Understanding the Debt Landscape: Why a Strategic Payoff Matters

Debt is an omnipresent feature of modern economies, ranging from manageable mortgages and student loans to more challenging credit card balances and personal loans. While some forms of debt, like a mortgage on an appreciating asset, can be considered “good debt” in certain contexts, high-interest consumer debt almost universally acts as a drag on personal wealth. Every dollar spent on interest payments is a dollar that cannot be saved, invested, or used to enhance your quality of life.

The sheer volume and variety of debts can be overwhelming. Many individuals find themselves juggling multiple creditors, varying interest rates, and different payment due dates. Without a clear, systematic approach, it’s easy to feel stuck in a perpetual cycle of minimum payments, watching interest accrue month after month. This is precisely why a strategic debt payoff method is not just beneficial, but essential. A well-defined strategy provides a roadmap, fosters discipline, and, most importantly, offers a tangible path to liberation from financial obligations.

A strategic approach goes beyond simply making payments; it involves actively managing your finances to optimize your debt reduction efforts. This means understanding your current financial position, identifying areas where you can free up extra cash, and committing to a consistent plan. Ignoring debt or only making minimum payments is akin to trying to bail out a leaky boat with a teacup – progress will be slow, if not non-existent, and the effort will feel Sisyphean. By embracing a structured method like the debt snowball or debt avalanche, you transform a daunting task into a series of achievable steps, building momentum and confidence along the way.

Before diving into the specifics of each method, it’s vital to have a clear picture of your entire financial landscape. This includes listing all your debts, their outstanding balances, interest rates, and minimum monthly payments. This foundational step is critical for deciding which strategy will serve you best and for creating a realistic timeline for your debt-free journey. Remember, the goal isn’t just to pay off debt, but to do so efficiently and sustainably, paving the way for a more secure financial future by 2026 and beyond.

The Debt Snowball Method: Building Momentum Through Small Wins

The debt snowball method is a debt reduction strategy that prioritizes psychological motivation over mathematical efficiency. It’s particularly appealing to individuals who thrive on seeing quick results and need consistent encouragement to stay committed to their financial goals. Developed and popularized by financial experts, this method focuses on paying off debts from the smallest balance to the largest, regardless of their interest rates.

How the Debt Snowball Method Works:

- List All Your Debts: Start by listing every single debt you have, from credit cards and personal loans to student loans and medical bills.

- Order by Smallest Balance: Arrange these debts from the smallest outstanding balance to the largest. Ignore the interest rates for this step.

- Make Minimum Payments on All But One: Continue to make the minimum required payments on all your debts except for the one with the smallest balance.

- Attack the Smallest Debt: Direct every extra dollar you can find towards paying off that smallest debt. This means any money you save from negotiating bills and lowering expenses, any bonuses, or any discretionary funds should go directly to this debt.

- Roll Over Payments: Once the smallest debt is completely paid off, you take the money you were paying on that debt (both the minimum payment and the extra amount) and add it to the minimum payment of the next smallest debt. This creates a “snowball” effect, where your payments on subsequent debts grow larger and larger.

- Repeat: Continue this process, tackling the next smallest debt with the accumulated payment amount until all your debts are paid off.

Example:

Let’s say you have four debts:

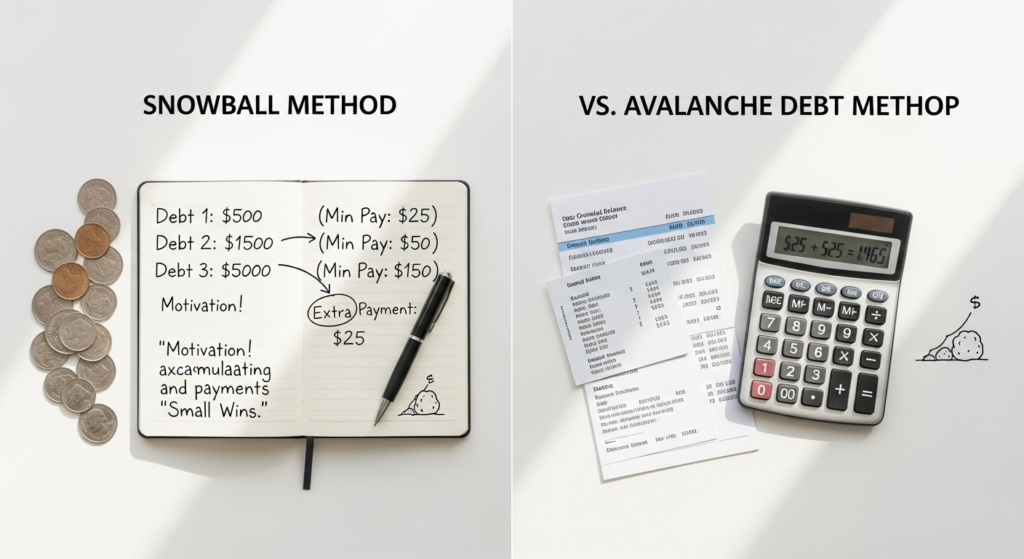

- Credit Card A: $500 balance, 20% APR, $25 minimum payment

- Personal Loan B: $2,000 balance, 10% APR, $50 minimum payment

- Credit Card C: $3,000 balance, 18% APR, $75 minimum payment

- Student Loan D: $10,000 balance, 6% APR, $100 minimum payment

Using the debt snowball, you’d order them: Credit Card A ($500), Personal Loan B ($2,000), Credit Card C ($3,000), Student Loan D ($10,000).

Advantages of the Debt Snowball:

- Psychological Boost: The primary benefit is the rapid succession of small wins. Paying off the first few debts quickly provides immense motivation and a feeling of accomplishment, making it easier to stick with the plan.

- Simplicity: It’s straightforward to understand and implement, requiring less complex calculations than the avalanche method.

- Increased Adherence: For those who might feel overwhelmed by a long-term, slow-burn strategy, the snowball method offers immediate gratification that can prevent burnout and ensure sustained effort.

Disadvantages:

- Higher Overall Cost: Because it doesn’t prioritize high-interest debts, you will likely pay more in total interest over the life of your debt.

- Mathematically Less Efficient: From a purely financial perspective, it’s not the cheapest way to pay off debt.

The debt snowball method is ideal for individuals who need that emotional push, those who have struggled with debt payoff in the past, or anyone who finds the idea of chipping away at a mathematically optimal but emotionally taxing plan too daunting. The feeling of success can be a powerful motivator, often outweighing the slightly higher interest paid for many people.

The Debt Avalanche Method: Maximizing Financial Efficiency Through Interest Savings

In stark contrast to the debt snowball, the debt avalanche method is a purely mathematical approach designed to save you the most money on interest. This strategy prioritizes efficiency, making it the preferred choice for those who are driven by logic, numbers, and the desire to minimize their overall debt cost. It focuses on tackling debts with the highest interest rates first, regardless of their balance.

How the Debt Avalanche Method Works:

- List All Your Debts: Just like with the snowball method, compile a comprehensive list of all your debts.

- Order by Highest Interest Rate: This is the critical difference. Arrange your debts from the highest annual percentage rate (APR) to the lowest. The balance of the debt is secondary in this ordering.

- Make Minimum Payments on All But One: Pay the minimum required amount on all your debts, except for the one with the highest interest rate.

- Attack the Highest Interest Debt: Dedicate any extra funds you have available – money saved through smart budgeting, extra income, or reduced expenses – to the debt with the highest interest rate.

- Roll Over Payments: Once the highest interest rate debt is completely paid off, you take the money you were paying on that debt (both the minimum payment and the extra amount) and add it to the minimum payment of the next debt on your list (which will be the one with the next highest interest rate).

- Repeat: Continue this process, systematically eliminating debts based on their interest rates until you are entirely debt-free.

Example:

Using the same four debts from the previous example:

- Credit Card A: $500 balance, 20% APR, $25 minimum payment

- Personal Loan B: $2,000 balance, 10% APR, $50 minimum payment

- Credit Card C: $3,000 balance, 18% APR, $75 minimum payment

- Student Loan D: $10,000 balance, 6% APR, $100 minimum payment

Using the debt avalanche, you’d order them by APR: Credit Card A (20%), Credit Card C (18%), Personal Loan B (10%), Student Loan D (6%).

Once Credit Card A is paid off, you take that $125 and add it to the minimum payment of Credit Card C. So, Credit Card C now receives $75 (minimum) + $125 = $200 per month. This continues until all debts are eliminated.

Advantages of the Debt Avalanche:

- Maximum Interest Savings: This is the most financially efficient method. By eliminating high-interest debts first, you reduce the total amount of interest paid over the life of your debt, saving you significant money.

- Faster Debt Freedom (Potentially): Because you’re saving on interest, more of your payments go towards the principal, which can lead to a faster overall debt payoff in terms of total time, assuming you stick with the plan.

- Logical & Objective: Appeals to those who prefer a data-driven approach to financial management.

Disadvantages:

- Slower Initial Gratification: If your highest interest debt also happens to be a large balance, it might take a considerable amount of time before you pay off your first debt. This lack of immediate “wins” can be demotivating for some individuals.

- Requires Discipline: Because the psychological boosts are less frequent, it demands a strong commitment and consistent discipline to see the strategy through.

The debt avalanche method is ideal for individuals who possess strong self-discipline, are motivated by financial optimization, and can withstand a potentially longer initial period without seeing a debt fully eliminated. It’s the mathematically superior choice for reducing the total cost of your debt, a crucial consideration for long-term financial health and the journey towards how to build generational wealth.

Snowball vs. Avalanche: A Side-by-Side Comparison

The choice between the debt snowball and debt avalanche methods often boils down to a fundamental question: which motivator is stronger for you – psychological momentum or pure financial efficiency? Both methods are powerful tools for debt reduction, but they leverage different aspects of human behavior and financial mathematics.

Key Differences:

- Ordering of Debts:

- Snowball: Smallest balance to largest balance.

- Avalanche: Highest interest rate to lowest interest rate.

- Primary Benefit:

- Snowball: Psychological motivation, quick wins, increased adherence.

- Avalanche: Maximum interest savings, lowest overall cost.

- Target User:

- Snowball: Individuals needing motivation, those prone to giving up, beginners in debt management.

- Avalanche: Disciplined individuals, those focused on financial optimization, analytical thinkers.

- Total Cost:

- Snowball: Generally results in paying more interest over time.

- Avalanche: Results in paying the least amount of interest over time.

- Time to Payoff:

- Snowball: Can feel faster due to quicker initial eliminations, but may take longer overall due to higher interest accumulation.

- Avalanche: Often leads to a faster overall payoff due to less money spent on interest, but the initial period might feel slower.

Pros and Cons Summary:

Debt Snowball

- Pros:

- Excellent for motivation and adherence.

- Provides quick wins that build confidence.

- Simpler to understand and implement.

- Cons:

- Costs more in total interest paid.

- Less mathematically efficient.

Debt Avalanche

- Pros:

- Saves the most money on interest.

- Mathematically the most efficient method.

- Can lead to a faster overall debt-free date.

- Cons:

- Can be demotivating if the highest interest debt is also a large balance.

- Requires strong discipline and patience.

The table below provides a quick visual summary:

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Order of Debts | Smallest Balance First | Highest Interest Rate First |

| Primary Driver | Psychological Motivation | Financial Efficiency |

| Total Interest Paid | Higher | Lower |

| Initial Momentum | Faster (Quick Wins) | Slower (Potentially) |

| Best For | People needing motivation, quick results | Disciplined individuals, saving money |

Ultimately, the “best” method is the one you can stick with consistently. A method that saves you $1,000 in interest but you abandon after three months is far less effective than a method that costs you an extra $500 but keeps you motivated until you’re completely debt-free. Your personal financial temperament plays a much larger role than pure mathematical optimization if consistency is a challenge.

Choosing Your Path: Factors to Consider and Practical Steps

Deciding between the debt snowball and debt avalanche isn’t a one-size-fits-all choice. It requires introspection, an honest assessment of your financial habits, and a clear understanding of your psychological triggers. Here are the key factors Fin3go recommends you consider to make the most informed decision for your journey to financial freedom by 2026.

1. Assess Your Financial Personality and Discipline

- Are you easily discouraged? If you need immediate gratification and find it hard to stick to long-term plans without visible progress, the debt snowball might be a better fit. The quick wins from paying off smaller debts can provide the necessary motivation to keep going.

- Are you highly disciplined and numbers-driven? If you’re comfortable with delayed gratification and prioritize saving money above all else, the debt avalanche method will likely appeal more. You’ll be motivated by the financial efficiency and the knowledge that you’re minimizing your overall cost.

2. Analyze Your Debt Portfolio

- Do you have a few small debts with high interest rates? If your smallest debts also happen to have the highest interest rates, then both methods might align, giving you the best of both worlds (quick wins and interest savings).

- Do you have very high-interest debts that are also large? If your highest interest debts are also your largest, the avalanche method might feel like a very long slog initially. In such cases, if motivation is a concern, the snowball could be a safer bet to get started, even if it costs a bit more.

3. Consider Your Overall Financial Situation

- Emergency Fund: Before aggressively tackling debt, ensure you have a starter emergency fund (e.g., $1,000) to cover unexpected expenses. This prevents you from incurring new debt if an emergency arises.

- Income Stability: If your income is somewhat unpredictable, the psychological boost of the snowball might be more valuable to maintain morale during leaner months.

4. The Role of Budgeting and Expense Management

Regardless of which debt payoff method you choose, its success hinges on your ability to find extra money to throw at your debts. This is where fundamental personal finance practices come into play:

- How To Create A Monthly Budget: A detailed budget is your financial GPS. It allows you to see exactly where your money is going, identify unnecessary expenditures, and earmark specific funds for debt acceleration. Without a budget, you’re essentially flying blind. Track every dollar, categorize your spending, and set realistic limits. This process will inevitably reveal areas where you can free up cash for debt payments.

- How To Negotiate Bills And Lower Expenses: This is an often-overlooked but incredibly powerful strategy. Call your service providers (internet, cable, phone, insurance) and negotiate lower rates. Look for cheaper alternatives for subscriptions, groceries, and entertainment. Even small savings, when consistent, can add up to significant amounts that can be directly applied to your highest-priority debt. Every dollar you save is a dollar you can put towards becoming debt-free faster.

These two practices are not optional; they are foundational to the effective implementation of either the snowball or avalanche method. They provide the fuel that drives your debt reduction engine.

5. Don’t Forget the “Why”

Remind yourself regularly why you are embarking on this journey. Is it to reduce stress, save for a down payment, invest more, or ultimately achieve generational wealth? Keeping your long-term goals in sight can provide the motivation needed to power through the challenging moments, regardless of which method you choose.

Ultimately, the “best” method is the one you can commit to and consistently execute. Analyze your situation, choose a strategy, and then stick with it. The most important step is to start.

Implementing Your Chosen Strategy: Practical Steps for Success

Once you’ve decided whether the debt snowball or debt avalanche is the right path for you, the real work of implementation begins. A strategy, no matter how well-conceived, is only as good as its execution. Here’s a detailed guide on putting your chosen method into action and ensuring its long-term success, setting you up for a stronger financial position by 2026.

1. Create a Master Debt List

This is your foundational document. List every single debt you owe: credit cards, personal loans, student loans, car loans, medical bills, etc. For each debt, record:

- Creditor Name

- Outstanding Balance

- Interest Rate (APR)

- Minimum Monthly Payment

- Due Date

This comprehensive list will allow you to correctly order your debts according to your chosen method (smallest balance for snowball, highest interest rate for avalanche).

2. Develop a Comprehensive Monthly Budget

As emphasized earlier, budgeting is non-negotiable. If you haven’t already, learn how to create a monthly budget that meticulously tracks your income and expenses. This budget will help you:

- Identify Disposable Income: Pinpoint exactly how much extra money you have each month to dedicate to accelerated debt payments beyond your minimums.

- Cut Unnecessary Spending: Discover areas where you can trim expenses, freeing up more cash for debt. Be ruthless in identifying non-essential expenditures.

- Stay Accountable: A budget provides a clear financial picture, allowing you to monitor your progress and make adjustments as needed.

Review your budget regularly, ideally weekly or bi-weekly, to ensure you’re on track and identify any deviations.

3. Optimize Your Spending and Boost Your Income

To maximize the “extra” payments you make, actively look for ways to reduce your outgoing money and increase your incoming money:

- Reduce Expenses: This goes hand-in-hand with budgeting. Look into how to negotiate bills and lower expenses. Call your utility providers, insurance companies, and subscription services. Cancel unused subscriptions. Cook at home more often. Look for free entertainment options.

- Increase Income: Consider side hustles, selling unused items, or asking for a raise at work. Even a small increase in income can significantly accelerate your debt payoff timeline when consistently applied to your target debt.

4. Automate Payments (Where Appropriate)

Set up automatic minimum payments for all your debts to avoid late fees and protect your credit score. For the debt you are aggressively tackling, you’ll need to manually make the extra payments. Be disciplined about sending that extra money as soon as your primary payment clears.

5. Track Your Progress and Celebrate Milestones

Seeing your efforts pay off is incredibly motivating. Use a spreadsheet, an app, or even a physical chart to track your debt balances as they decrease. When you pay off a debt, take a moment to celebrate! These small victories are crucial for maintaining momentum, especially with the avalanche method where initial wins might be further apart.

6. Be Flexible and Persistent

Life happens. There will be months where unexpected expenses arise, or your income might fluctuate. Don’t let a temporary setback derail your entire plan. Adjust your budget, reassess your extra payment amount, and get back on track as quickly as possible. Consistency over time is more important than perfection every single month.

7. Re-evaluate Periodically

It’s a good idea to revisit your debt list and chosen strategy every 6-12 months. Your financial situation might change, interest rates could shift, or your motivation levels might vary. A periodic review ensures your strategy remains the most effective for your current circumstances.

By diligently following these practical steps, you’ll not only implement your chosen debt payoff method effectively but also build strong financial habits that will serve you well long after your debts are gone. This disciplined approach is a critical stepping stone towards achieving broader financial goals, including how to build generational wealth.

Beyond Payoff: Integrating Debt Management into Your Financial Future

The journey to becoming debt-free is a significant accomplishment, but it’s not the end of your financial evolution—it’s a powerful new beginning. Once you’ve successfully eliminated your consumer debts using either the snowball or avalanche method, you’re in a prime position to redirect your financial energy towards building lasting wealth and securing your future. This transition from debt management to wealth creation is a crucial phase that Fin3go encourages all its readers to master.

1. Redirect Your “Debt Payments” into Savings and Investments

The first and most impactful step after paying off debt is to continue “paying yourself.” The money you were previously dedicating to debt payments should now be rerouted into strategic savings and investment vehicles. This is often referred to as the “debt-free dividend.”

- Boost Your Emergency Fund: If you only had a starter emergency fund during your debt payoff, now is the time to build it up to 3-6 months (or even more) of living expenses. This provides a robust financial safety net against job loss, medical emergencies, or unforeseen expenses, preventing you from falling back into debt.

- Fund Retirement Accounts: Maximize contributions to tax-advantaged accounts like 401(k)s, IRAs, and HSAs. The power of compound interest works wonders over time, and every year you contribute earlier and more significantly can have a monumental impact on your retirement nest egg.

- Invest for Mid-Term Goals: Whether it’s a down payment on a home, funding your children’s education, or starting a business, direct funds into appropriate investment vehicles (e.g., brokerage accounts, 529 plans).

2. Focus on Building Generational Wealth

Once you’ve secured your immediate financial future, the focus can shift towards long-term legacy. The principles of how to build generational wealth involve more than just accumulating assets; they encompass strategic planning, smart investing, and responsible stewardship.

- Diversified Investment Portfolio: Work with a financial advisor to create a diversified investment portfolio tailored to your risk tolerance and long-term goals. This may include stocks, bonds, real estate, and other assets.

- Estate Planning: Develop a comprehensive estate plan, including a will, trusts, and power of attorney. This ensures your assets are distributed according to your wishes and minimizes tax implications for your heirs.

- Financial Education for Heirs: A crucial, yet often overlooked, aspect of generational wealth is passing on financial literacy and responsible money habits to future generations. Educate your children and grandchildren about budgeting, saving, investing, and debt management.

- Strategic Real Estate: Beyond your primary residence, consider investment properties that can generate passive income and appreciate over time.

3. Maintain Good Financial Habits

The habits you developed during your debt payoff journey—like rigorous budgeting (how to create a monthly budget) and vigilant expense management (how to negotiate bills and lower expenses)—are invaluable for wealth building. Don’t abandon them. Continue to track your spending, review your financial goals annually, and look for opportunities to optimize your finances. This ongoing discipline ensures you avoid new high-interest debt and continue to grow your net worth.

4. Protect Your Assets

As your wealth grows, so does the importance of protecting it. Ensure you have adequate insurance coverage—life, disability, home, auto, and umbrella liability—to shield your assets from unforeseen circumstances. Review your policies regularly to ensure they meet your current needs.

By transitioning thoughtfully from debt elimination to proactive wealth building, you’re not just improving your own financial standing but also laying a robust foundation for your family’s prosperity for generations to come. The debt-free life you achieve by 2026 is merely the launchpad for an even more ambitious financial journey.

Frequently Asked Questions

What is the absolute best debt payoff method for everyone?▾

Can I combine elements of both the snowball and avalanche methods?▾

How important is having a budget when using these methods?▾

What if I only have one debt? Do these methods still apply?▾

Should I focus on debt payoff or building an emergency fund first?▾

Once I’m debt-free, what should I do next to secure my financial future?▾

Recommended Resources

Related reading: What Is Growth Hacking And How Does It Work (Kacerr).

Related reading: Affiliate Marketing For Beginners 2026 (Page Release).