How to Negotiate Bank Fees and Get Them Waived: Your Ultimate Fin3go Guide

Few things are as frustrating as seeing unexpected charges erode your hard-earned money. Bank fees – whether they’re for overdrafts, monthly maintenance, or ATM withdrawals – can feel like an inevitable tax on your financial life. Many people simply accept them, believing they have no recourse. However, this couldn’t be further from the truth. With the right approach and a little preparation, you can absolutely learn how to negotiate bank fees and get them waived. This comprehensive guide from Fin3go will empower you with the knowledge and actionable strategies to challenge these charges, save money, and maintain healthier financial habits, a core component of effective personal finance and fintech management. Don’t let your bank hold onto your cash unnecessarily; it’s time to take control of your financial relationship and improve your overall financial health.

Accumulated bank fees can significantly hinder your savings goals, delay debt repayment, and generally impede your financial progress. Understanding how to identify, challenge, and prevent these charges is a crucial skill for anyone serious about optimizing their personal finance. This article will walk you through every step, from understanding common fees to employing advanced negotiation tactics and exploring alternative banking solutions, ensuring you master the art of getting bank fees waived.

What Are Common Bank Fees and What Are You Paying For?

Before you can effectively negotiate a bank fee, you need to understand what you’re being charged for and why. Banks are in the business of making money, and fees are a significant revenue stream. While some fees are legitimate costs for services rendered, others can feel punitive or simply designed to nickel-and-dime customers. A crucial first step in any negotiation is identifying and understanding these common charges.

- Overdraft Fees: These are among the most common and contentious fees. An overdraft occurs when you spend more money than you have in your account. The bank covers the transaction but then charges you a fee, often ranging from $25 to $35 per occurrence. Some banks also charge extended overdraft fees if your account remains negative for several days.

- Monthly Maintenance Fees: Also known as service fees, these are regular charges simply for having an account. While many banks offer “free” checking, these accounts often come with conditions, such as maintaining a minimum daily balance, having direct deposit, or making a certain number of debit card transactions. Fail to meet these conditions, and a monthly fee (e.g., $5-$15) kicks in.

- ATM Fees: You might encounter two types of ATM fees: one from your own bank if you use an out-of-network ATM, and another from the owner of the ATM itself. These can quickly add up, often $2-$5 per transaction.

- Foreign Transaction Fees: When you use your debit or credit card for purchases in a foreign currency or outside your home country, your bank may charge a fee, typically 1% to 3% of the transaction amount.

- Wire Transfer Fees: Sending or receiving money via a wire transfer, especially internationally, can incur significant fees, sometimes $25-$50 per transfer. For international transfers, consider fintech solutions like Wise (formerly TransferWise) or Revolut, which often offer lower fees and better exchange rates than traditional banks, significantly reducing your overall costs.

- Insufficient Funds (NSF) Fees: Similar to overdraft fees, an NSF fee occurs when you attempt a transaction (like writing a check or making an electronic payment) and don’t have enough money in your account, but the bank rejects the transaction rather than covering it. You’re still charged a fee for the attempted transaction.

- Late Payment Fees (for connected products): While technically not a “bank fee” for your checking or savings account, if you have a credit card or loan with the same institution, late payment fees can impact your overall financial relationship and leverage.

- Account Closure Fees: Some banks charge a fee if you close an account shortly after opening it, often within 90 or 180 days.

Understanding why these fees exist is also helpful. Overdrafts, for instance, are often framed as a “service” to prevent your transaction from being declined, though the high fees often overshadow this perceived benefit. Monthly fees help banks cover operational costs and incentivize customers to maintain profitable relationships. By being informed, you shift from a passive recipient of charges to an active participant ready to question and challenge them.

Comparing Fees Across Bank Types: It’s important to note that fee structures can vary significantly between different types of financial institutions. Traditional brick-and-mortar banks often have higher monthly maintenance fees and more stringent requirements for waivers, while online-only banks (neobanks) and credit unions typically pride themselves on offering accounts with no monthly fees, fewer overdraft charges, and sometimes even fee-free international transactions. For example, a traditional bank might charge $10-$15 for monthly maintenance unless you maintain a $1,500 minimum balance, whereas many online banks offer truly free checking with no such requirements. This comparison is crucial when assessing the fairness of the fees you’re being charged and considering alternatives.

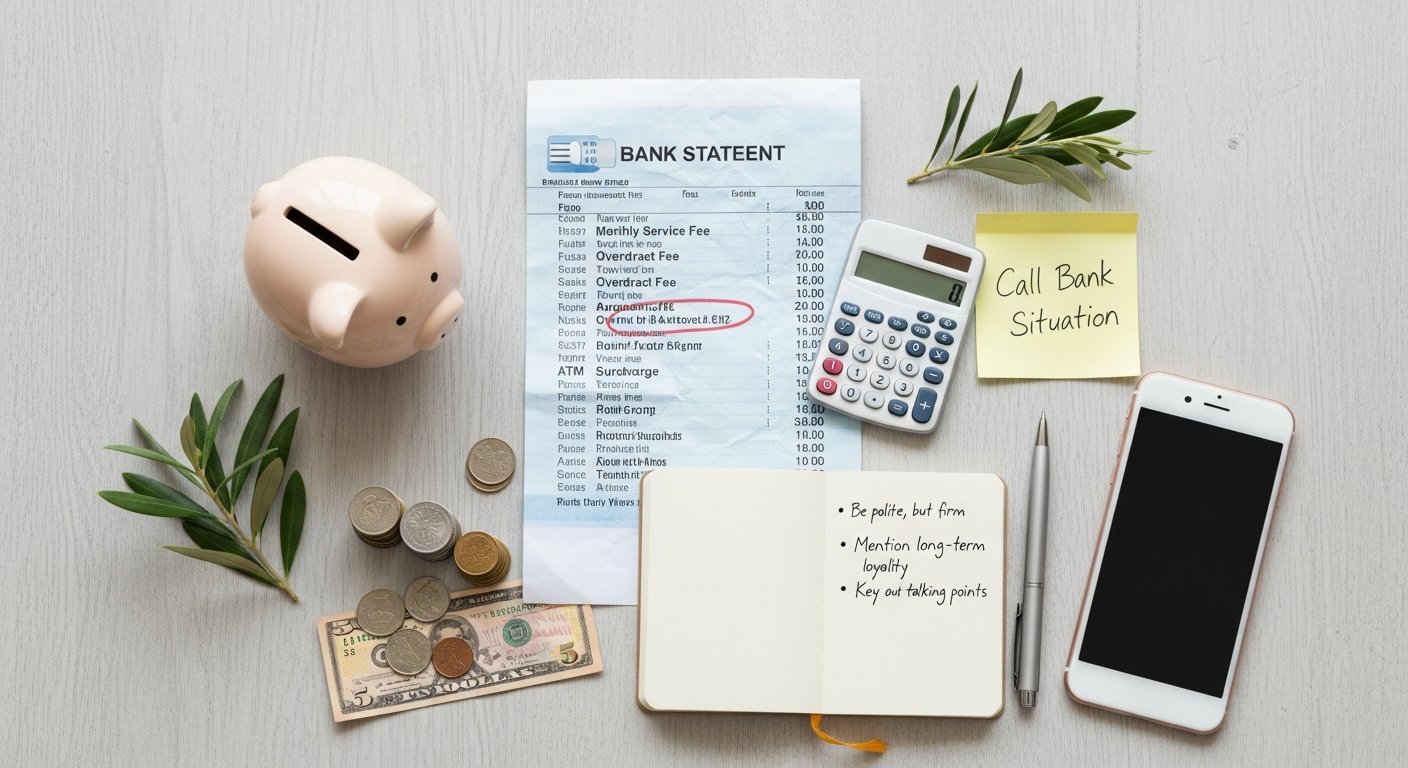

Practical Step: Review Your Bank Statements Religiously. Make it a habit to check your bank statements and online transaction history regularly. Many people only glance at their balance, missing the detailed breakdown of fees. Identify recurring fees or one-off charges that seem out of place. This proactive approach is the first and most critical step in learning how to negotiate bank fees and get them waived effectively.

How to Prepare Your Case Before You Call to Negotiate Bank Fees?

Approaching your bank without preparation is like walking into a courtroom without a lawyer. To maximize your chances of success when you want to negotiate bank fees, you need to arm yourself with information and a clear strategy. This preparation phase is crucial for building a strong argument and demonstrating that you are a valued customer worth keeping.

Here’s how to prepare your arsenal:

- Know Your Account History and Relationship Value: Banks value long-term, profitable customers. Before you call, assess your relationship with the bank:

- Account Tenure: How long have you been a customer? Longer tenure usually translates to more goodwill.

- Average Balance: Do you typically maintain a healthy balance in your accounts?

- Direct Deposits: Do you have regular direct deposits of your salary or other income?

- Other Products: Do you have other accounts or products with the same bank (e.g., savings, credit cards, mortgage, auto loans)? Bundling services often makes you a more valuable customer.

- Fee History: Is this your first fee, or do you rarely incur fees? A clean record shows responsible financial behavior. If you have been charged fees before and had them waived, make a note of it.

Real-World Example: A customer who has held a checking account for 15 years, maintains an average balance of $5,000, and also has a mortgage and credit card with the bank has significantly more leverage than someone who opened an account last month with a minimal balance.

- Research the Specific Fee: Understand precisely what fee you were charged, the date it occurred, and the amount. If it was an overdraft, identify the transaction that caused it. Was it a small purchase that pushed you over, or a larger bill? This precision demonstrates you’ve done your homework.

- Review Your Bank’s Fee Schedule and Policies: Most banks publish their fee schedules online. Look for any conditions under which the fee might be waived automatically. Sometimes, fees are waived if you meet certain criteria (e.g., a minimum number of debit card transactions, a specific direct deposit amount, or enrollment in e-statements). Knowing these can help you argue that you almost met a condition, or to ask what you can do to avoid future fees.

- Gather Any Relevant Documentation: While usually not strictly necessary for a phone call, having your bank statements handy can be useful for referencing transaction dates or account numbers. If the fee was due to an error on the bank’s part (rare, but possible), have proof ready.

- Define Your Goal: What do you want to achieve from this interaction? A full waiver? A partial refund? A reversal of the fee as a one-time courtesy? Understanding your desired outcome will help you steer the conversation. Be prepared for less than a full waiver; a partial refund is better than nothing.

By meticulously gathering this information, you transform yourself from a hopeful supplicant into an informed customer advocating for fair treatment. This preparation instills confidence and provides you with the ammunition to build a compelling case.

Actionable Tip: Create a “Banking Relationship” Cheat Sheet. Before you call, jot down key points: how long you’ve been with them, your average balance, other products you have, and your clean fee history. This brief summary will be invaluable during your conversation when you aim to negotiate bank fees.

How Can You Communicate Effectively with Your Bank to Negotiate Fees?

Once you’ve done your homework, the next crucial step is the actual communication with your bank. This is where the “negotiation” truly happens. Your demeanor, clarity, and persistence can make all the difference in successfully getting a fee waived. Remember, you’re interacting with a person, often a customer service representative, who has specific guidelines but also some discretion.

Here’s how to navigate the conversation:

- Choose the Right Channel: Phone is Usually Best.

- Phone Call: This is generally the most effective method. It allows for real-time dialogue, clarifies misunderstandings, and lets you build a rapport with the representative. You can also convey nuance in your tone.

- In-Person Visit (Branch): For complex issues or if you prefer face-to-face interaction, visiting a branch can be effective. This can be particularly useful if you have a long-standing relationship with specific branch staff.

- Online Chat or Secure Message: While convenient, these methods lack the personal touch and can sometimes lead to canned responses. Use them for simple inquiries or if phone calls are not feasible.

- Be Polite, Professional, and Empathetic: This cannot be stressed enough. Customer service representatives deal with frustrated people all day. Starting the conversation calmly and courteously sets a positive tone. Begin by politely explaining your situation.

- “Hello, my name is [Your Name], and I’m calling about a fee on my account.”

- “I understand you’re just doing your job, and I appreciate your help with this.”

A pleasant demeanor significantly increases the likelihood that the representative will go the extra mile for you.

- State Your Case Clearly and Concisely: After the initial pleasantries, clearly explain:

- The specific fee: “I noticed a $35 overdraft fee on [Date] for transaction [Transaction Details].”

- Your understanding of what happened: “It appears I had an unexpected expense that caused my balance to dip briefly.” (If it was a genuine mistake on your part.)

- Your request: “I’m hoping you could consider waiving this fee as a one-time courtesy.”

Avoid rambling or getting emotional. Stick to the facts you gathered during your preparation.

- Highlight Your Value as a Customer: This is where your preparation pays off. Subtly (or not so subtly) weave in details about your relationship with the bank.

- “I’ve been a loyal customer with [Bank Name] for [Number] years, and I usually maintain a healthy balance.”

- “I also have my direct deposit and a [Credit Card/Loan] with you.”

- “This is my first time incurring such a fee, and I’m generally very careful with my finances.”

This reminds the bank that you’re not just another account number, but a valuable asset they want to retain.

- Be Prepared to Negotiate and Compromise: Sometimes a full waiver isn’t possible, but a partial refund or a future credit might be. If the representative says they can’t waive the full amount, politely ask:

- “I understand. Is there any possibility of a partial refund?”

- “Could you perhaps offer a credit to my account for a portion of the fee?”

- “What can I do on my end to ensure this doesn’t happen again, and are there any financial literacy programs I can enroll in to prevent future fees?”

- Know When to Escalate (Politely): If the first representative insists they cannot help, and you believe your case is strong, it’s okay to ask to speak to a supervisor or manager. Do so politely:

- “I appreciate your time, but I’m still hoping for a resolution on this. Would it be possible to speak with a supervisor who might have more flexibility?”

Supervisors often have greater authority to issue waivers.

- Note Down Details: Always write down the name of the representative you spoke with, the date and time of the call, and the outcome. If the fee is waived, confirm when you can expect to see the change reflected in your account. This record is invaluable if you need to follow up.

Real-World Example: “Hi, my name is Sarah, and I’m calling about a $35 overdraft fee on my checking account from May 15th. I’ve been a customer with [Bank Name] for eight years, and this is the first time I’ve ever had an overdraft. I usually have my direct deposit come into this account and maintain a good balance. I’m usually very diligent with my finances, and I was hoping you might be able to waive this fee as a one-time courtesy.”

What Are Advanced Strategies to Negotiate Bank Fees and Prevent Future Charges?

Beyond the basics of polite communication and highlighting your customer value, there are several advanced tactics you can employ to increase your success rate when you negotiate bank fees. Moreover, the best negotiation is often prevention, so understanding how to proactively avoid future fees is key to long-term financial health.

Advanced Negotiation Tactics to Get Bank Fees Waived:

- The “Goodwill Gesture” Ask: Frame your request not as a demand, but as an appeal for a goodwill gesture. This subtly acknowledges the bank’s discretion and positions you as a reasonable, valued customer. “Given my long history with the bank, I was hoping you could extend a goodwill waiver for this particular fee.” This works especially well for first-time offenders or rare occurrences.

- Leverage Competition (Carefully): If you’re consistently running into fees that could be avoided elsewhere, you can (politely) mention competitor offers. This is particularly effective for recurring fees like monthly maintenance. “I’ve noticed that [Competitor Bank] offers a similar checking account with no monthly fees. I truly value my relationship here, but these fees are becoming a concern. Is there anything you can do to help me avoid them, perhaps by moving me to a different account type or waiving it based on my direct deposit?” This shows you’re considering alternatives, which can incentivize the bank to retain your business.

- Offer a Compromise: If a full waiver seems out of reach, don’t give up. Propose a middle ground. “If a full waiver isn’t possible, would it be feasible to offer a 50% refund, or credit my account with half the fee amount?” Any amount saved is a win.

- Ask for a Specific Program or Solution: Instead of just asking for a waiver, ask what the bank can do to help you prevent future fees. “Are there any financial literacy programs, alerts, or account linking options that could help me avoid this in the future?” This shows initiative and a desire for a long-term solution, which can make a representative more willing to help.

- Understanding Fee Waiver Triggers: Some fees have built-in waiver conditions. For example, many banks waive monthly maintenance fees if you:

- Maintain a minimum daily balance (e.g., $1,500).

- Have a certain amount of direct deposits each month (e.g., $500).

- Are enrolled in specific services (e.g., e-statements, online banking).

- Are under a certain age (student accounts) or over a certain age (senior accounts).

- Have other bundled products with the bank.

Knowing these criteria allows you to ask for a waiver based on meeting (or almost meeting) these conditions, or to adjust your banking habits to meet them going forward.

Proactive Strategies for Preventing Future Fees:

The best way to negotiate fees is to avoid them entirely. Implement these strategies to maintain control over your finances:

- Set Up Account Alerts: Most banks offer free email or text alerts for various account activities:

- Low Balance Alerts: Get notified when your balance drops below a set threshold, giving you time to transfer funds or adjust spending.

- Large Transaction Alerts: Be notified of any transaction over a certain amount, helping you spot potential fraud or unexpected deductions.

- Overdraft Alerts: Some banks will notify you before an overdraft officially processes, giving you a small window to deposit funds.

- Link Accounts for Overdraft Protection: Connect your checking account to a savings account or a line of credit. If you overdraw your checking, funds are automatically transferred to cover the transaction, often for a smaller transfer fee rather than a large overdraft fee. Ensure you understand the terms, as some lines of credit may charge interest.

- Review and Optimize Your Account Type: Are you in the right account? If you consistently struggle to meet minimum balance requirements for a “free” checking account, consider:

- A truly free checking account from an online bank or credit union.

- A basic checking account with lower (or no) monthly fees, even if it has fewer perks.

Specific Data Point: Many challenger banks and credit unions pride themselves on offering checking accounts with no monthly maintenance fees, no minimum balance requirements, and often no foreign transaction fees, making them attractive alternatives for fee-conscious consumers.

- Maintain Minimum Balances: If your account has a minimum balance requirement to waive fees, make it a priority to keep your balance above that threshold.

- Use In-Network ATMs: Stick to your bank’s ATMs or those in their partner networks to avoid surcharges. Many banks have apps that help you locate nearby fee-free ATMs.

- Monitor Your Automatic Payments: Ensure you have sufficient funds before recurring bills are deducted. Set reminders a day or two before large payments are due.

- Opt-Out of Overdraft “Protection”: Under federal law, banks must ask for your permission to process ATM and one-time debit card transactions that would overdraw your account. If you opt-out, these transactions will simply be declined, saving you the overdraft fee. Be aware this means your card might be declined at checkout, which can be inconvenient.

By combining assertive negotiation tactics with robust preventative measures, you empower yourself to significantly reduce, and often eliminate, bank fees from your financial life. This proactive approach is a cornerstone of smart personal finance management.

Actionable Tip: Schedule a “Fee Audit” Annually. Once a year, review all your accounts and their associated fees. Compare them to other offerings in the market. This ensures you’re always getting the best value for your banking relationship.

When Should You Consider Alternative Banking Solutions Beyond Negotiation?

While mastering how to negotiate bank fees is a powerful skill, there comes a point when persistent fees, despite your best efforts, signal a deeper issue with your current banking relationship. If you find yourself constantly battling fees, or if your bank is unwilling to work with you, it might be time to explore alternative banking solutions. The financial landscape has evolved dramatically, offering more choices than ever before.

Assessing Your Current Bank Relationship:

Before making a change, honestly evaluate your current situation:

- Frequency of Fees: Are you incurring fees regularly, even after implementing prevention strategies?

- Bank’s Responsiveness: How receptive is your bank to your fee waiver requests? Do they consistently refuse, or only offer limited flexibility?

- Account Type Suitability: Is your current account type truly the best fit for your spending habits, income patterns, and balance management?

- Overall Value: Beyond fees, are you getting good value from your bank (e.g., competitive interest rates, excellent customer service, user-friendly digital tools, access to loans)?

If the answers lean towards a negative experience, it’s a clear indicator that your bank may no longer be serving your best financial interests.

Exploring Alternative Banking Options:

The good news is that you have a wide array of choices beyond traditional brick-and-mortar banks:

- Fintech & Neobanks (Online-Only Banks): These digital-first institutions are often built on a model of lower overhead, which translates into fewer fees for customers.

- Pros: Frequently offer no monthly maintenance fees, no overdraft fees (or very low ones), no foreign transaction fees, competitive interest rates on savings, and robust mobile apps with advanced budgeting and alert features. Examples include Chime, Ally Bank, SoFi Money, and Varo.

- Cons: Limited or no physical branch access, which can be an issue for cash deposits or complex in-person services.

Real-World Example: Many online banks offer interest-bearing checking accounts with no monthly fees and reimburse ATM fees, a stark contrast to traditional banks that might charge $10-$15 monthly for basic checking unless strict conditions are met.

- Credit Unions: Member-owned, non-profit financial institutions.

- Pros: Generally known for lower fees, better interest rates on savings, and more personalized customer service compared to large commercial banks. Their focus is on member benefit, not shareholder profit.

- Cons: May have fewer branches and ATMs, and their technology might not always be as cutting-edge as fintechs (though many are catching up). Membership requirements can apply (e.g., living in a certain area, belonging to an affiliated organization).

- Different Account Types at Your Current Bank: Sometimes, you don’t need to switch banks entirely. Your current institution might offer other account types that better suit your needs. For instance, a basic checking account might have fewer perks but also fewer fees than a premium account you might have been upsold on. Inquire about student accounts, senior accounts, or accounts designed for lower transaction volumes if applicable.

The Switching Process: Making a Smooth Transition

Switching banks might seem daunting, but it can be a straightforward process with careful planning:

- Open a New Account First: Do not close your old account until your new one is fully set up and operational.

- Update Direct Deposits: Change your payroll, government benefits, or other regular incoming payments to your new account.

- Update Automatic Payments and Subscriptions: List all recurring bills (utilities, streaming services, loan payments, insurance) and update them with your new account information. This is crucial to avoid late fees or service interruptions.

- Transfer Funds: Once all direct deposits and automatic payments are re-routed, transfer the remaining balance from your old account to your new one. Keep a small buffer in the old account for a few weeks to catch any missed payments.

- Close the Old Account: After confirming all transactions have cleared and no new activity is occurring, formally close your old account. Request a confirmation in writing. Be mindful of any account closure fees if you close it too soon after opening.

By taking a proactive approach to your banking relationship – first by learning how to negotiate bank fees and get them waived, and then by exploring alternatives if negotiation consistently fails – you ensure that your financial services align with your best interests. This commitment to optimizing your banking choices is a powerful step towards greater financial freedom and less money wasted on avoidable fees.

Actionable Tip: Create a “Switching Checklist.” List all your direct deposits and automatic payments. Check them off one by one as you update them with your new bank details. This methodical approach will prevent missed payments and ensure a smooth transition.

Conclusion

Bank fees, while often presented as an unavoidable aspect of financial services, are not set in stone. This guide has equipped you with the comprehensive knowledge and actionable strategies necessary to understand, challenge, and ultimately waive many of these charges. From meticulously reviewing your statements and preparing a strong case based on your value as a customer, to employing polite yet firm communication techniques, you now know precisely how to negotiate bank fees and get them waived effectively.

Remember, the power to save hundreds, even thousands, of dollars over your lifetime lies in being informed, proactive, and persistent. Don’t be a passive recipient of fees; be an active participant in your financial well-being. By understanding the types of fees, preparing your negotiation strategy, communicating professionally, and implementing preventative measures like account alerts and linking accounts, you can significantly reduce your financial outflows to your bank, thereby improving your overall financial health and progress towards your savings goals.

And if, despite your best efforts, your current banking relationship proves to be a consistent source of frustration and fees, remember that you have options. The modern financial landscape, rich with fintech innovators and community-focused credit unions, offers a plethora of alternatives designed to be more customer-friendly and fee-transparent. Empower yourself to make a change that truly benefits your bottom line and aligns with your personal finance management goals.

Don’t just accept bank fees – empower yourself to challenge them. Start negotiating today and reclaim your financial power. Your wallet will thank you.

Frequently Asked Questions About Negotiating Bank Fees

Can I negotiate any type of bank fee?▾

How often can I ask for a fee waiver?▾

What if I’m a new customer? Do I still have leverage?▾

Is it better to call or visit a branch to negotiate?▾

What if my bank refuses to waive the fee?▾