Understanding Your Current Financial Landscape: The Bedrock of Savings

Before you can begin to negotiate or cut expenses, you must first understand exactly where your money is going. This foundational step is often overlooked but is arguably the most crucial. Without a clear picture of your income and outflows, efforts to save or negotiate will be akin to sailing without a compass – directionless and inefficient. This is precisely where the discipline of budgeting comes into play, serving as your essential financial roadmap.

The Imperative of a Monthly Budget

Creating a monthly budget isn’t just about restricting spending; it’s about gaining control, making informed decisions, and aligning your financial actions with your long-term aspirations. If you’re wondering How To Create A Monthly Budget, the process begins with a simple yet powerful exercise: documenting every dollar that enters and leaves your bank account. This isn’t a one-time task; it’s an ongoing practice that evolves with your life and financial situation.

- Track Your Income: Start by tallying all your sources of income for the month. This includes salaries, freelance payments, rental income, and any other regular inflows.

- Categorize Your Expenses: This is where the real insights emerge. Divide your expenses into distinct categories. Common categories include:

- Fixed Expenses: These are costs that largely stay the same each month, such as rent/mortgage, loan payments, insurance premiums, and subscriptions.

- Variable Expenses: These fluctuate from month to month and offer the most flexibility for reduction. Examples include groceries, dining out, entertainment, transportation, and utilities.

- Discretionary Spending: Often lumped with variable, but specifically refers to non-essential items or activities like hobbies, impulse purchases, or luxury goods.

- Analyze and Adjust: Once you have a clear picture, analyze where your money is going. Are you spending more on dining out than you realized? Is a particular subscription service going unused? This analysis reveals areas ripe for negotiation or reduction. Many find the 50/30/20 rule helpful: 50% of income for needs, 30% for wants, and 20% for savings and debt repayment. While a guideline, it provides a solid framework.

Utilize Fin3go’s resources or popular budgeting apps to streamline this process. Many fintech solutions can automatically categorize your transactions, providing real-time insights into your spending habits. This granular view empowers you to pinpoint exactly which bills are taking the largest bite out of your income and which expenses are merely draining your funds without providing significant value. Understanding your financial landscape is the first, indispensable step towards effective negotiation and sustainable expense reduction.

The Psychology of Negotiation: Why It Works and How to Embrace It

For many, the thought of negotiating a bill can evoke feelings of anxiety or discomfort. We’ve been conditioned to accept prices as they are presented, often viewing bills as non-negotiable decrees. However, this mindset is a significant barrier to financial savings. The truth is, many companies, particularly those in competitive industries, anticipate and even welcome negotiation. It’s a fundamental aspect of commerce, and understanding the psychology behind it can transform your approach to managing expenses.

Shifting Your Perspective: From Aversion to Empowerment

The primary reason negotiation works is simple: companies want to retain your business. Acquiring new customers is often far more expensive than keeping existing ones satisfied. When you express a desire to leave or question your current rates, you’re not being confrontational; you’re simply exercising your consumer power. Companies would rather offer you a discount or an improved plan than lose you to a competitor.

- It’s Expected: Many businesses have retention departments specifically trained to negotiate. They have a playbook for offering discounts, upgrades, or special deals to keep customers happy. They expect you to call.

- You Have Leverage: Your loyalty, your payment history, and the competitive market itself are all forms of leverage. Researching competitor prices gives you tangible points to discuss.

- It’s a Win-Win: A successful negotiation means you save money, and the company retains a paying customer. It’s not about one party “winning” over the other, but finding a mutually beneficial arrangement.

- Confidence is Key: Approach the conversation with politeness, firmness, and confidence. You are a valuable customer, and you have every right to seek fair pricing for the services you receive.

Overcoming the initial apprehension is crucial. Start with smaller negotiations, perhaps a subscription you no longer fully utilize, and build your confidence. Remember, the worst they can say is no, and even then, you’re no worse off than when you started. By embracing the mindset that negotiation is a standard, acceptable part of consumer interaction, you unlock a powerful tool for financial optimization.

Identifying Negotiable Bills and Expenses: Your Target List for Savings

Prime Candidates for Negotiation

Armed with your budget, begin to compile a list of expenses where you believe there’s room for improvement. Here are the most common and often successful areas:

- Internet, Cable, and Phone Services: This is arguably the easiest category for negotiation. The telecommunications industry is fiercely competitive.

- Strategy: Research competitor offers in your area. Bundle services if advantageous. Call the “retention” or “cancellations” department, not general customer service. Mention you’re considering switching providers due to price.

- Insurance Premiums (Auto, Home, Health, Life): Insurance companies frequently adjust rates, and loyalty doesn’t always pay.

- Strategy: Shop around annually. Get quotes from multiple providers. Ask your current insurer for a “loyalty discount” or to review your policy for potential savings (e.g., higher deductibles, bundling policies). Inquire about discounts for good driving, home security systems, or payment in full.

- Credit Card Interest Rates: High interest rates on credit card debt can quickly erode your financial progress.

- Strategy: If you have a good payment history, call your credit card company and ask for a lower interest rate. Explain you’re a loyal customer and are looking to manage your debt more effectively. Be prepared to mention you’re considering balance transfers to other cards with lower rates. This is a critical step in managing debt, whether you eventually choose the Snowball Vs Avalanche Debt Payoff Method.

- Medical Bills: Often overlooked, medical bills are surprisingly negotiable, especially for out-of-pocket expenses.

- Strategy: Review bills for errors. Ask for an itemized bill. Negotiate a discount for paying in cash or paying the full balance upfront. Inquire about payment plans. Hospitals often have charity care programs or financial assistance for those who qualify.

- Bank Fees (Monthly Maintenance, Overdraft): While some banks have eliminated these, others still charge them.

- Strategy: Call your bank and politely ask for a waiver, especially if it’s your first time or you have a good account history. Consider switching to a bank or credit union that offers fee-free accounts.

- Subscriptions and Memberships: Gyms, streaming services, software, magazines – these can add up.

- Strategy: Evaluate usage. Can you get by with a cheaper tier? Can you share family plans? If you’re a long-term member, ask for a discount or a loyalty rate. Many services offer annual discounts if you pay upfront.

- Rent: While often challenging, in certain markets or situations, rent can be negotiable.

- Strategy: If you’re a good, long-term tenant, your landlord might be open to negotiating a renewal rate, especially if the market is soft or they want to avoid the cost and hassle of finding a new tenant. Offer to sign a longer lease for a slightly lower rate increase.

By systematically identifying these categories and prioritizing those with the highest financial impact, you can create a targeted negotiation plan that yields tangible savings. Remember, every dollar saved is a dollar earned, moving you closer to your financial objectives.

Strategies for Successful Negotiation: Your Playbook for Savings

Negotiation isn’t just about asking for a lower price; it’s a strategic process that requires preparation, confidence, and a clear understanding of your goals. With the right techniques, you can significantly increase your chances of success across various bill categories. Here’s your Fin3go playbook for effective negotiation in 2026.

Step-by-Step Negotiation Tactics

Approach each negotiation as a mini-project. The more prepared you are, the more confident and successful you’ll be.

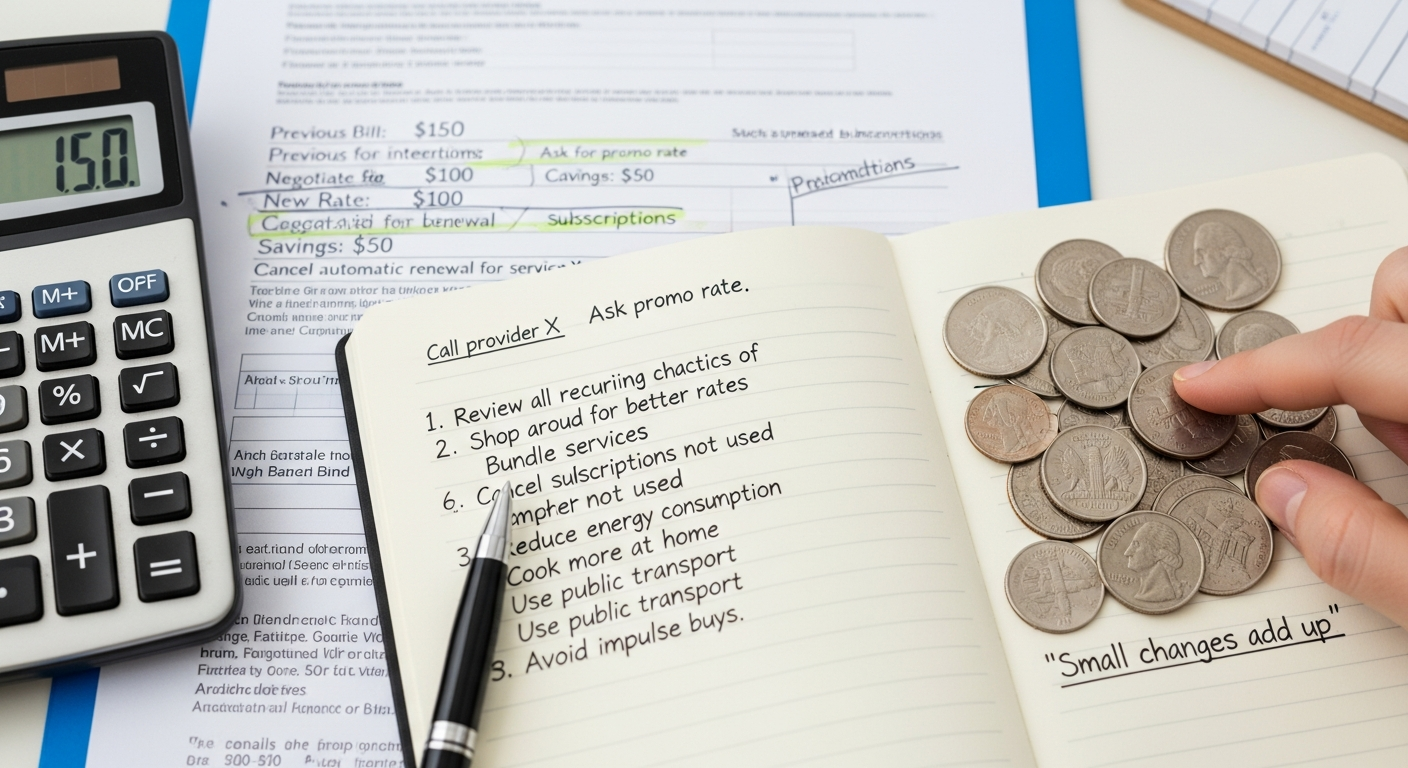

- Do Your Homework: Research is Power.

- Gather Current Information: Have your most recent bill handy. Know your current rates, contract end dates, and any applicable penalties for early termination.

- Competitor Analysis: Research what competitors are offering for similar services in your area. Look for introductory rates, bundles, and special promotions. This is your strongest leverage.

- Your Usage History: If you’re negotiating internet or phone, know your average data usage. If you’re barely using your high-tier plan, you have a strong case for downgrading.

- Your Value as a Customer: Note your payment history. Are you a long-term, on-time payer? This is valuable to them.

- Choose the Right Time and Channel:

- Timing: The best time to negotiate is often just before your contract expires or when a promotional rate is about to end. Another good time is when you receive an unexpected rate increase.

- Channel: For most services, a phone call is best, allowing for real-time dialogue and back-and-forth. Ask to speak to the “retention” or “cancellations” department, as these agents have more authority to offer discounts. For medical bills, a direct call to the billing department is ideal.

- Master the Script: Be Polite, Firm, and Clear.

- Start with a Positive Tone: Begin politely. “Hello, I’m calling because I’ve been a loyal customer for X years, and I really value your service, but I’m concerned about my current bill.”

- State Your Goal Clearly: “I’m looking to lower my monthly payment for [service] because [reason – e.g., competitor X is offering a better rate, my budget is tight, I’m not utilizing the full service].”

- Present Your Research: “I’ve seen that [Competitor Name] is offering [specific plan/rate] for [X amount], and I was hoping you could match or beat that.”

- Be Patient and Listen: The representative might offer an initial small discount. If it’s not enough, politely reiterate your request. Listen to their counter-offers and reasoning.

- Don’t Be Afraid of Silence: Sometimes, a polite silence after stating your case can prompt the representative to find a better offer.

- Ask for Alternatives: If a direct discount isn’t possible, ask about other ways to save: bundling options, downgrading services, temporary promotions, or waiving fees.

- Be Prepared to Escalate (Politely): If the first representative can’t help, politely ask to speak with a supervisor. They often have more leeway.

- Be Prepared to Walk Away (The Ultimate Leverage): If you’ve exhausted all options and aren’t satisfied, state that you’re considering cancelling your service. Often, this triggers the best offers from retention departments. Only use this if you’re genuinely prepared to switch providers.

- Document Everything:

- Note the date, time, and name of the representative you spoke with.

- Record the details of any new agreement, including the new price, terms, and how long it lasts. Ask for a confirmation email. This documentation is crucial if there are any discrepancies later.

By following these strategies, you transform a potentially daunting task into an empowering financial action. Each successful negotiation not only saves you money but also builds your confidence for future financial interactions.

Beyond Negotiation: Long-Term Expense Reduction and Wealth Building

While negotiating bills offers immediate relief and significant savings, a truly robust financial strategy extends beyond one-off conversations. Long-term expense reduction involves a holistic approach to your spending habits, debt management, and future investments. The goal isn’t just to save a few dollars now, but to cultivate habits that lead to lasting financial freedom and the ability to How To Build Generational Wealth.

Cultivating Sustainable Savings Habits

- Automate Your Savings: The easiest way to save is to make it automatic. Set up automatic transfers from your checking to your savings or investment accounts immediately after payday. This ensures you pay yourself first and reduces the temptation to spend.

- Strategic Debt Management: Lowering expenses often frees up capital. Direct this freed-up money towards high-interest debt. Understanding the Snowball Vs Avalanche Debt Payoff Method is crucial here.

- Debt Snowball: Focus on paying off the smallest debt first, regardless of interest rate. The psychological wins of clearing debts quickly can be highly motivating.

- Debt Avalanche: Prioritize debts with the highest interest rates first. This method saves you the most money on interest over time.

Choose the method that best aligns with your personality and financial discipline, but commit to eliminating high-interest debt, as it’s one of the biggest drains on your finances.

- Refinance Major Debts: For larger obligations like mortgages, student loans, or auto loans, explore refinancing options. Lowering your interest rate or extending your term (if financially sound) can significantly reduce monthly payments or total interest paid over the life of the loan.

- Mindful Consumption and Lifestyle Inflation: Be conscious of lifestyle creep – where increased income leads to increased spending. Before making a significant purchase, ask yourself if it aligns with your values and long-term financial goals. Can you differentiate between needs and wants?

- Energy Efficiency and Home Improvements: Invest in energy-efficient appliances, seal drafts, or install smart thermostats. These upfront costs can lead to substantial, long-term savings on utility bills.

- Meal Planning and Smart Grocery Shopping: Food is a significant variable expense. Plan your meals, buy in bulk when appropriate, stick to a shopping list, and avoid impulse purchases to drastically cut down on grocery costs.

Connecting Savings to Wealth Building

Every dollar saved and every expense reduced is a dollar that can be invested. This is the direct link to building substantial wealth, including generational wealth. By consistently lowering your expenses, you create a surplus that can be directed towards:

- Investment Accounts: Fund your 401(k), IRA, or other brokerage accounts. The power of compounding interest means that even small, consistent investments can grow into significant sums over time.

- Emergency Fund: Build a robust emergency fund (3-6 months of living expenses) to prevent future debt in case of unforeseen circumstances.

- Education Funds: Save for your children’s or your own future education.

- Real Estate: Save for a down payment on a home or investment property.

The journey to How To Build Generational Wealth begins with disciplined financial habits, smart expense management, and strategic investing. By integrating negotiation into a broader strategy of long-term expense reduction and wealth accumulation, you set a powerful precedent for your financial future and that of your descendants in 2026 and beyond.

Leveraging Technology for Financial Optimization: The Fin3go Advantage

In the digital age, personal finance is no longer solely about spreadsheets and manual calculations. Fintech (financial technology) has revolutionized how we manage our money, offering powerful tools that can automate savings, track spending, and even negotiate on your behalf. At Fin3go, we believe in harnessing these innovations to simplify your financial life and amplify your savings.

Fintech Tools for Smart Expense Management

Embracing technology can significantly streamline the process of understanding, reducing, and negotiating your expenses.

- Budgeting and Expense Tracking Apps: Apps like Mint, YNAB (You Need A Budget), or Personal Capital connect directly to your bank accounts and credit cards, automatically categorizing your transactions. This provides real-time insights into your spending patterns, making it easier to identify areas for reduction. They can even send alerts when you’re approaching budget limits.

- Automated Bill Negotiation Services: Yes, there are services designed to negotiate bills for you! Companies like Trim, Billshark, or Truebill specialize in contacting your service providers (internet, cable, phone) on your behalf to find lower rates or cancel unwanted subscriptions. They often work on a commission basis, taking a percentage of the savings they achieve for you. This is an excellent option if you’re time-strapped or uncomfortable with direct negotiation.

- Comparison Websites and Apps: Before signing up for new services or renewing old ones, use comparison websites for insurance (e.g., Policygenius, The Zebra), utilities (in deregulated markets), or credit cards. These platforms quickly show you the best rates available, providing invaluable leverage for your negotiations.

- Subscription Management Tools: Many budgeting apps now include features to track and manage all your subscriptions in one place, alerting you to forgotten or unused services. This helps prevent “subscription creep,” a common drain on finances.

- AI-Powered Financial Advisors: While not directly negotiating bills, AI-driven platforms can analyze your entire financial picture, offer personalized advice on budgeting, investing, and debt management, and help you identify areas where you can optimize your spending to meet your financial goals for 2026 and beyond. This proactive advice can guide your negotiation strategies.

- Digital Banking and High-Yield Savings Accounts: Modern digital banks often offer higher interest rates on savings, lower fees, and intuitive mobile apps that make managing your money easier. Moving your savings to a high-yield account ensures your money is working harder for you.

The integration of fintech into your financial strategy isn’t just about convenience; it’s about gaining a competitive edge. These tools provide data, automation, and expert assistance that can significantly enhance your ability to lower expenses, manage debt effectively (whether using the Snowball Vs Avalanche Debt Payoff Method or another strategy), and ultimately accelerate your journey towards building generational wealth. Embrace the Fin3go advantage by leveraging these powerful technologies to your benefit.

Maintaining Momentum: Ongoing Savings Strategies for a Secure Future

Achieving significant savings through negotiation and initial expense reduction is a fantastic start, but the journey to financial mastery is continuous. To truly secure your financial future and build lasting wealth, it’s essential to establish ongoing strategies that keep your expenses low and your savings growing. This requires vigilance, regular review, and a proactive approach to your finances.

Cultivating a Culture of Continuous Financial Optimization

- Regular Budget Review: Your budget isn’t a static document. Life changes, income fluctuates, and expenses evolve. Make it a habit to review your budget monthly or quarterly. This allows you to catch any spending creep, reallocate funds, and identify new opportunities for savings or negotiation.

- Annual Bill Audit: Set a reminder to conduct an annual audit of all your major recurring bills. This is the perfect time to re-negotiate internet, cable, phone, and insurance rates. Many companies offer new promotions annually, and being proactive ensures you don’t miss out on savings. Think of it as your yearly financial check-up.

- Question Every Recurring Charge: Before automatically renewing a subscription or paying a bill, ask yourself: “Am I getting full value from this? Is there a cheaper alternative? Can I negotiate this?” This critical thinking prevents unnecessary financial leakage.

- Embrace the “No-Spend” Challenge: Periodically challenge yourself to a “no-spend” day, weekend, or even a week (excluding essentials). This practice not only saves money but also helps you become more aware of your spending triggers and differentiates between needs and wants.

- Optimize Your Taxes: While not a direct bill negotiation, understanding tax credits, deductions, and optimizing your withholding can significantly impact your net income. Consider consulting a tax professional or utilizing tax software to ensure you’re not overpaying.

- Invest in Financial Education: Continuously educate yourself on personal finance topics. The more you understand about investing, debt management, market trends, and economic shifts, the better equipped you’ll be to make informed decisions that protect and grow your wealth. Fin3go is here to be your ongoing resource.

- Set Clear Financial Goals: Having tangible goals – whether it’s saving for a down payment, early retirement, or funding a child’s education – provides powerful motivation to maintain your savings momentum. Regularly revisit these goals to ensure your financial actions are aligned with your aspirations.

By integrating these ongoing strategies into your financial routine, you transform one-time savings into a perpetual engine for wealth creation. This sustained effort not only lowers your immediate expenses but also builds the financial resilience and capital necessary to pursue ambitious objectives, including the long-term vision of How To Build Generational Wealth for your family, securing a brighter financial future for 2026 and beyond.

Frequently Asked Questions

Can I negotiate all types of bills?▾

What if I’m not good at negotiating or feel uncomfortable doing it?▾

How often should I attempt to negotiate my bills?▾

What documents or information should I have ready before calling to negotiate?▾

Is it better to call or email when negotiating bills?▾

What’s the riskiest bill to negotiate, and what should I be aware of?▾

Recommended Resources

Explore How To Improve Employee Productivity In Your Company for additional insights.

Check out On Page Seo Checklist 2026 on Page Release for a deeper dive.