What is Portfolio Diversification?

At its heart, portfolio diversification explained simply means not putting all your eggs in one basket. Imagine you’re carrying a basket of eggs, and you trip. If all your eggs are in that one basket, you could lose them all. However, if you had distributed your eggs across several different baskets, a mishap with one basket wouldn’t result in the total loss of your egg supply. This age-old analogy perfectly encapsulates the essence of diversification in investing.

In financial terms, diversification is the practice of investing in a variety of assets that react differently to various market conditions. The goal is to minimize the risk of your entire portfolio suffering significant losses due to the underperformance of any single investment or asset class. By combining assets with different risk and return characteristics, investors aim to achieve a smoother, more consistent return profile over time, even amidst market volatility.

A well-diversified portfolio seeks to balance assets that might perform well in an economic boom with those that might hold their value, or even thrive, during a downturn. For instance, while stocks might soar during periods of economic growth, bonds often provide stability and income during recessions. Real estate might offer long-term capital appreciation and rental income, while commodities could hedge against inflation. The beauty of diversification lies in this offsetting relationship, where the poor performance of one asset can be mitigated by the strong performance of another.

The importance of diversification has been highlighted repeatedly throughout history, particularly during periods of market turmoil. Investors who had concentrated their wealth in a single stock, sector, or even a single country often faced severe losses when those specific investments faltered. Conversely, those with diversified portfolios typically experienced less severe drawdowns and were often quicker to recover. Understanding this fundamental principle is the first step towards building a robust financial future. It’s not about avoiding risk entirely, which is impossible in investing, but about managing and optimizing it to achieve your long-term financial objectives.

The Core Principles of Diversification

To effectively implement portfolio diversification, it’s crucial to understand the foundational principles upon which it rests. These principles guide investors in selecting and allocating assets to create a resilient and balanced portfolio.

Asset Allocation: The Foundation

The bedrock of diversification is asset allocation. This refers to the strategic distribution of your investment capital across various asset classes, such as stocks (equities), bonds (fixed income), cash, real estate, and alternative investments. The choice of asset classes and their respective proportions in your portfolio is perhaps the most critical decision in investment planning, often having a greater impact on your long-term returns than individual stock picking.

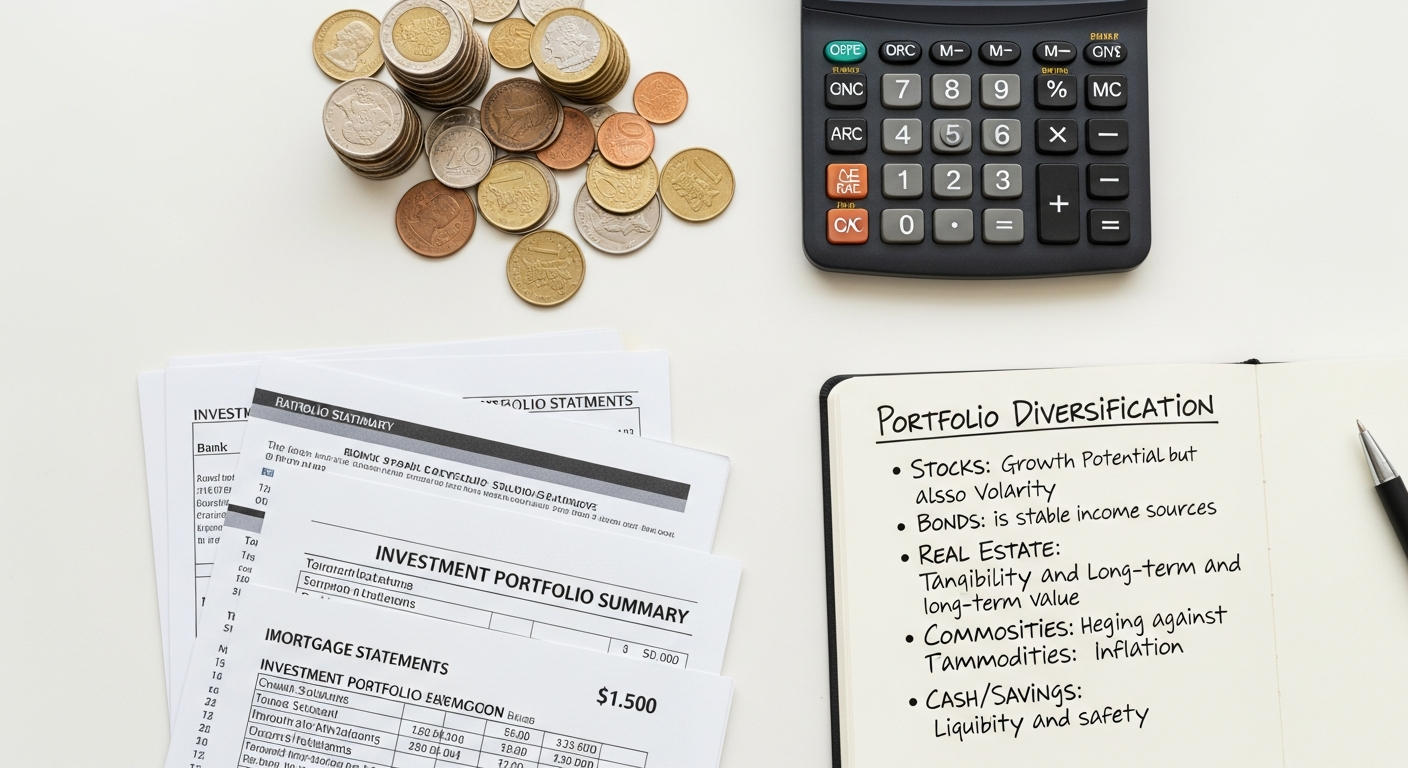

- Stocks (Equities): Generally offer higher growth potential but come with greater volatility. They represent ownership in companies.

- Bonds (Fixed Income): Tend to be less volatile than stocks, providing a steady income stream and capital preservation. They represent loans made to governments or corporations.

- Cash and Cash Equivalents: Provide liquidity and safety, though typically with lower returns. Essential for emergency funds.

- Real Estate: Can offer capital appreciation and rental income, acting as a hedge against inflation. This can be direct property ownership or through Real Estate Investment Trusts (REITs).

- Alternative Investments: A broad category including commodities, private equity, hedge funds, and even certain cryptocurrencies. These can add further diversification but often come with higher risk or illiquidity.

Your ideal asset allocation will depend heavily on your investment horizon, risk tolerance, and financial goals. A younger investor with a longer time horizon might opt for a higher percentage of stocks for growth, while someone nearing retirement might lean more towards bonds for capital preservation and income.

Understanding Correlation: The Key to Effective Diversification

The effectiveness of diversification hinges on the concept of correlation. Correlation measures how two different assets move in relation to each other.

- Positive Correlation: Assets move in the same direction. If Asset A goes up, Asset B tends to go up. Diversifying with highly positively correlated assets offers little risk reduction.

- Negative Correlation: Assets move in opposite directions. If Asset A goes up, Asset B tends to go down. These assets are highly valuable for diversification as they can offset each other’s movements.

- Zero Correlation: Assets move independently of each other. Their movements have no discernible relationship.

The goal of diversification is to combine assets that have low or negative correlation. For example, stocks and bonds often exhibit low or negative correlation; when stock markets are falling due to economic uncertainty, investors might flock to bonds, driving their prices up. By including both in your portfolio, you reduce overall portfolio volatility.

Risk vs. Return: Optimizing the Balance

Diversification doesn’t eliminate risk, but it helps in optimizing the risk-return tradeoff. By combining various assets, you aim to achieve the highest possible return for a given level of risk, or conversely, the lowest possible risk for a desired level of return. This concept is central to Modern Portfolio Theory (MPT), pioneered by Nobel laureate Harry Markowitz, which suggests that investors can construct an “efficient frontier” of portfolios that offer the best possible expected return for their level of risk. A diversified portfolio, therefore, is not just about spreading risk; it’s about strategically combining assets to improve the overall efficiency of your investment.

Types of Diversification Strategies

1. Asset Class Diversification

As discussed, this is the most fundamental form. It involves allocating your investments across different asset categories, each with its own risk and return characteristics.

- Equities (Stocks): Can be further diversified by market capitalization (large-cap, mid-cap, small-cap), growth vs. value styles, and domestic vs. international markets.

- Fixed Income (Bonds): Diversify by issuer (government, corporate, municipal), credit quality (investment grade, high-yield), maturity (short-term, intermediate-term, long-term), and geographic location.

- Real Estate: Can be accessed through direct property ownership, REITs (Real Estate Investment Trusts), or real estate funds.

- Commodities: Such as gold, silver, oil, and agricultural products. Often used as inflation hedges.

- Cash and Cash Equivalents: Money market funds, high-yield savings accounts.

2. Geographic Diversification

Investing solely in your home country ties your portfolio’s fate closely to that nation’s economic and political health. Geographic diversification means spreading your investments across different countries and regions worldwide.

- Developed Markets: Countries like the U.S., Canada, Western Europe, and Japan. Generally more stable but with potentially lower growth rates.

- Emerging Markets: Countries like China, India, Brazil, and parts of Southeast Asia. Offer higher growth potential but come with increased political and economic risk.

This strategy protects your portfolio from country-specific downturns, currency fluctuations, and geopolitical risks. For instance, if the U.S. economy faces a recession, a portfolio with exposure to thriving Asian markets might help cushion the blow.

3. Industry/Sector Diversification

Even within the stock market, concentrating all your equity investments in a single industry can be risky. Industry/sector diversification involves spreading your investments across various economic sectors.

- Technology: Software, hardware, internet services.

- Healthcare: Pharmaceuticals, biotech, medical devices.

- Financials: Banks, insurance companies, investment firms.

- Consumer Staples: Food, beverages, household goods (tend to be resilient in downturns).

- Utilities: Electricity, gas, water providers (stable, often regulated).

Different sectors perform differently depending on the economic cycle. For example, technology stocks might thrive during periods of innovation and growth, while consumer staples might be more defensive during recessions. By diversifying across sectors, you avoid being overly reliant on the performance of a single industry.

4. Market Capitalization Diversification

Within the equity class, companies are often categorized by their market capitalization (the total value of a company’s outstanding shares).

- Large-Cap Stocks: Established, financially stable companies (e.g., Apple, Microsoft). Often less volatile.

- Mid-Cap Stocks: Medium-sized companies with growth potential.

- Small-Cap Stocks: Smaller companies, often with higher growth potential but also higher risk and volatility.

Including a mix of these can provide exposure to different growth drivers and risk profiles.

5. Investment Style Diversification

Investors often categorize stocks by their “style.”

- Growth Stocks: Companies expected to grow earnings and revenues at a faster rate than the market average.

- Value Stocks: Companies that appear to be undervalued by the market, often paying dividends.

These styles can perform differently in various market environments. A diversified portfolio often includes both.

6. Time Diversification (Dollar-Cost Averaging)

While not diversification of assets, time diversification, often implemented through dollar-cost averaging, is a crucial strategy for managing risk. Instead of investing a large lump sum all at once, which exposes you to the risk of investing at a market peak, dollar-cost averaging involves investing a fixed amount of money at regular intervals (e.g., monthly).

This strategy ensures you buy more shares when prices are low and fewer when prices are high, effectively averaging out your purchase price over time. It reduces the impact of market timing risk and can be particularly beneficial for long-term investors contributing to their portfolios regularly, like through employer-sponsored retirement plans.

By thoughtfully combining these diversification strategies, investors can build a robust portfolio designed to withstand various economic conditions and achieve their financial objectives over the long haul.

Benefits of a Diversified Portfolio

The strategic implementation of portfolio diversification offers a multitude of advantages that are crucial for long-term financial success and peace of mind. These benefits underscore why it remains a cornerstone of prudent investing.

1. Risk Mitigation and Reduction of Volatility

The most significant and widely recognized benefit of diversification is its ability to mitigate risk. By spreading your investments across various assets with different risk profiles and correlations, you reduce the impact of any single investment’s poor performance. If one asset class or sector experiences a downturn, the negative effect on your overall portfolio is cushioned by the performance of other, potentially uncorrelated, assets. This smoothing effect leads to lower portfolio volatility, meaning less dramatic swings in the value of your investments. For instance, during a stock market crash, a diversified portfolio with a healthy allocation to bonds might experience a smaller decline than a portfolio concentrated solely in equities.

2. Smoother, More Consistent Returns Over Time

While diversification doesn’t guarantee higher returns, it significantly enhances the likelihood of achieving smoother and more consistent returns over the long term. Instead of chasing the highest-performing asset each year (a futile endeavor), a diversified portfolio aims for steady, incremental growth. By avoiding significant losses that can result from concentrated bets, a diversified approach helps your portfolio recover more quickly from market corrections and maintains a more predictable growth trajectory. This consistency is invaluable for investors planning for major life events like retirement or funding future projects, such as building up streams of Passive Income Ideas 2026.

3. Enhanced Long-Term Growth Potential

Paradoxically, by reducing risk, diversification can also lead to enhanced long-term growth potential. How? By ensuring that your portfolio isn’t derailed by a single catastrophic event. A highly concentrated portfolio might offer astronomical returns if a single bet pays off, but it carries an equally high risk of devastating losses. A diversified portfolio, by consistently capturing returns from various market segments, is better positioned to compound wealth steadily over decades, ultimately leading to substantial growth. It enables investors to stay invested through market cycles, benefiting from the market’s overall upward trend without being overly exposed to the inevitable individual asset class or sector downturns.

4. Capital Preservation

Beyond growth, diversification plays a vital role in capital preservation. For investors closer to retirement or those with a lower risk tolerance, protecting their principal investment becomes paramount. A well-diversified portfolio, particularly one with a balanced allocation to less volatile assets like high-quality bonds, can help safeguard your accumulated wealth against significant market drawdowns, ensuring that your financial resources are available when you need them most.

5. Peace of Mind and Reduced Emotional Investing

Perhaps one of the most underrated benefits of diversification is the peace of mind it offers. Knowing that your financial future isn’t tied to the fortunes of a single company or industry can significantly reduce stress during periods of market uncertainty. This psychological comfort helps investors avoid impulsive, emotional decisions, such as panic-selling during a downturn or chasing “hot” investments during a boom. By adhering to a well-diversified strategy, investors are better able to stick to their long-term plan, which is often the most critical factor in achieving financial success. It reinforces the discipline learned from consistent financial planning, akin to how a detailed guide on How To Create A Monthly Budget helps maintain spending discipline.

In essence, diversification is a powerful tool that, when implemented thoughtfully, creates a more robust, stable, and ultimately more successful investment experience. It’s about building a portfolio that can weather storms and capture opportunities, leading you steadily towards your financial goals.

Common Diversification Mistakes to Avoid

While diversification is a powerful strategy, it’s not foolproof. Investors can sometimes make mistakes that undermine its effectiveness, turning a potentially robust strategy into a suboptimal one. Being aware of these common pitfalls is as important as understanding the principles of diversification itself.

1. Over-Diversification (Diworsification)

There’s a fine line between adequate diversification and over-diversification, sometimes jokingly referred to as “diworsification.” While spreading your investments across different assets is good, owning too many different investments can dilute your returns without significantly reducing additional risk. For instance, buying 50 different mutual funds that all invest in large-cap U.S. equities doesn’t add much diversification beyond what 5-10 well-chosen funds would provide. Instead, it often leads to:

- Diluted Returns: The strong performance of a few assets is offset by the mediocre performance of many others.

- Increased Complexity: Managing a portfolio with too many holdings becomes cumbersome, making it difficult to track performance, rebalance, and understand your true exposure.

- Higher Fees: Each additional fund or stock might come with its own management fees or trading costs, which can eat into your returns.

The goal is to have enough investments to spread risk effectively, not to own every possible asset. For most investors, a portfolio comprising a few well-chosen ETFs or mutual funds covering different asset classes and geographies is sufficient.

2. Ignoring Correlation

True diversification requires investing in assets that are not highly correlated. A common mistake is to invest in many different assets that tend to move in the same direction. For example, buying shares in ten different technology companies might seem diversified, but if all these companies are highly sensitive to the same market conditions (e.g., interest rate hikes, tech sector downturns), you’re not truly diversified. You’ve simply concentrated your risk within a single, albeit broad, sector. Always consider how different assets behave under various market scenarios.

3. Neglecting Rebalancing

4. Emotional Investing and Herd Mentality

Diversification is a long-term strategy that requires discipline. Giving in to emotional impulses, such as panic-selling during market downturns or chasing “hot” investments that have already experienced significant gains, can completely undo the benefits of diversification. The “herd mentality”—following what everyone else is doing—often leads to buying high and selling low, directly contradicting sound investment principles. A diversified portfolio is designed to help you weather market storms, making it easier to stick to your plan and avoid costly emotional decisions.

5. Focusing Only on Past Performance

While past performance can offer insights, it is by no means a guarantee of future results. A common mistake is to diversify into funds or assets solely based on their recent stellar performance. Often, by the time an asset has caught widespread attention for its returns, much of its significant growth may have already occurred. Moreover, assets that performed well in one market cycle might underperform in the next. Diversification should be based on fundamental principles, risk tolerance, and long-term goals, not on chasing past winners.

6. Underestimating the Impact of Fees and Taxes

While not directly a diversification mistake, ignoring investment fees and taxes can significantly erode your diversified portfolio’s returns. Excessive trading to diversify, investing in funds with high expense ratios, or generating unnecessary taxable events can reduce your net gains. Always be mindful of the costs associated with your investments and seek tax-efficient strategies where possible.

By being aware of and actively avoiding these common pitfalls, investors can ensure their diversification strategy truly serves its purpose: reducing risk and fostering stable, long-term growth.

Building Your Diversified Portfolio

Constructing a diversified portfolio is a personalized process that requires careful consideration of your financial situation, goals, and risk tolerance. It’s not a one-size-fits-all solution but a strategic framework tailored to your unique circumstances.

Step 1: Assess Your Financial Foundation and Goals

Before you even think about specific investments, you need a clear picture of your overall financial health.

- Create a Monthly Budget: Understanding your income and expenses is fundamental. Knowing How To Create A Monthly Budget helps you identify how much you can realistically save and invest each month without compromising your essential needs. This budget also highlights areas where you might be overspending, freeing up more capital for investment.

- Build an Emergency Fund: Before investing for growth, ensure you have 3-6 months’ worth of living expenses saved in an easily accessible, liquid account. This prevents you from having to sell investments at an inopportune time due to unexpected expenses.

- Manage High-Interest Debt: High-interest debt (like credit card debt) can quickly erode investment gains. Prioritize paying off such debts. Understanding methods like the Snowball Vs Avalanche Debt Payoff Method can help you strategically tackle your liabilities, clearing the path for more aggressive investing.

- Define Your Financial Goals: What are you investing for? Retirement? A down payment on a house? Funding your children’s education? Generating Passive Income Ideas 2026? Clearly defined goals with specific timelines will dictate your investment horizon and guide your asset allocation decisions.

Step 2: Determine Your Risk Tolerance

Your willingness and ability to take on investment risk are crucial.

- Risk Tolerance: This is your psychological comfort level with potential losses. Are you comfortable with significant market fluctuations for potentially higher returns, or do you prefer stability even if it means lower growth?

- Risk Capacity: This is your financial ability to withstand losses without jeopardizing your financial goals. A younger investor with a long time horizon generally has a higher risk capacity than someone nearing retirement.

Be honest with yourself. An overly aggressive portfolio might lead to panic selling during downturns, while an overly conservative one might not achieve your long-term goals.

Step 3: Choose Your Asset Allocation

Based on your goals, time horizon, and risk tolerance, decide on the percentage of your portfolio to allocate to each major asset class (stocks, bonds, cash, real estate, etc.).

- Aggressive: Higher percentage in stocks (e.g., 80% stocks, 20% bonds). Suitable for long horizons and high risk tolerance.

- Moderate: Balanced mix (e.g., 60% stocks, 40% bonds). Common for many investors.

- Conservative: Higher percentage in bonds and cash (e.g., 30% stocks, 70% bonds). Suitable for short horizons or low risk tolerance.

Remember the “age rule” (100 or 110 minus your age in stocks) as a rough starting point, but always customize it to your personal situation.

Step 4: Select Specific Investments for Diversification

Once you have your target asset allocation, select the specific investment vehicles to achieve that mix.

- Low-Cost Index Funds and ETFs: These are excellent tools for diversification. They track broad market indexes (like the S&P 500) or specific sectors/geographies, providing instant diversification across many underlying securities at a very low cost.

- Mutual Funds: Actively managed funds can also provide diversification, but be mindful of higher expense ratios.

- Individual Stocks and Bonds: For experienced investors who enjoy research and have the time to manage a more complex portfolio, individual securities can be chosen. However, even then, ensure you own a sufficient number across different industries and geographies to be truly diversified.

- Real Estate: Consider REITs for liquid exposure to real estate without direct property ownership.

Ensure your selections achieve diversification across:

- Asset Classes: Stocks, bonds, real estate, cash.

- Geographies: Domestic, international, emerging markets.

- Industries/Sectors: Technology, healthcare, financials, consumer goods, utilities, etc.

- Market Capitalization: Large-cap, mid-cap, small-cap.

Step 5: Implement and Monitor

Set up your investment accounts (brokerage, IRA, 401k) and execute your investment plan. Once implemented, your portfolio isn’t static. It needs regular monitoring. Review your portfolio at least annually to ensure it still aligns with your goals and risk tolerance. Markets change, and so might your life circumstances.

Building a diversified portfolio is an ongoing process, not a one-time event. By following these steps and regularly assessing your financial landscape, you can construct a robust portfolio designed for long-term success.

Rebalancing and Maintaining Diversification

Building a diversified portfolio is the first crucial step, but its effectiveness over the long term hinges on proper maintenance. Markets are dynamic, and without regular attention, even the most thoughtfully constructed portfolio can drift from its intended asset allocation, thereby undermining its diversification benefits. This is where rebalancing comes in.

Why is Rebalancing Crucial?

Over time, the performance of different asset classes will vary. Some assets will grow faster than others, causing their proportion in your portfolio to increase, while underperforming assets will shrink in proportion.

For example, imagine you started with a 60% stock, 40% bond portfolio. If the stock market experiences a strong bull run for several years, your stock allocation might grow to 70% or even 80% of your portfolio, while your bond allocation shrinks. This “drift” means your portfolio is now more aggressive and riskier than you initially intended. Conversely, if bonds outperform, your portfolio might become too conservative, potentially sacrificing growth.

Rebalancing corrects this drift by bringing your portfolio back to its target asset allocation. It ensures that your portfolio’s risk level remains consistent with your risk tolerance and financial goals, maintaining the core benefits of diversification.

How to Rebalance Your Portfolio

There are typically two main ways to rebalance:

- Selling High, Buying Low: This is the classic rebalancing method. You sell portions of the asset classes that have grown above their target weight (effectively selling assets that have performed well) and use the proceeds to buy more of the asset classes that have fallen below their target weight (buying assets that have underperformed). This method not only restores your allocation but also forces you to adhere to the fundamental investing principle of “buy low, sell high.”

- Directing New Contributions: If you’re regularly contributing new

Recommended Resources

Explore Shopify Vs Woocommerce Which Is Better for additional insights.

Check out How To Rebalance Investment Portfolio on Trading Costs for a deeper dive.