Online Banks vs. Credit Unions: A 2026 Guide to Maximizing Your Money

The financial world of 2026 is characterized by heightened digital integration, personalized services, and a strong emphasis on value. Online banks, often called neobanks or challenger banks, have continued their trajectory of growth, leveraging technology to offer streamlined, low-cost services. Credit unions, on the other hand, have held steadfast to their member-centric cooperative model, adapting to digital demands while retaining their community focus. Deciding between them isn’t merely about convenience; it’s about aligning your financial institution with your values, spending habits, saving goals, and the level of personalized service you desire. Let’s dive deep into what each offers and how they stack up.

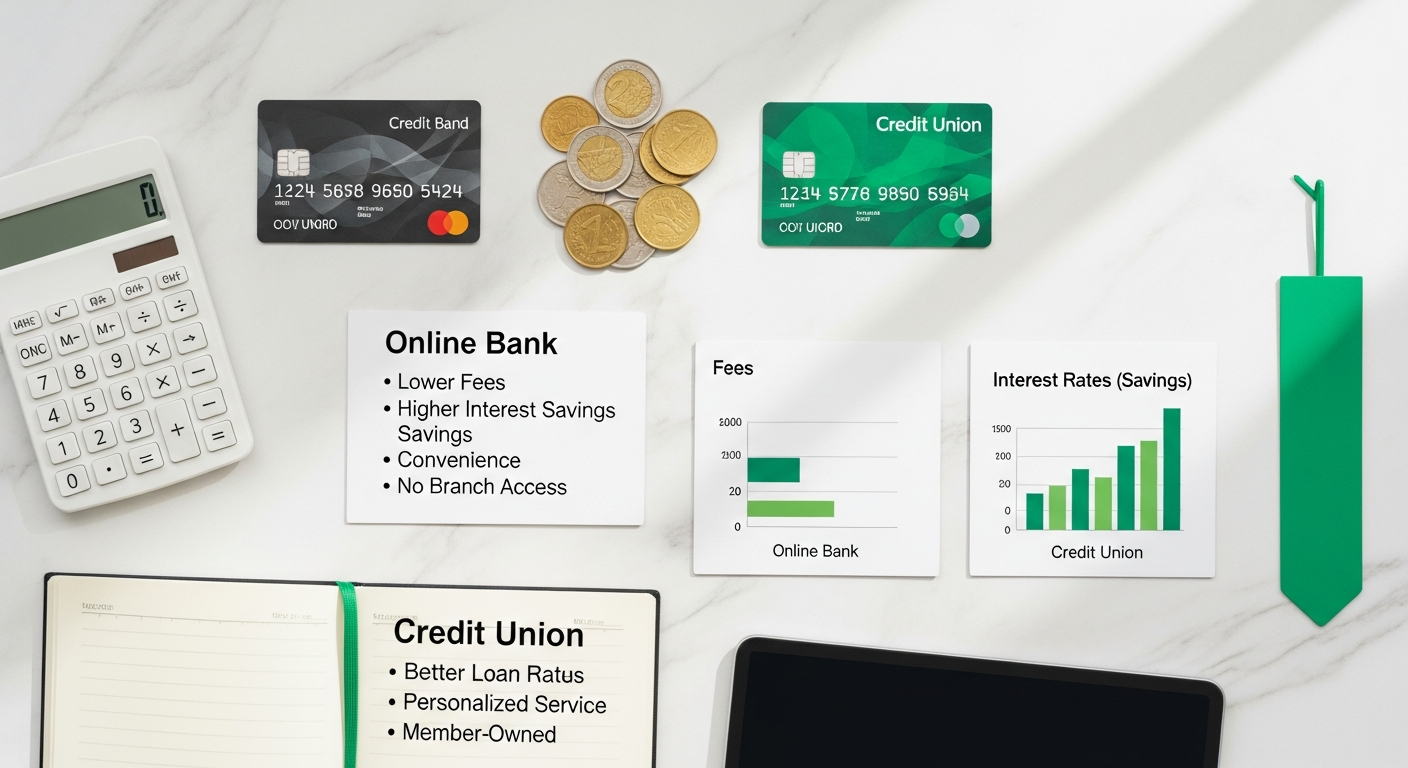

Understanding Online Banks: The Digital Frontier of Finance

Online banks, by definition, operate without physical branches. This lean operational model allows them to pass significant savings onto their customers in the form of higher interest rates on savings accounts, lower fees, and sometimes, no fees at all. They are digital-first, meaning all banking activities – from opening an account to depositing checks, transferring funds, and applying for loans – are conducted entirely through their websites or mobile applications. By 2026, the sophistication of these digital platforms has reached new heights, offering intuitive interfaces, advanced budgeting tools, and often AI-powered insights into spending patterns.

The core appeal of online banks lies in their efficiency and competitive offerings. Without the overhead of maintaining a vast network of physical branches and staffing them, they can afford to offer significantly more attractive Annual Percentage Yields (APYs) on savings accounts and Certificates of Deposit (CDs) compared to most traditional banks. This can translate into hundreds, even thousands, of extra dollars in interest earned over time, especially for individuals with substantial savings. Furthermore, many online banks have pioneered fee-free banking, eliminating common charges like monthly maintenance fees, overdraft fees (or offering robust overdraft protection options), and foreign transaction fees.

However, the lack of a physical presence can be a double-edged sword. While the convenience of banking from anywhere at any time is undeniable, some individuals prefer the option of walking into a branch to speak with a human teller, especially for complex transactions or financial advice. Online banks typically address this by offering 24/7 customer support via phone, chat, or email, and by integrating with extensive ATM networks (often fee-free) for cash withdrawals and, in some cases, deposits. For those comfortable with technology and self-service, online banks represent a powerful tool for maximizing savings and minimizing banking costs in 2026.

Key Features and Considerations for Online Banks:

- Higher Interest Rates: Consistently offer some of the highest APYs on savings, money market, and CD accounts.

- Lower/No Fees: Many boast fee-free checking and savings, with minimal charges for other services.

- Advanced Mobile Apps: State-of-the-art apps for all banking needs, including mobile check deposit, bill pay, budgeting tools, and instant transfers.

- Accessibility: 24/7 access to accounts and customer service, regardless of location.

- FDIC Insured: Deposits are typically insured up to $250,000 per depositor, per institution, ensuring security.

- Cash Handling: Reliance on ATM networks for cash withdrawals and increasingly sophisticated solutions (like retail partnerships or specific apps) for cash deposits.

Exploring Credit Unions: Community-Focused Financial Cooperatives

Historically, credit unions have been known for their personalized customer service and community involvement. While they have embraced digital transformation, offering robust online banking and mobile apps in 2026, many still maintain a network of physical branches, providing a hybrid banking experience. Membership typically requires meeting specific criteria, such as living in a particular geographic area, working for a certain employer, or being affiliated with a specific organization. However, many credit unions have broad eligibility requirements that make it easy for almost anyone to join.

The financial benefits of credit unions often manifest in various ways. They frequently offer more favorable loan rates for mortgages, auto loans, and personal loans compared to traditional banks. Their savings rates, while often not reaching the peak APYs of top online banks, are generally more competitive than those found at large national banks. Furthermore, credit unions are renowned for their willingness to work with members, offering financial counseling, flexible payment options, and a more understanding approach during financial difficulties. This member-first philosophy fosters a strong sense of trust and loyalty among their clientele.

Key Features and Considerations for Credit Unions:

- Member-Owned: Profits are returned to members through better rates and services.

- Personalized Service: Often provide a more human, relationship-driven banking experience.

- Competitive Loan Rates: Tend to offer lower interest rates on loans (auto, mortgage, personal).

- Lower Fees: Generally have lower fees or are more willing to waive them for members.

- NCUA Insured: Deposits are federally insured up to $250,000 by the National Credit Union Administration (NCUA), offering equivalent safety to FDIC insurance.

- Community Focus: Strong emphasis on local community development and financial education for members.

- Shared Branching: Many participate in shared branching networks, allowing members to conduct transactions at thousands of credit union branches nationwide, mitigating the limitation of a smaller branch network.

Interest Rates and Fees: Where Your Money Grows Faster

When it comes to the bottom line – how much your money earns and how much you pay to access it – the comparison between online banks and credit unions can be quite stark, though not always unilaterally favoring one over the other. As we move through 2026, the competitive landscape has only intensified, with both models striving to offer compelling value propositions.

Online Banks typically excel in offering superior interest rates on deposits. Their low operational overhead directly translates into higher APYs on savings accounts, money market accounts, and Certificates of Deposit (CDs). For a saver, even a fraction of a percentage point difference can amount to significant additional earnings over time. For example, if a leading online bank offers 4.50% APY on a high-yield savings account while a traditional bank offers 0.50% and a credit union offers 1.50%, the choice for maximizing passive income is clear. Furthermore, online banks have been at the forefront of the “no-fee” movement. Many offer checking accounts with no monthly maintenance fees, no minimum balance requirements, and often reimburse ATM fees from other banks, creating a truly cost-effective banking experience.

Credit Unions, while often lagging behind the very top online banks in savings APYs, generally offer better rates than large traditional banks. Their real competitive edge, however, often lies in their loan products. Credit unions are consistently cited for offering lower interest rates on auto loans, personal loans, and even mortgages. This is a significant advantage for members looking to borrow money, as lower interest rates translate directly into less money paid over the life of the loan. On the fee front, credit unions are also highly competitive. They typically have lower fees than traditional banks and are more likely to work with members to waive fees or restructure payment plans in times of need, reflecting their member-centric approach. They might not always offer entirely “fee-free” accounts like some online banks, but their fees are usually reasonable and transparent.

For someone primarily focused on growing their savings without incurring fees, online banks often present the most attractive option in 2026. For those looking to secure favorable loan terms, value personalized service, and benefit from generally lower overall banking costs, a credit union could be the superior choice. It’s essential to compare specific products and rates from institutions you’re considering, as offerings can vary widely.

Customer Service and Accessibility: High-Tech vs. High-Touch

The manner in which you interact with your financial institution is a major factor in satisfaction and ease of managing your money. In 2026, both online banks and credit unions have adapted to meet evolving customer expectations, but their core approaches to service and accessibility remain distinct.

Online Banks are the epitome of convenience for the digitally savvy. Their accessibility is 24/7, from anywhere with an internet connection. Their primary service channels are digital: robust mobile apps, intuitive websites, email, and live chat. Many also offer phone support, often around the clock. The customer service experience is typically efficient and self-directed. For common queries or transactions, the advanced AI-powered chatbots and extensive FAQs on their platforms can provide immediate answers. For more complex issues, reaching a human representative might involve a phone call, which, while efficient, lacks the face-to-face interaction some prefer. The lack of physical branches means no waiting in line at a teller, but also no direct human contact for advice or specialized services, which could be a drawback for those who value personal relationships with their bankers.

Credit Unions, while embracing digital tools, have maintained a strong emphasis on personalized, high-touch service. Many still operate physical branches, allowing members to walk in, speak with a representative, and receive tailored advice. This face-to-face interaction can be invaluable for complex financial decisions, applying for loans, or simply building a relationship with a financial advisor. In 2026, credit unions continue to invest in their digital platforms, offering mobile check deposit, online bill pay, and robust mobile apps that rival those of traditional banks and some online-only institutions. Furthermore, the shared branching network is a significant accessibility advantage for credit unions. It allows members of one credit union to conduct transactions at thousands of other credit union branches across the country, effectively expanding their physical footprint far beyond their individual network. This combines the benefit of in-person service with the convenience of a wider network.

The choice here hinges on your personal preference. If you prioritize maximum digital convenience, self-service, and rarely need in-person assistance, an online bank will likely meet your needs. If you value the option of talking to a person, appreciate a more community-oriented approach, or anticipate needing personalized financial advice, a credit union’s hybrid model might be more appealing, especially with the extended reach of shared branching.

Technology and Digital Tools: The Future of Banking Today

The digital experience is paramount in 2026, and both online banks and credit unions have made significant strides in their technological offerings. However, their approaches and priorities in this realm can differ.

Online Banks are inherently technology-driven. Their existence is predicated on delivering a seamless digital experience. This means their mobile apps and web platforms are often cutting-edge, featuring intuitive interfaces, advanced security protocols, and innovative tools. Expect features like:

- Advanced Budgeting & Spending Trackers: Many integrate with personal finance management (PFM) tools or offer their own, providing detailed insights into spending categories, recurring payments, and saving trends.

- AI-Powered Insights: Some online banks leverage artificial intelligence to offer personalized financial advice, detect unusual spending, or recommend ways to save money automatically.

- Mobile Check Deposit: A standard feature that allows users to deposit checks simply by snapping a photo with their smartphone.

- Seamless Transfers: Easy and often instant transfers between internal accounts, external banks, and peer-to-peer payments.

- Virtual Cards & Digital Wallets: Integration with Apple Pay, Google Pay, and often offering virtual debit card numbers for enhanced online security.

- Open Banking & API Integrations: Many are built with open banking principles, allowing for easier and more secure connections with third-party financial apps and services.

These features are designed for maximum convenience and self-sufficiency, appealing to a tech-savvy generation that expects their banking to be as fluid and integrated as other digital services.

Credit Unions, while historically slower to adopt bleeding-edge tech, have significantly ramped up their digital offerings by 2026. Recognizing the importance of digital access, most now offer robust mobile apps and online banking platforms that cover all essential functions, including:

- Mobile Check Deposit: Widely available across most credit unions.

- Online Bill Pay: Conveniently pay bills directly from your account.

- Account Management: View balances, transaction history, and manage alerts.

- Secure Messaging: Communicate with member service representatives through secure channels within the app.

- ATM Finders: Locate both their own ATMs and those within shared networks.

While credit unions may not always have the absolute latest AI-driven insights or the most polished UI/UX compared to some challenger banks, they provide a reliable and comprehensive digital experience. Their focus is often on functionality and security, ensuring members can manage their finances effectively online while still having the option for in-person support when needed. Many have also invested in enhancing cybersecurity measures, ensuring that member data is protected against the evolving threats of the digital age.

If you’re an early adopter of technology and prioritize the most advanced digital tools and features, an online bank might be more your speed. If you prefer a solid, reliable digital banking experience that complements traditional services, a credit union will likely serve you well without sacrificing essential online functionalities.

Loan Products and Financial Services: Beyond Basic Banking

While checking and savings accounts are the bread and butter of any financial institution, the availability and competitiveness of other financial products – particularly loans – can significantly impact your overall financial journey. Both online banks and credit unions offer a range of services beyond basic deposits, but with different strengths.

Online Banks have expanded their product offerings considerably. While initially focused on high-yield savings, many now provide competitive checking accounts, Certificates of Deposit (CDs), and even some lending products. Common loan offerings from online banks in 2026 include:

- Personal Loans: Often with competitive rates and streamlined online application processes.

- Mortgages: A growing number of online lenders and some online banks offer competitive mortgage rates and a fully digital application and approval process, which can be much faster than traditional methods.

- Auto Loans: Similarly, online applications for auto loans are becoming more prevalent and efficient.

- Credit Cards: Many online banks have their own branded credit cards, often designed to complement their deposit products with competitive rewards or low interest rates.

The strength of online banks in lending often lies in their efficiency and data-driven approach. They can often process applications quickly, offering rapid approvals and disbursements. However, their lending criteria can sometimes be less flexible than credit unions, relying heavily on credit scores and automated underwriting processes. They might be less inclined to work with individuals who have a less-than-perfect credit history, though this is evolving with more sophisticated risk assessment models.

Credit Unions are often the preferred choice for members seeking loans due to their typically lower interest rates and more flexible underwriting. As member-owned institutions, they are structured to provide financial assistance to their members, often leading to better terms than what might be available at for-profit institutions. Their loan products commonly include:

- Auto Loans: Consistently praised for highly competitive rates on new and used car loans.

- Mortgages: Offer a range of mortgage products (fixed-rate, adjustable-rate, FHA, VA) with competitive interest rates and often more personalized guidance through the application process.

- Personal Loans: Accessible personal loans for various needs, often with more flexible terms and a willingness to consider individual circumstances beyond just credit scores.

- Credit Cards: Typically offer credit cards with lower interest rates and fewer fees compared to many bank-issued cards.

- Student Loans: Some credit unions also offer private student loans or refinancing options.

- Small Business Loans: Many community-focused credit unions provide essential lending to local small businesses, supporting economic development.

Credit unions’ willingness to consider the “whole person” rather than just a credit score, their commitment to financial counseling, and their lower interest rates make them a powerful ally for anyone needing to borrow money. They excel in fostering a relationship that goes beyond transactions, aiming to help members achieve their financial goals through accessible and affordable credit.

If you primarily need high-yield savings and prefer a digital-first lending experience with good credit, online banks offer efficiency. But if you value competitive loan rates, personalized guidance, and potentially more flexible lending criteria, especially if your credit history isn’t pristine, a credit union often provides superior value.

Safety and Security: Protecting Your Deposits in 2026

Regardless of whether you choose an online bank or a credit union, the safety and security of your money should be a paramount concern. Fortunately, both types of institutions offer robust protection for your deposits, mandated by federal regulations.

Online Banks are typically regulated in the same way as traditional banks. Most reputable online banks in the United States are members of the Federal Deposit Insurance Corporation (FDIC). This means that your deposits are insured up to the standard maximum of $250,000 per depositor, per ownership category, per insured bank. This insurance covers checking accounts, savings accounts, money market deposit accounts, and Certificates of Deposit (CDs). In the event of an online bank’s failure, the FDIC would step in to ensure you recover your insured funds. Beyond deposit insurance, online banks invest heavily in cybersecurity. Their entire operation relies on digital security, so they employ state-of-the-art encryption, multi-factor authentication, fraud detection systems, and continuous monitoring to protect customer data and transactions from cyber threats, which are increasingly sophisticated in 2026. They often offer advanced security features within their apps, such as biometric login and real-time alerts for suspicious activity.

Credit Unions provide equivalent protection for your deposits through the National Credit Union Administration (NCUA). The NCUA is an independent federal agency that charters and supervises federal credit unions and insures deposits at federal and state-chartered credit unions. Similar to the FDIC, NCUA insurance protects your savings up to $250,000 per depositor, per ownership category, per insured credit union. This ensures that your money is safe, even if the credit union were to fail. Credit unions also prioritize cybersecurity, implementing strong encryption, secure online banking platforms, and fraud prevention measures. While they may have a physical presence, their digital security protocols are just as vital to their operations and are regularly audited to meet stringent federal standards. Many credit unions also offer additional layers of security through educational resources for members on fraud prevention and identity theft.

Therefore, when considering safety and security, there is no inherent advantage of one over the other in terms of federal deposit insurance. Both FDIC and NCUA insurance provide the same level of protection for your deposits. The key is to ensure that the online bank is FDIC-insured or the credit union is NCUA-insured, which nearly all legitimate institutions are. Your personal security habits, such as using strong passwords and being wary of phishing attempts, are equally crucial in protecting your accounts.

Summary: Making the Right Choice for Your Financial Future

The choice between an online bank and a credit union in 2026 boils down to your personal financial priorities, preferences, and lifestyle. Online banks typically offer superior interest rates on deposits and often boast lower or no fees, leveraging technology for unparalleled convenience and efficiency. They are ideal for tech-savvy individuals who prioritize maximizing savings, are comfortable with digital-only interactions, and rarely need in-person assistance. Credit unions, on the other hand, shine with their member-owned model, often providing more competitive loan rates, personalized customer service, and a strong community focus. They appeal to those who value a relationship-based banking experience, desire flexible lending options, and appreciate the option of physical branches or shared networks. Both offer robust federal deposit insurance, ensuring the safety of your money. Ultimately, the “better” option is the one that best aligns with your financial goals, banking habits, and the level of personalized interaction you seek to maximize your money and foster your financial well-being.