What Exactly Are Sinking Funds? Dispelling the Myths

At its core, a sinking fund is a dedicated savings account or designated pool of money set aside specifically for a known, future expense. Unlike an emergency fund, which is reserved for unforeseen events like job loss or medical emergencies, a sinking fund anticipates costs you know are coming, even if their exact timing or amount might vary slightly. Think of it as pre-paying for your future self, ensuring that when the expense inevitably arrives, the money is already there, waiting.

The concept is deceptively simple but profoundly impactful. Instead of facing a large bill for, say, car insurance, holiday gifts, or a home repair with dread and the potential need to dip into savings or, worse, incur debt, a sinking fund allows you to systematically save smaller amounts over time. This proactive approach smooths out your cash flow, eliminates financial surprises, and significantly reduces stress.

Let’s clarify some common misconceptions:

- Sinking Fund vs. Emergency Fund: While both are savings, their purposes differ. An emergency fund is your financial safety net for the unexpected (e.g., job loss, medical emergency). A sinking fund is for planned, irregular expenses (e.g., car repairs, annual subscriptions, vacations). You need both.

- Sinking Fund vs. General Savings: A general savings account might lump everything together, making it hard to track progress towards specific goals. Sinking funds are highly targeted, giving each dollar a purpose and making saving feel more tangible and motivating.

- Sinking Fund vs. Debt Repayment: While some people might use a sinking fund to save for a down payment to avoid future debt, the primary goal isn’t necessarily debt repayment itself, but rather preventing new debt from forming due to unexpected or irregular expenses.

By embracing sinking funds, you transition from a reactive financial posture to a proactive one. You’re no longer scrambling when the car needs new tires or when holiday season approaches; instead, you’re calmly allocating funds you’ve already set aside. This fundamental shift is a powerful step towards true financial mastery.

The Core Benefits of Integrating Sinking Funds into Your Financial Strategy

Incorporating sinking funds into your personal finance framework isn’t just about managing money; it’s about fundamentally altering your relationship with it. The benefits extend far beyond simply having cash available for a specific expense. They touch upon every aspect of your financial health and overall well-being.

Here are the core advantages:

- Prevents Debt Accumulation: This is arguably the most significant benefit. Many people fall into credit card debt not from extravagant spending, but from unexpected large expenses they weren’t prepared for. A broken appliance, an annual car registration, or a significant dental bill can quickly lead to high-interest debt if a dedicated fund isn’t in place. Sinking funds act as a powerful preventative measure, allowing you to pay cash for these items and avoid the debt trap entirely.

- Reduces Financial Stress and Anxiety: Imagine the peace of mind knowing that when your property taxes are due, or when it’s time for that much-needed family vacation, the money is already there. The constant worry about where funds will come from for irregular expenses is a major source of financial stress. Sinking funds eliminate this anxiety, replacing it with a sense of control and calm.

- Empowers Goal Achievement: Whether your goal is a new car, a home renovation, or a dream trip, sinking funds provide a clear, structured path to get there. By breaking down large goals into smaller, manageable monthly contributions, they make intimidating financial targets feel achievable. This structured saving mechanism fuels motivation and keeps you on track.

- Improves Budgeting Accuracy and Effectiveness: Sinking funds force you to consider and plan for expenses that often get overlooked in a standard monthly budget. When you learn How To Create A Monthly Budget, you typically account for fixed monthly costs like rent and utilities, and variable costs like groceries. Sinking funds add another layer of sophistication, ensuring that annual, quarterly, or irregular expenses are also properly accounted for, leading to a much more realistic and robust budget. This holistic view prevents budget blowouts when those irregular bills arrive.

- Enhances Financial Discipline and Awareness: The act of consistently contributing to specific funds builds financial discipline. It encourages you to think proactively about your spending and saving habits. You become more aware of where your money is going and where it needs to go, fostering a deeper understanding of your financial landscape.

- Allows for Strategic Purchases and Better Deals: By saving up for larger purchases, you put yourself in a position to pay cash, often enabling you to negotiate better prices or avoid interest charges. Instead of rushing a purchase with credit, you can wait for sales or the opportune moment, maximizing the value of your money.

Embracing sinking funds is a strategic decision that pays dividends in both tangible savings and invaluable peace of mind. It’s a testament to the power of planning and consistency in personal finance.

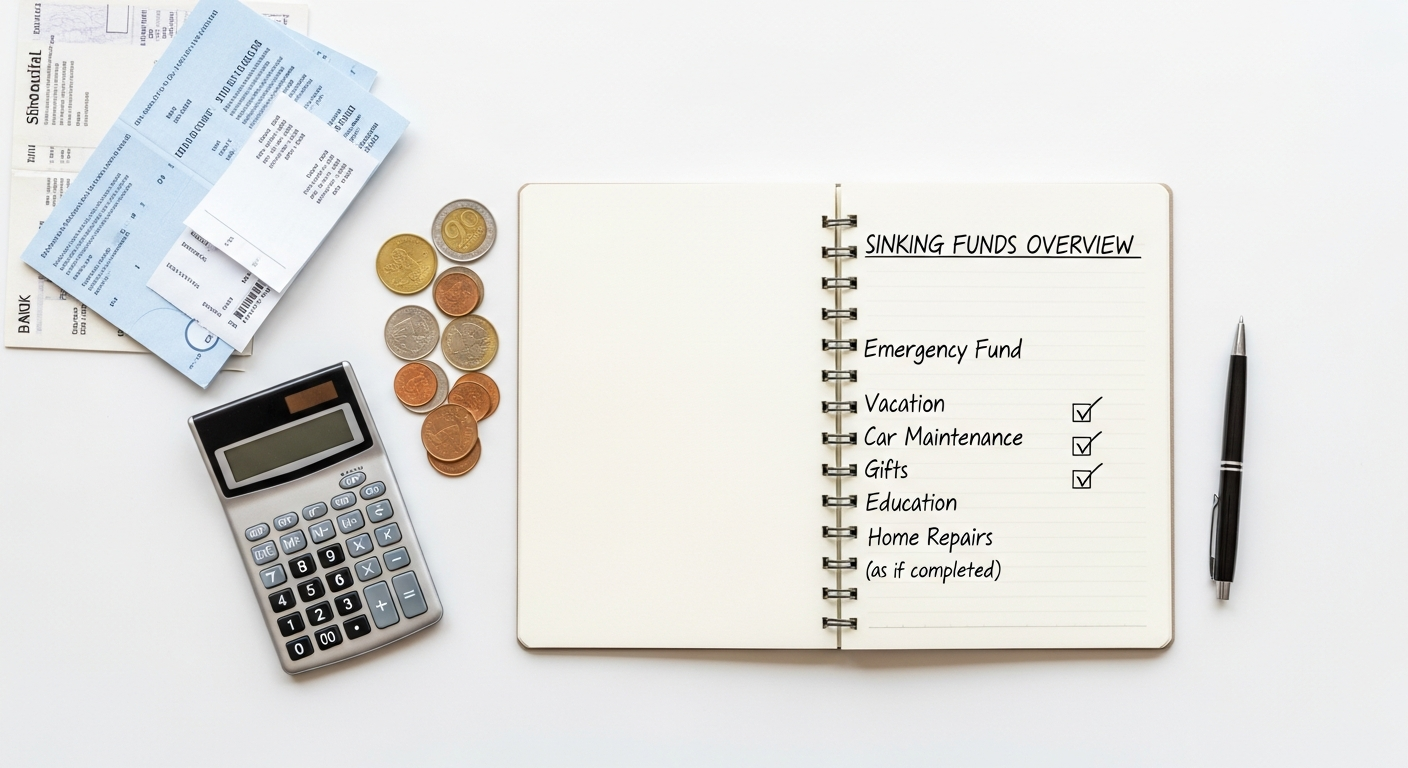

Identifying Your Sinking Fund Needs: Common Categories and Examples

To begin, sit down with your past bank statements, calendars, and a clear mind. Look back over the last 12-24 months and note down every expense that wasn’t a regular monthly bill. Think about what’s coming up in 2026. This audit will reveal many of your recurring irregular expenses.

Here are common categories and examples to get you started:

1. Seasonal and Annual Expenses

These are expenses that occur once or twice a year but can be substantial.

- Holidays/Gifts: Christmas, birthdays, anniversaries, Mother’s/Father’s Day. The average household spends hundreds, if not thousands, on gifts annually.

- Vacations/Travel: A highly anticipated trip requires significant savings for flights, accommodation, activities, and spending money.

- Annual Insurance Premiums: Car insurance, homeowner’s/renter’s insurance, life insurance often offer discounts for annual lump-sum payments.

- Property Taxes: If not escrowed with your mortgage, these can be a large annual or semi-annual bill.

- Vehicle Registration & Inspection: Mandatory annual costs for car owners.

- Memberships & Subscriptions: Annual fees for gyms, professional organizations, software, streaming services, or club memberships.

- Back-to-School/College: Supplies, tuition fees, textbooks, new clothes for students.

- Pet Care: Annual vet check-ups, vaccinations, licensing fees.

2. Irregular and Maintenance Expenses

These are expenses that are harder to predict but are inevitable for homeowners and vehicle owners.

- Car Maintenance & Repairs: Oil changes, tire rotations, unexpected repairs (brakes, battery, etc.). Even with a new car, maintenance is a fact of life.

- Home Maintenance & Repairs: Roof repairs, appliance replacements (dishwasher, fridge), HVAC servicing, plumbing issues, exterior painting, lawn care equipment.

- Medical/Dental Deductibles: If you have a high-deductible health plan, you’ll need to cover a certain amount before insurance kicks in. This includes routine dental cleanings, eye exams, and potential procedures.

- Personal Care: Regular hair appointments, massages, or other routine self-care services that aren’t monthly but still occur periodically.

3. Planned Purchases and Investments

These are larger, often aspirational, purchases that require significant upfront capital.

- New Appliance Fund: Saving for a new washer, dryer, refrigerator, or oven before your old one completely breaks down.

- New Car Down Payment: Instead of taking out a massive loan, saving a substantial down payment reduces your loan amount and monthly payments.

- Home Down Payment: A substantial sinking fund for this purpose is crucial for aspiring homeowners.

- Furniture Replacement: Saving for that new sofa or dining set you’ve been eyeing.

- Technology Upgrades: A new laptop, smartphone, or gaming console every few years.

- Professional Development/Education: Courses, certifications, conferences, or even saving for a future degree.

By categorizing your expenses this way, you gain clarity and can prioritize which sinking funds are most critical for your financial stability and future goals. Remember, you don’t have to create a fund for every single item at once. Start with the most impactful and common ones, then gradually expand as your financial capacity grows.

How to Calculate and Allocate for Your Sinking Funds

Once you’ve identified your sinking fund needs, the next critical step is to determine how much you need to save for each and how to integrate these contributions into your existing budget. This process requires a bit of research and mathematical calculation, but it’s straightforward and incredibly empowering.

Step 1: Estimate the Total Cost for Each Expense

For each sinking fund category you’ve identified, estimate the total cost of the expense.

- For known costs: Use exact figures. For instance, if your annual car insurance premium is $1,200, that’s your target. If your property taxes are $3,000, that’s the number.

-

For variable or irregular costs: Do some research.

- Past expenses: Look at old receipts or bank statements. How much did you spend on holiday gifts last year? How much was that car repair?

- Online research: What’s the average cost of a major appliance repair in your area? How much does a typical vacation to your desired destination cost?

- Get quotes: For larger planned purchases like a new roof or a significant home renovation, get a few estimates.

- Pad your estimates: It’s always better to slightly overestimate than underestimate. Add a 10-15% buffer, especially for repairs or large purchases.

Example: You want to save for a family vacation in 2026. You estimate flights at $1,000, accommodation at $1,500, activities at $500, and spending money at $1,000. Total estimated cost: $4,000.

Step 2: Determine the Timeline

For each expense, identify when you’ll need the money.

- Fixed dates: Your car insurance is due in June. Property taxes in December.

- Target dates: You want to go on vacation in August 2026. You plan to buy a new laptop by October 2026.

- Ongoing: For things like car repairs or home maintenance, you might save perpetually, aiming for a consistent balance in the fund.

Example: For the $4,000 vacation, you want to leave in August 2026. Assuming it’s currently January 2026, you have 8 months to save.

Step 3: Calculate the Monthly Contribution

Divide the total estimated cost by the number of months until you need the money.

Monthly Contribution = Total Estimated Cost / Number of Months

Repeat this calculation for every single sinking fund you intend to create.

Step 4: Integrate into Your Monthly Budget

This is where the rubber meets the road. Once you have your monthly contribution amounts for all your sinking funds, these figures become non-negotiable line items in your monthly budget.

- Prioritize: If your budget is tight, you might not be able to fund every single item initially. Prioritize the most critical funds first (e.g., car repairs, medical deductibles, annual insurance) before moving to aspirational ones (e.g., vacation, new gadgets).

-

Find the money: If your calculations show you need to save $X for sinking funds each month but your current budget doesn’t allow for it, you have two options:

- Increase income: Look for ways to earn more.

- Decrease expenses: Review your current spending. Can you cut back on dining out, entertainment, or unnecessary subscriptions? This is where strategies like learning How To Negotiate Bills And Lower Expenses can be incredibly valuable, freeing up cash flow that can then be redirected into your sinking funds. Every dollar saved on recurring bills can be a dollar put towards future financial stability.

- Adjust as needed: Life happens. If an expense comes in higher or lower than expected, or if your timeline changes, adjust your future contributions accordingly. Sinking funds should be flexible enough to adapt to your changing financial landscape.

By systematically calculating and allocating funds, you transform vague financial goals into concrete, actionable steps within your budget. This methodical approach ensures you’re prepared for whatever 2026 throws your way.

Setting Up Your Sinking Funds: Practical Implementation Strategies

Calculating your sinking fund contributions is a crucial first step, but the real magic happens in the implementation. How you set up and manage these funds can significantly impact your success. The goal is to make the process as seamless, automatic, and transparent as possible.

1. Where to Keep Your Sinking Fund Money

The physical location of your sinking fund money is important for both psychological and practical reasons.

- Separate Savings Accounts (Digital Envelopes): This is arguably the most recommended strategy. Open multiple savings accounts, ideally with an online-only bank that offers high-yield savings rates and allows for easy creation of sub-accounts or “buckets.” Label each account clearly (e.g., “Vacation Fund,” “Car Repair Fund,” “Home Maintenance Fund”). This provides clear separation from your checking account and your emergency fund, making it less tempting to dip into them for non-designated purposes. Many modern banks offer this “digital envelope” feature without needing to open entirely separate accounts, making management simple.

- High-Yield Savings Accounts (HYSA): Regardless of how many accounts you open, ensure they are in a high-yield savings account. While sinking funds are for shorter-term goals than long-term investments, every little bit of interest earned helps your money grow, even if minimally.

- Budgeting Apps: Some budgeting apps (like YNAB, Mint, Personal Capital) allow you to “virtually” earmark money within a single account for different purposes. While the money might physically reside in one savings account, the app helps you track how much is allocated to each sinking fund. This works well for those who prefer fewer actual bank accounts.

- Avoid Your Checking Account: Keeping sinking fund money in your checking account makes it too easy to accidentally spend it. Separate it to maintain discipline.

2. Automate Your Contributions

Automation is the cornerstone of successful sinking fund management. Set it and forget it.

- Scheduled Transfers: Set up automatic recurring transfers from your checking account to your designated sinking fund savings accounts. Schedule these transfers to coincide with your paydays (e.g., bi-weekly or monthly).

- Consistency is Key: Even if you start with small amounts, consistent contributions will build up over time. Automation ensures you never “forget” to save.

- Adjust as Income Changes: If you get a raise or a bonus, consider increasing your automated contributions to accelerate your goals or create new funds.

3. Tracking and Monitoring Your Progress

Regularly checking in on your sinking funds keeps you motivated and informed.

- Budgeting Spreadsheets: A simple spreadsheet can list each fund, its target amount, current balance, and monthly contribution. This gives you a clear overview.

- Budgeting Apps: As mentioned, many apps are excellent for tracking balances and visualizing progress toward your sinking fund goals.

- Bank Statements: Review your separate savings account balances periodically to ensure transfers are happening correctly and balances are growing as expected.

4. Review and Adjust Regularly

Your financial life isn’t static, and neither should your sinking funds be.

-

Monthly/Quarterly Check-ins: As part of your regular budget review, take a look at your sinking funds.

- Are your estimates still accurate for upcoming expenses?

- Have any new irregular expenses popped up that need a fund?

- Have you achieved a goal and now need to redirect those contributions?

- Do you need to increase or decrease contributions based on changes in income or expense estimates?

- Be Flexible: If you face an unexpected financial crunch, you might need to temporarily pause or reduce contributions to certain sinking funds. The key is to be intentional about these changes and resume contributions as soon as possible.

- Celebrate Wins: When you successfully use a sinking fund to pay for a planned expense without stress or debt, acknowledge that achievement! It reinforces positive financial habits.

By putting these practical strategies into play, you transform the theoretical concept of sinking funds into a tangible, working system that actively supports your financial goals and reduces stress.

Sinking Funds as a Catalyst for Long-Term Financial Growth and Wealth Building

While the immediate benefits of sinking funds—preventing debt, reducing stress, and enabling planned purchases—are clear, their strategic importance extends much further. Sinking funds are not just about managing day-to-day expenses; they are a powerful, often overlooked, catalyst for long-term financial growth and the ambitious goal of How To Build Generational Wealth.

Preventing Wealth Erosion

One of the greatest threats to wealth accumulation is financial setbacks that force you to raid your investments or incur high-interest debt. When an unexpected car repair or a hefty annual insurance premium hits, without a dedicated sinking fund, people often resort to:

- Credit Card Debt: High-interest credit card debt quickly erodes wealth through interest payments, diverting money that could have been invested.

- Dipping into Emergency Funds: While emergency funds are for emergencies, misusing them for predictable irregular expenses means they aren’t fully funded when a true emergency strikes, potentially leading to debt or asset sales.

- Selling Investments: Liquidating investments prematurely can trigger capital gains taxes and means missing out on potential future growth.

Sinking funds act as a protective barrier, shielding your existing wealth and investments from these common pitfalls. By ring-fencing funds for known expenses, you keep your emergency fund intact, your credit card balances low, and your investment portfolio growing undisturbed. This stability is foundational for building wealth over time.

Freeing Up Capital for Strategic Investments

When you’re consistently prepared for irregular expenses, you free up mental and financial bandwidth. The money that would otherwise be held in reserve for “what if” scenarios (that are actually “when” scenarios) or spent on interest payments can be purposefully directed towards wealth-building avenues:

- Increased Investment Contributions: With your day-to-day and irregular expenses smoothly managed, you have more disposable income to contribute to your retirement accounts (401k, IRA), brokerage accounts, or other investment vehicles. Consistent, long-term investing is the bedrock of wealth creation.

- Accelerated Debt Repayment: Beyond preventing new debt, sinking funds can free up cash flow to aggressively pay down existing high-interest debts, such as student loans or mortgages, thereby saving you thousands in interest over the long run. The money saved on interest can then be redirected into investments.

- Funding for Large, Wealth-Generating Purchases: Sinking funds can be used to save for significant down payments on assets that appreciate, like real estate. A larger down payment reduces loan interest, builds equity faster, and improves your financial leverage. Similarly, saving for an education or professional certification through a sinking fund can significantly boost your earning potential, which is a direct pathway to greater wealth.

Building Generational Wealth Through Financial Prudence

The disciplined approach fostered by sinking funds is directly relevant to building generational wealth. Generational wealth isn’t just about passing down a large sum of money; it’s also about instilling financial literacy, stability, and good habits.

- Setting a Strong Example: By demonstrating meticulous financial planning and debt avoidance through sinking funds, you teach future generations invaluable lessons in money management.

- Creating a Stable Foundation: A family whose finances are stable, free from the constant burden of unexpected bills and high-interest debt, is better positioned to save, invest, and make strategic financial decisions for the long term. This stability reduces the likelihood of financial crises that can deplete inherited wealth or prevent its accumulation.

- Enabling Strategic Asset Acquisition: By consistently saving for large purchases (e.g., real estate, business investments), sinking funds facilitate the acquisition of assets that can be passed down or used to generate income for future generations.

- Reducing Financial Burden on Heirs: A well-managed financial life, supported by sinking funds, means less financial stress and fewer unexpected burdens (like neglected home repairs or outstanding large bills) for your heirs to contend with. This allows them to focus on growing the wealth rather than repairing past financial oversights.

In essence, sinking funds provide the essential financial stability and predictability that allow individuals and families to look beyond immediate needs and focus on the bigger picture of sustained financial growth and the legacy they wish to build for future generations. They are a testament to the power of small, consistent actions leading to monumental long-term results.

Advanced Sinking Fund Tactics and Common Pitfalls to Avoid

Once you’ve mastered the basics of setting up and managing sinking funds, there are several advanced tactics you can employ to optimize their effectiveness. Equally important is being aware of common pitfalls that can undermine your efforts.

Advanced Sinking Fund Tactics

1. Prioritizing When Funds Are Tight

It’s common to feel overwhelmed by the number of potential sinking funds. If your budget can’t accommodate all your desired contributions, prioritize:

- Needs Over Wants: Focus on essential, non-negotiable expenses first (e.g., annual insurance, car maintenance, medical deductibles) before saving for aspirational items like vacations or new gadgets.

- Imminent Over Distant: Fund expenses that are coming up sooner. If your car registration is due in 3 months and a new appliance is a year away, prioritize the registration.

- Highest Impact: Which expenses, if not funded, would cause the most financial distress or lead to debt? Prioritize those.

2. Creating a “Buffer” or “Overflow” Fund

For highly unpredictable irregular expenses (e.g., general home repairs, appliance failures), consider a single “Buffer” or “General Irregular Expense” fund. Instead of having a separate fund for every single possible repair, this fund acts as a catch-all. When a specific large repair occurs, you can then refill the general fund. This simplifies management.

3. The “Roll-Over” Strategy

What happens if you oversave for a specific fund (e.g., vacation cost less than expected) or if an expense doesn’t occur (e.g., no major car repairs that year)? Don’t just absorb it into your checking account. Consider:

- Rolling it into the next year’s fund: If you oversaved for holiday gifts, let the surplus roll over to next year’s holiday fund.

- Reallocating to a higher-priority fund: If your car repair fund has a surplus, consider moving it to another fund that’s struggling or to a long-term savings goal.

- Boosting your emergency fund or investments: A surplus is always an opportunity to strengthen your overall financial position.

4. Using Windfalls Strategically

Bonuses, tax refunds, or unexpected gifts are excellent opportunities to supercharge your sinking funds. Instead of treating them as free money to spend, allocate a portion (or all) to top up your sinking funds, especially for larger, long-term goals. This can significantly accelerate your progress.

Common Pitfalls to Avoid

1. Underestimating Costs or Overestimating Income

This is a frequent mistake. Be realistic and even slightly conservative when estimating expenses. Similarly, don’t allocate more to sinking funds than your actual disposable income allows after all other essential bills are paid. An unrealistic budget is doomed to fail.

2. Not Automating Contributions

Relying on manual transfers is a recipe for inconsistency. Life gets busy, and it’s easy to forget or procrastinate. Automation is your best friend for sinking funds.

3. Mixing Sinking Funds with Emergency Funds

While both are savings, their distinct purposes need distinct funding. Using your emergency fund for a planned expense means it’s not fully available for a true emergency, defeating its purpose. Keep them separate.

4. Neglecting Regular Review and Adjustment

Setting up sinking funds isn’t a one-and-done task. Your life, expenses, and goals change. If you don’t review and adjust your funds quarterly or annually, they will quickly become outdated and ineffective.

5. Getting Too Granular (Analysis Paralysis)

While it’s good to be specific, creating a sinking fund for every single minor expense can become overwhelming. Start with the big, impactful categories and consolidate smaller, similar expenses into broader funds if it helps simplify management. The goal is clarity and control, not excessive complexity.

6. Feeling Guilty About Using the Funds

These funds are meant to be spent! When the expense arrives, use the money you’ve diligently saved. Don’t feel guilty. That’s the whole point. Celebrate the fact that you were prepared and avoided stress or debt.

By understanding and avoiding these common missteps, you can ensure your sinking fund strategy remains robust, effective, and truly serves its purpose in your financial journey through 2026 and beyond.

Frequently Asked Questions

Recommended Resources

Related reading: How To Do A Content Audit (Page Release).

Learn more about this topic in Dividend Investing Strategy Guide at Trading Costs.