Understanding the Traditional IRA: Tax Deferral in Action

The Traditional IRA has long been a cornerstone of retirement planning, primarily appealing to individuals who benefit from an upfront tax deduction. Established in 1974, it represents a classic approach to retirement savings: contribute now, get a potential tax break, and pay taxes later in retirement.

Contribution Mechanics and Deductibility

With a Traditional IRA, contributions are typically made with pre-tax dollars. This means that for many taxpayers, the money they put into a Traditional IRA can be deducted from their taxable income in the year the contribution is made. This immediate tax benefit is a significant draw, effectively lowering your adjusted gross income (AGI) and, consequently, your current year’s tax liability. For 2026, the maximum contribution limit for an IRA is expected to be $7,000, with an additional catch-up contribution of $1,000 for those aged 50 and over, bringing the total to $8,000. These limits apply across both Traditional and Roth IRAs, meaning you can contribute up to this amount collectively, not to each type separately.

However, the deductibility of Traditional IRA contributions isn’t universal. It hinges on several factors, most notably whether you or your spouse are covered by a retirement plan at work (such as a 401(k), 403(b), or pension plan) and your Modified Adjusted Gross Income (MAGI). If neither you nor your spouse is covered by a workplace retirement plan, your contributions are generally 100% deductible, regardless of your income. If you are covered by a workplace plan, the deductibility phases out as your MAGI rises above certain thresholds. For example, for 2026, if you’re covered by a workplace plan, the deduction might begin to phase out at an MAGI of around $79,000 and be completely phased out at $89,000 for single filers. These thresholds are adjusted annually for inflation and can vary significantly for married couples filing jointly or separately.

Even if your contributions aren’t deductible, you can still contribute non-deductible after-tax money to a Traditional IRA. While these contributions don’t offer an upfront tax break, they allow your investments to grow tax-deferred. Keeping meticulous records of these non-deductible contributions is crucial, as they will not be taxed again when withdrawn in retirement, helping to avoid double taxation.

Tax-Deferred Growth

One of the most powerful features of a Traditional IRA is its tax-deferred growth. This means that any investment earnings (dividends, interest, capital gains) within the account are not taxed year-to-year. Instead, taxes are postponed until you begin making withdrawals in retirement. This compounding effect, unhindered by annual taxation, can significantly accelerate the growth of your nest egg over decades. Imagine your investments growing, and those earnings themselves earning returns, without a portion being siphoned off by taxes each year. This deferred taxation allows your money to work harder for you, a principle central to long-term wealth accumulation.

This tax deferral mechanism is particularly beneficial for individuals who anticipate being in a lower tax bracket in retirement than they are during their working years. By deferring taxes, they effectively pay taxes on their withdrawals at a potentially lower rate in the future.

Withdrawals and Required Minimum Distributions (RMDs)

When you reach retirement age, specifically 59½, you can begin taking qualified withdrawals from your Traditional IRA without penalty. These withdrawals, including both your deductible contributions and all accumulated earnings, are taxed as ordinary income in the year they are received. Withdrawals made before age 59½ are generally subject to a 10% early withdrawal penalty, in addition to being taxed as ordinary income, unless an exception applies (e.g., qualified higher education expenses, first-time home purchase up to $10,000, unreimbursed medical expenses).

A distinctive feature of Traditional IRAs is the concept of Required Minimum Distributions (RMDs). The government doesn’t want to defer taxes indefinitely. Therefore, once you reach a certain age (currently 73, though this has shifted and may shift again), you are mandated to begin withdrawing a minimum amount from your Traditional IRA each year. This rule ensures that the IRS eventually collects the deferred taxes. RMDs are calculated based on your account balance at the end of the previous year and your life expectancy, as determined by IRS tables. Failing to take an RMD or taking less than the required amount can result in a significant penalty, typically 25% (or potentially 10% if corrected promptly) of the amount you should have withdrawn.

The RMD rule means that while Traditional IRAs offer tax deferral, they also come with a structured payout schedule in later life, which can sometimes complicate estate planning or how beneficiaries inherit the account.

Understanding the Roth IRA: Tax-Free Growth and Withdrawals

The Roth IRA, introduced in 1997, revolutionized retirement savings by flipping the traditional tax model on its head. Instead of an upfront tax deduction, the Roth IRA offers the compelling promise of tax-free withdrawals in retirement.

Contribution Mechanics and Income Limitations

Unlike Traditional IRAs, contributions to a Roth IRA are made with after-tax dollars. This means there’s no immediate tax deduction for the money you contribute. You pay taxes on your income in the year you earn it, and then you contribute a portion of that already-taxed income to your Roth IRA. The contribution limits for 2026 are the same as for Traditional IRAs: $7,000, with an additional $1,000 catch-up contribution for those aged 50 and over.

A critical aspect of the Roth IRA is its income eligibility. The ability to contribute directly to a Roth IRA is subject to Modified Adjusted Gross Income (MAGI) limits. These limits are designed to restrict direct Roth contributions to middle and upper-middle-income earners. For 2026, for single filers, the ability to contribute directly to a Roth IRA may begin to phase out at an MAGI of approximately $146,000 and be completely phased out at $161,000. For married couples filing jointly, these thresholds are significantly higher. If your MAGI exceeds these limits, you cannot contribute directly to a Roth IRA, although strategies like the “backdoor Roth” allow higher earners to bypass these direct contribution limits.

Despite these income limits, the appeal of the Roth IRA remains strong due to its unparalleled tax benefits in retirement.

Tax-Free Growth and Qualified Withdrawals

The true power of the Roth IRA lies in its tax-free growth and tax-free withdrawals in retirement. Once your after-tax contributions are in the account, all earnings accumulate tax-free. More importantly, when you take qualified withdrawals in retirement, neither your contributions nor your earnings are subject to federal income tax. This means that every dollar you withdraw from a qualified Roth IRA is yours to keep, entirely free of tax.

For withdrawals to be “qualified,” two main conditions must be met:

- You must be at least 59½ years old.

- The Roth IRA must have been open for at least five years (known as the “5-year rule”). This 5-year period begins on January 1st of the year you made your first Roth IRA contribution, regardless of your age.

If both conditions are met, all withdrawals are tax-free and penalty-free. If you need to withdraw contributions before meeting these conditions, your original contributions can generally be withdrawn tax-free and penalty-free at any time, as you’ve already paid taxes on that money. However, withdrawing earnings prematurely (before age 59½ and the 5-year rule is met) will subject those earnings to income tax and a 10% early withdrawal penalty, with exceptions similar to those for Traditional IRAs.

The tax-free nature of Roth withdrawals makes it an incredibly attractive option for those who anticipate being in a higher tax bracket in retirement or who simply want the certainty of knowing their retirement income won’t be eroded by future tax burdens.

No Required Minimum Distributions (RMDs) for the Original Owner

Another significant advantage of the Roth IRA is that the original owner is not subject to Required Minimum Distributions (RMDs) during their lifetime. This offers immense flexibility in managing your retirement income and allows your investments to continue growing tax-free for as long as you wish. This feature is particularly appealing for estate planning. A Roth IRA can be passed on to beneficiaries, who will then be subject to their own RMD rules (though often with more favorable tax treatment than inherited Traditional IRAs), making it an excellent vehicle for How To Build Generational Wealth.

Key Differences: A Side-by-Side Comparison

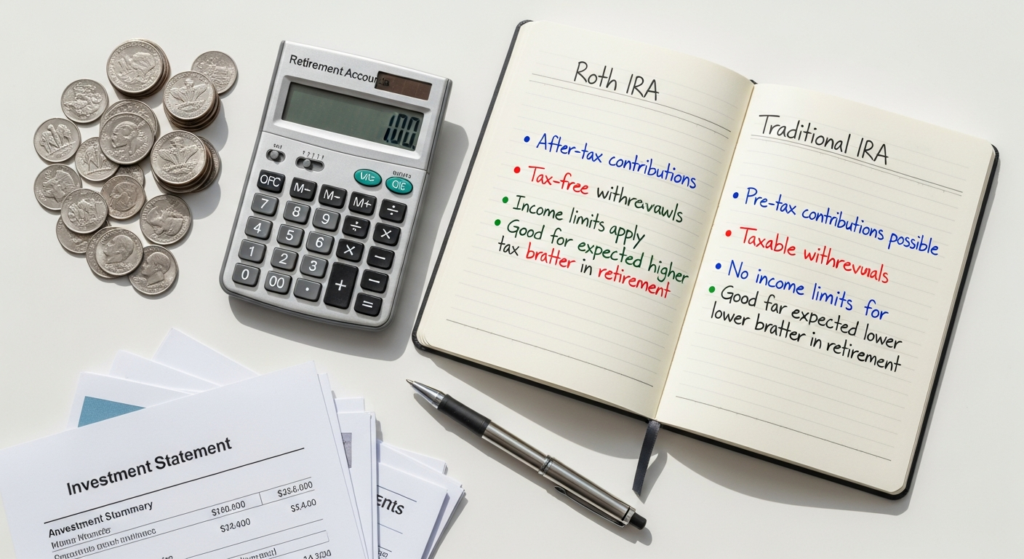

Tax Treatment: Contributions, Growth, and Withdrawals

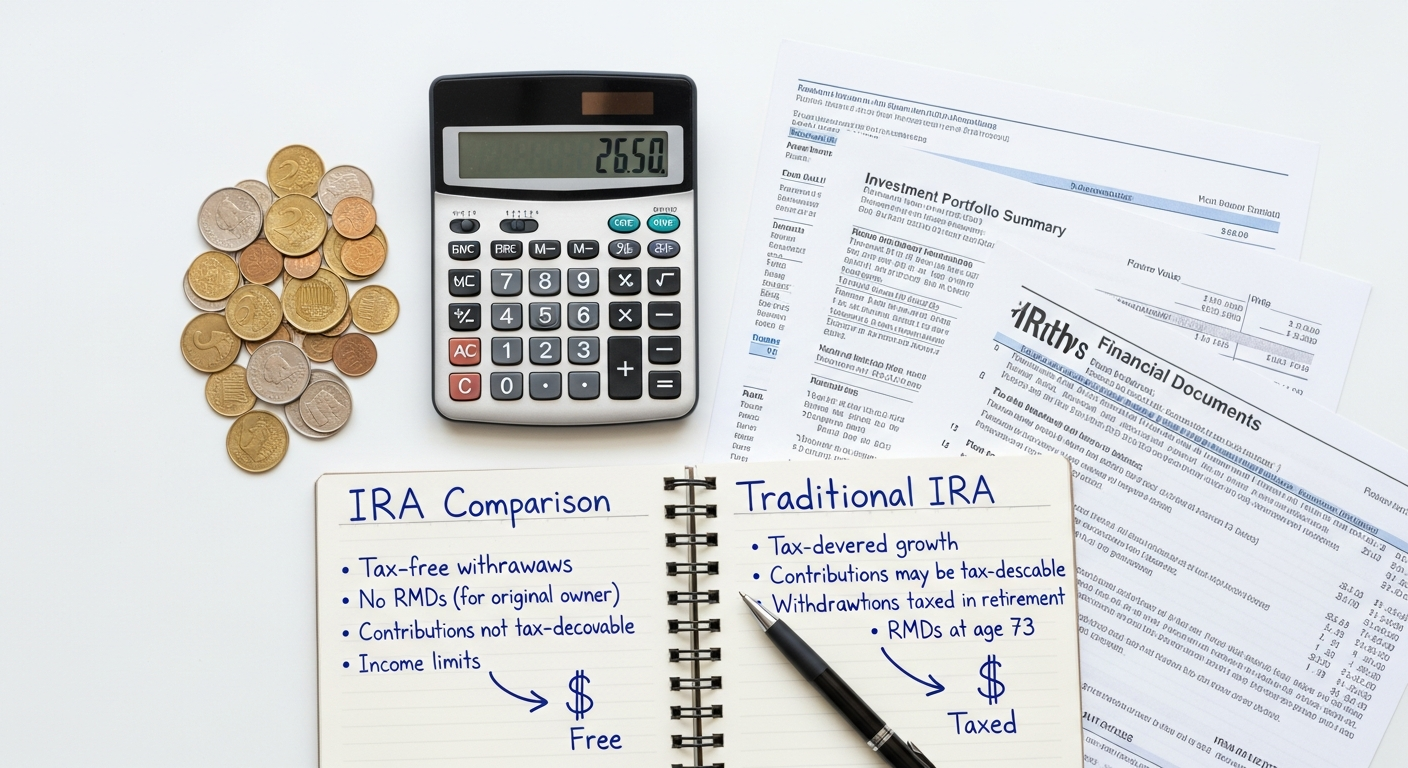

- Traditional IRA:

- Contributions: Potentially tax-deductible in the year they are made, reducing current taxable income.

- Growth: Tax-deferred. Earnings grow tax-free within the account but are taxed upon withdrawal.

- Withdrawals: Taxable as ordinary income in retirement (for deductible contributions and all earnings).

- Roth IRA:

- Contributions: Made with after-tax dollars; no upfront tax deduction.

- Growth: Tax-free. Earnings grow completely tax-free.

- Withdrawals: Tax-free in retirement, provided they are “qualified” (age 59½ and 5-year rule met).

This fundamental difference in tax timing is the bedrock of the Roth vs. Traditional debate. Do you want your tax break now or later?

Eligibility and Income Limits

- Traditional IRA:

- Contribution Eligibility: Anyone with earned income can contribute, regardless of income level.

- Deductibility Limits: Tax deductibility of contributions is subject to MAGI limits if you (or your spouse) are covered by a workplace retirement plan.

- Roth IRA:

- Contribution Eligibility: Direct contributions are subject to MAGI limits. If your income is too high, you cannot contribute directly, though the “backdoor Roth” strategy can be used.

The income restrictions on direct Roth contributions can be a deciding factor for high earners, often pushing them towards a Traditional IRA (potentially non-deductible) or a backdoor Roth strategy.

Required Minimum Distributions (RMDs)

- Traditional IRA: RMDs are mandatory, typically starting at age 73 (subject to change by legislation). Failure to take RMDs results in significant penalties.

- Roth IRA: No RMDs for the original owner. This offers greater flexibility in managing your retirement assets and can be a powerful tool for legacy planning. Beneficiaries of an inherited Roth IRA will have their own RMD rules, but typically receive tax-free withdrawals.

Flexibility and Estate Planning

The absence of RMDs for Roth IRAs provides considerable flexibility. You can allow your money to continue growing tax-free for your entire life, making it an excellent vehicle for wealth transfer. Beneficiaries inherit a tax-free income stream, making the Roth IRA a potent tool for How To Build Generational Wealth. While Traditional IRAs also contribute to generational wealth, beneficiaries will have to pay income tax on withdrawals, making the Roth IRA often more attractive from a beneficiary’s perspective.

Which IRA is Right for You? Strategic Considerations

The choice between a Roth and a Traditional IRA is rarely black and white. It depends heavily on your current financial situation, your future expectations, and your overall financial philosophy. Here are the key factors to consider:

Current vs. Future Tax Brackets

This is perhaps the most significant determinant.

- Choose Traditional IRA if: You expect to be in a lower tax bracket in retirement than you are now. The upfront tax deduction makes sense if you can defer taxes at a higher current rate and pay them at a lower future rate.

- Choose Roth IRA if: You expect to be in a higher tax bracket in retirement than you are now. Paying taxes on your contributions now, at a potentially lower rate, allows your withdrawals to be tax-free when your income (and thus tax bracket) might be higher. This is often the case for younger professionals just starting their careers, who anticipate significant income growth over time.

Consider your career trajectory. Are you just starting out, with income likely to increase substantially? A Roth might be advantageous. Are you in your peak earning years, expecting to scale back or retire to a lower income? A Traditional IRA’s current deduction could be more beneficial.

Income Level and AGI

Your current income plays a crucial role:

- If your MAGI is too high for direct Roth contributions: A Traditional IRA (potentially non-deductible) might be your only direct IRA option. However, the “backdoor Roth” strategy allows high-income earners to contribute to a non-deductible Traditional IRA and then convert it to a Roth, bypassing the direct income limits.

- If you can deduct Traditional IRA contributions: And you are in a high tax bracket, the immediate tax savings can be very attractive.

Age and Retirement Horizon

Younger individuals often benefit more from a Roth IRA. With decades for their money to grow tax-free, the compounding effect can be immense. For those closer to retirement, the immediate tax deduction of a Traditional IRA might be more appealing, especially if their income is currently high and they anticipate a significant drop in income during retirement.

Financial Goals and Flexibility

Consider your broader financial picture.

- Emergency Fund and Flexibility: Roth IRAs offer unique flexibility. You can withdraw your contributions (but not earnings) at any time, tax-free and penalty-free, for any reason. While not recommended as a primary emergency fund, this feature can provide an additional layer of financial security. For individuals just starting their financial journey, balancing saving for retirement with building an emergency fund is crucial. Tools like How To Create A Monthly Budget become indispensable here, allowing you to allocate funds effectively between immediate needs and long-term goals like IRA contributions.

- Debt Payoff: If you have high-interest debt, prioritizing debt repayment might be more beneficial than maximizing IRA contributions initially. Once that debt is under control, the funds freed up can be aggressively channeled into your chosen IRA. Understanding methods like the Snowball Vs Avalanche Debt Payoff Method can accelerate this process, clearing the path for robust retirement savings.

- First-Time Home Purchase: Both IRAs allow penalty-free withdrawals of up to $10,000 for a first-time home purchase, but with different tax implications. With a Roth, this withdrawal could be entirely tax-free if certain conditions (including the 5-year rule) are met.

Beyond the Basics: Advanced Strategies & Hybrid Approaches

For many, the choice isn’t necessarily one or the other. A diversified approach, or utilizing advanced strategies, can further optimize your retirement plan.

The Backdoor Roth Strategy

As mentioned, direct contributions to a Roth IRA are phased out at higher income levels. The backdoor Roth strategy allows high-income earners to effectively bypass these limits. It involves contributing non-deductible after-tax money to a Traditional IRA and then immediately converting that Traditional IRA balance to a Roth IRA. If you have no other pre-tax Traditional IRA balances, this conversion is generally tax-free. This strategy is perfectly legal and a common tactic for those who want the benefits of a Roth IRA but are otherwise ineligible.

Roth Conversions

Even if you’ve primarily contributed to a Traditional IRA throughout your career, you can convert some or all of your Traditional IRA balance into a Roth IRA. This is known as a Roth conversion. The catch is that any pre-tax money you convert (deductible contributions and all earnings) will be subject to income tax in the year of conversion. This strategy can be advantageous if you anticipate future tax rates will be significantly higher, or if you want to eliminate future RMDs and create a tax-free inheritance for beneficiaries. Strategic Roth conversions can also be planned during years when you anticipate being in a lower tax bracket (e.g., during a sabbatical, early retirement, or a year with significant tax deductions).

Having Both Traditional and Roth IRAs

It’s not uncommon, or even unwise, to have both a Traditional and a Roth IRA. This creates a “tax diversification” strategy. By holding assets in both pre-tax (Traditional) and after-tax (Roth) accounts, you give yourself flexibility in retirement. When you need income, you can choose to draw from the account that offers the most favorable tax treatment given your income level and the prevailing tax laws at that time. This hybrid approach allows you to hedge against uncertainty regarding future tax rates, providing more control over your taxable income in retirement.

For example, if you need to keep your income low in a particular retirement year to qualify for certain deductions or subsidies, you might draw more heavily from your Roth IRA. Conversely, if you’re in a very low tax bracket due to other circumstances, drawing from a Traditional IRA might be more efficient. This proactive management of your retirement income streams is a hallmark of sophisticated financial planning.

Conclusion

The choice between a Roth IRA and a Traditional IRA is a cornerstone of effective retirement planning, with each offering distinct advantages based on your tax situation, income level, and long-term financial goals. The Traditional IRA appeals with its immediate tax deductions and tax-deferred growth, ideal for those who anticipate being in a lower tax bracket in retirement. In contrast, the Roth IRA, funded with after-tax dollars, promises completely tax-free growth and withdrawals in retirement, a powerful draw for individuals who expect higher future tax rates or desire greater flexibility and a tax-free legacy. Understanding the nuances of contribution limits for 2026, income eligibility, RMDs, and the strategic implications of each account type is paramount.

Ultimately, the “best” choice is the one that aligns most closely with your personal financial forecast and objectives. Whether you opt for one exclusively, strategically combine both, or utilize advanced tactics like backdoor Roth conversions, making an informed decision is vital. Remember that your financial situation is dynamic; what’s suitable today may evolve tomorrow. Regularly review your retirement strategy, just as you would review your How To Create A Monthly Budget or debt payoff plan, to ensure it continues to serve your best interests. By carefully weighing the Roth IRA vs. Traditional IRA differences, you empower yourself to build a robust and tax-efficient foundation for a secure and prosperous retirement.

Frequently Asked Questions

Can I contribute to both a Roth and a Traditional IRA in the same year?▾

What happens if my income is too high to contribute to a Roth IRA?▾

Are there any exceptions to the 10% early withdrawal penalty for IRAs?▾

How does the 5-year rule for Roth IRAs work?▾

Which IRA is better for building generational wealth?▾

Should I consider my employer’s 401(k) or 403(b) plan before contributing to an IRA?▾

Recommended Resources

Learn more about this topic in Ai Writing Tools For Content Marketing at Page Release.

Learn more about this topic in Best Ecommerce Platforms Comparison 2026 at E-ComProfits.