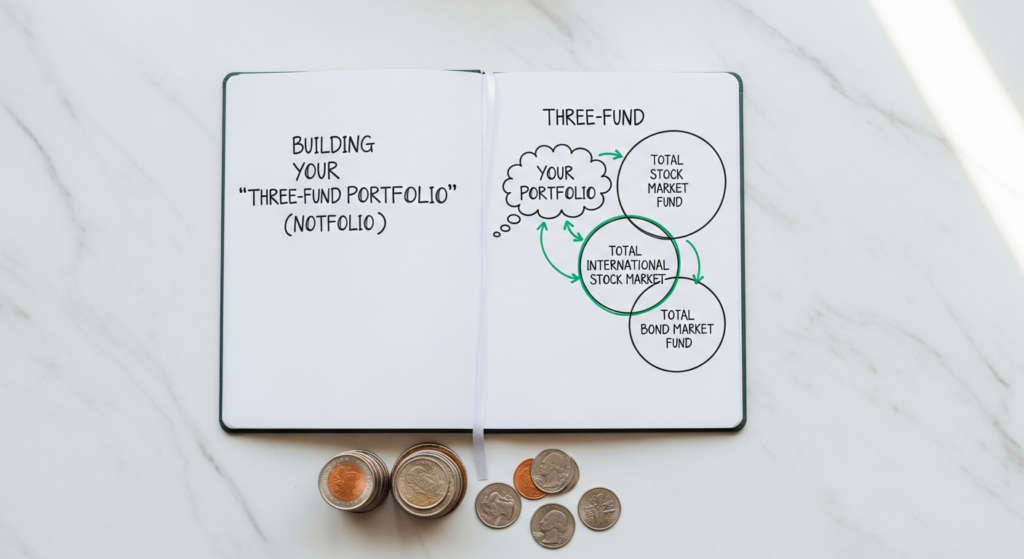

- U.S. Total Stock Market: Capturing the growth potential of the American economy.

- International Total Stock Market: Diversifying globally and tapping into growth from developed and emerging markets worldwide.

- U.S. Total Bond Market: Providing stability, income, and a hedge against stock market volatility.

By combining these three elements, you create a portfolio that is highly diversified across different geographies, company sizes, and asset types, significantly reducing your overall risk while positioning you for consistent growth. As of 2026, the underlying principles of diversification and low-cost indexing remain as vital as ever for successful long-term investing.

The Three Pillars: Understanding Each Core Fund

Let’s dive deeper into each of the three essential components that form the bedrock of this powerful portfolio. Understanding what each fund represents and why it’s crucial will empower you to build your portfolio with confidence.

Pillar 1: Total U.S. Stock Market Index Fund (or ETF)

This fund is your gateway to the robust and dynamic U.S. economy. A total U.S. stock market index fund aims to track the performance of the entire U.S. stock market. This means it holds stocks from virtually every publicly traded company in the United States, weighted by their market capitalization. From tech giants like Apple and Microsoft to established consumer brands, mid-sized companies, and even promising small-cap innovators, you’ll own a piece of it all.

- What it covers: Large-cap, mid-cap, and small-cap U.S. companies. It’s essentially buying a slice of the entire American corporate landscape.

- Why it’s important: Provides broad exposure to the engine of U.S. economic growth. Historically, the U.S. stock market has been a powerful wealth creator. It captures the innovation, productivity, and profitability of American enterprises.

- Example Fund Types: Look for funds with names like “Total Stock Market Index,” “S&P 500 Index” (though Total Stock Market is broader), or “U.S. Equity Market.” Leading providers like Vanguard, Fidelity, and Schwab offer excellent options with incredibly low expense ratios, often under 0.05% as of 2026.

Pillar 2: Total International Stock Market Index Fund (or ETF)

While the U.S. market is strong, limiting your investments solely to your home country introduces “home bias” risk. A total international stock market index fund diversifies your equity holdings by investing in thousands of companies located outside the United States. This includes companies in developed markets (like Europe, Japan, Australia) and often a significant allocation to emerging markets (like China, India, Brazil).

- What it covers: A broad spectrum of companies across various developed and emerging countries worldwide.

- Why it’s important:

- Global Diversification: Different countries and economies perform well at different times. International exposure helps smooth out returns and reduces reliance on any single national market.

- Access to Growth: Some of the fastest-growing economies are outside the U.S., particularly in emerging markets.

- Currency Diversification: While not a direct fund goal, investing internationally can indirectly provide some hedge against fluctuations in the U.S. dollar over the long term.

- Example Fund Types: Search for funds called “Total International Stock Market Index,” “Developed Markets Index,” or “Global Equity ex-U.S.” Expense ratios for these funds are still very competitive, typically in the 0.05% to 0.15% range in 2026.

Pillar 3: Total U.S. Bond Market Index Fund (or ETF)

The third pillar introduces a crucial element of stability and income to your portfolio. A total U.S. bond market index fund invests in a wide variety of investment-grade bonds issued by the U.S. government (Treasuries, agencies) and U.S. corporations. Unlike stocks, which represent ownership in a company, bonds represent a loan to a borrower (the government or a corporation) that pays you interest over a set period.

- What it covers: A diversified basket of U.S. dollar-denominated, investment-grade bonds with varying maturities.

- Why it’s important:

- Stability: Bonds are generally less volatile than stocks, especially during market downturns. They act as a ballast, cushioning your portfolio when stocks decline.

- Income Generation: Bonds provide regular interest payments, offering a consistent stream of income.

- Diversification from Stocks: Bonds often move inversely to stocks, meaning when stocks fall, bonds may rise or hold steady, reducing overall portfolio risk. This correlation is particularly valuable during economic uncertainty.

- Example Fund Types: Look for funds named “Total Bond Market Index,” “U.S. Aggregate Bond Index,” or “Intermediate-Term Bond.” These also boast very low expense ratios, often below 0.10% in 2026.

Crafting Your Allocation: The Right Mix for Your Goals

Once you understand the role of each fund, the next critical step is determining your asset allocation – the percentage you’ll assign to each of the three funds. This is where your personal circumstances, financial goals, risk tolerance, and investment horizon come into play. There’s no one-size-fits-all answer, but understanding the factors involved will help you make an informed decision.

Your asset allocation dictates your portfolio’s overall risk and potential return. A higher percentage in stocks generally means higher potential returns but also higher volatility and risk. A higher percentage in bonds typically means lower potential returns but greater stability and less risk.

Key Factors to Consider:

- Age and Investment Horizon: Generally, younger investors with many years until retirement (a long investment horizon) can afford to take more risk. They might opt for a higher allocation to stocks (e.g., 80-90%). As you get closer to needing your money, you’ll typically want to reduce risk by increasing your bond allocation.

- Risk Tolerance: Be honest with yourself. How would you react if your portfolio dropped by 20-30% in a short period? If you’d panic and sell, a more conservative allocation with more bonds might be better, even if it means potentially lower long-term returns. Behavioral psychology is a huge part of successful investing.

- Financial Goals: Are you saving for a short-term goal (e.g., a down payment in 3-5 years) or a long-term goal (retirement in 20+ years)? Shorter-term goals generally warrant a more conservative approach due to less time to recover from market downturns.

- Income Stability and Emergency Fund: Ensure you have a stable income and a fully funded emergency savings account (3-6 months of living expenses) before investing. This frees you from needing to tap into your investments during market downturns.

Common Asset Allocation Approaches (as a Starting Point for 2026):

- Aggressive (e.g., 80% Stocks / 20% Bonds): Suitable for young investors with a very long time horizon (20+ years) and high risk tolerance. Example: 48% US Stocks, 32% International Stocks, 20% Bonds.

- Moderate (e.g., 70% Stocks / 30% Bonds): A balanced approach for those with a moderately long horizon (10-20 years) and moderate risk tolerance. Example: 42% US Stocks, 28% International Stocks, 30% Bonds.

- Conservative (e.g., 60% Stocks / 40% Bonds): Ideal for those closer to retirement (5-10 years away) or with a lower risk tolerance. Example: 36% US Stocks, 24% International Stocks, 40% Bonds.

- Rule of Thumb: A common guideline is to subtract your age from 110 (or even 120, reflecting increasing lifespans and retirement length in 2026) to determine your approximate stock allocation. For example, a 30-year-old might aim for 80-90% stocks, while a 60-year-old might aim for 50-60%. Remember, this is just a starting point, and your personal risk tolerance is paramount.

When dividing your stock allocation between US and International, a common split is 60/40 or 70/30 in favor of US stocks. However, some investors prefer a 50/50 split for maximum global diversification. The key is to choose an allocation you can stick with through market ups and downs.

Finding Your Funds: Practical Steps for 2026

With your desired asset allocation in mind, the next practical step is to select the specific funds and open an investment account. As of 2026, the landscape for low-cost index funds and ETFs is more accessible than ever before, thanks to competition among major financial institutions.

1. Choose a Reputable Brokerage Firm

Your first decision is where to open your investment account. Look for brokerage firms known for their low costs, wide selection of funds (especially their own low-cost index funds/ETFs), and user-friendly platforms. Top contenders that are well-established in 2026 include:

- Vanguard: Pioneered index investing, known for extremely low expense ratios on its own funds.

- Fidelity: Offers its own suite of zero-expense ratio index funds and a broad selection of third-party ETFs.

- Charles Schwab: Competitive pricing, broad fund selection, and often no commissions on their own ETFs.

- Other Platforms: Depending on your needs, other platforms like M1 Finance (for automated portfolio investing) or robo-advisors like Betterment and Wealthfront (which can automatically manage a diversified portfolio for you) could also be options, though they may involve different fee structures.

Consider whether you’re opening a tax-advantaged account (like a Roth IRA, Traditional IRA, or 401(k) through your employer) or a taxable brokerage account.

2. Selecting the Specific Funds

Once you have your brokerage account, it’s time to choose the actual funds. The goal is to find one fund for each of the three pillars that meets these criteria:

- Index Fund or ETF: These are ideal because they passively track a market index, keeping management fees low.

- Low Expense Ratio (ER): This is paramount. The expense ratio is the annual fee you pay as a percentage of your investment. Even a difference of 0.50% can cost you tens or hundreds of thousands of dollars over decades due to the power of compounding. In 2026, excellent total market index funds often have ERs under 0.10% (e.g., 0.03% to 0.08%).

- Broad Diversification: Ensure the fund truly covers the “total market” for its category (U.S. stocks, international stocks, U.S. bonds). Avoid niche or sector-specific funds for your core portfolio.

Example Fund Search (Generic for 2026, as specific tickers can change):

When searching on your chosen brokerage platform, look for fund names that clearly indicate their broad market coverage:

- For U.S. Total Stock Market:

- “Total Stock Market Index Fund”

- “U.S. Broad Market ETF”

- Examples (for concept, not specific recommendation): VTSAX (Vanguard), FSKAX (Fidelity), SWTSX (Schwab).

- For Total International Stock Market:

- “Total International Stock Index Fund”

- “International Developed & Emerging Markets ETF”

- Examples (for concept): VTIAX (Vanguard), FTIHX (Fidelity), SWISX / SFILX (Schwab).

- For Total U.S. Bond Market:

- “Total Bond Market Index Fund”

- “U.S. Aggregate Bond ETF”

- Examples (for concept): VBTLX (Vanguard), FXNAX (Fidelity), SWAGX (Schwab).

Always double-check the expense ratio and the fund’s investment objective to ensure it aligns with the three-fund philosophy. Many brokerages allow you to buy their own brand of ETFs or index funds commission-free, making them even more attractive.

The Long Game: Managing Your Three-Fund Portfolio

Building your three-fund portfolio is a fantastic achievement, but true wealth creation comes from consistent execution and long-term commitment. The beauty of this strategy is its low maintenance, but “low maintenance” doesn’t mean “no maintenance.” Here’s how to manage your portfolio effectively for decades to come:

1. Automate Your Investments

2. Rebalancing Your Portfolio

Over time, the market performance of your three funds will differ, causing your asset allocation to drift away from your target percentages. For example, if stocks have a stellar year, their portion of your portfolio will grow, making your portfolio riskier than intended. Rebalancing is the process of adjusting your portfolio back to your desired allocation.

- Why Rebalance? It ensures you maintain your intended risk level and, often, involves selling assets that have performed well (selling high) and buying those that have lagged (buying low) – a disciplined approach that can enhance returns over the long run.

- When to Rebalance?

- Time-based: Annually (e.g., every January) is a common and effective frequency.

- Threshold-based: Rebalance when any asset class drifts by a certain percentage from its target (e.g., 5% or 10%). So, if your 60% stock allocation grows to 66%, you’d rebalance.

- How to Rebalance?

- Using New Contributions: The simplest method is to direct new money to the underperforming asset class until your allocation is back in line. This avoids selling and potential tax implications in taxable accounts.

- Selling and Buying: If new contributions aren’t enough, you might sell a portion of your overperforming assets and use the proceeds to buy more of the underperforming assets. Be mindful of capital gains taxes in taxable accounts.

3. Stay the Course and Avoid Market Timing

The biggest enemy of the long-term investor is often emotion. Market downturns are inevitable. When they happen, the urge to sell and “wait until things get better” is strong. Resist it! The three-fund portfolio is designed to weather these storms. Historically, markets have always recovered and reached new highs. Time in the market, not timing the market, is what truly matters.

Focus on your long-term goals, continue your automated investments, and trust the diversified nature of your portfolio. The power of compounding works best when left undisturbed over many decades.

4. Review Periodically (But Don’t Tinker)

While the portfolio itself is set-and-forget, your life isn’t. Every few years, especially after major life events (marriage, children, new job), take a moment to review your financial goals and risk tolerance. Your initial asset allocation might need minor adjustments as you age or if your circumstances significantly change. However, avoid making impulsive changes based on market headlines.

Beyond the Basics: When to Consider Expanding (Briefly)

For most beginners, and indeed for many seasoned investors, the three-fund portfolio is all you’ll ever need. Its elegant simplicity and robust performance make it an incredibly powerful tool. However, as you gain experience and your knowledge grows, you might encounter discussions about expanding beyond these three core funds. For example, some investors consider adding a dedicated small-cap value fund for a potential “value tilt” or looking into real estate investment trusts (REITs) or commodities for further diversification. There are also discussions about investing in specific country funds or adjusting bond durations based on interest rate outlooks.

Our advice at Fin3go for beginners is clear: Master the three-fund portfolio first. Understand its mechanics, live through market cycles with it, and appreciate its benefits. Adding complexity prematurely can lead to over-optimization, higher costs, and often, no better (or even worse) results. The core three-fund approach is designed to capture the vast majority of market returns with minimal effort. Only after you are completely comfortable and have a strong grasp of investment theory should you consider whether adding additional, specific asset classes aligns with your evolving goals and risk profile.

The three-fund portfolio offers a clear, effective, and low-stress path to long-term wealth accumulation. By understanding its components, choosing an allocation that fits your personal circumstances, and committing to consistent contributions and periodic rebalancing, you empower yourself to navigate the financial markets with confidence. It’s a strategy that proves that sometimes, less is truly more when it comes to intelligent investing. Start your journey today, and watch your financial future grow.