Wealthfront vs Betterment: The Ultimate Robo-Advisor Showdown for Smart Investing in 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

In the ever-evolving landscape of personal finance technology, choosing the right robo-advisor can significantly impact your financial future. Two names consistently rise to the top of the list for their innovative approaches to automated investing: Wealthfront vs Betterment. These pioneers have democratized sophisticated investment strategies, making them accessible to a broad range of investors, from beginners to seasoned wealth accumulators.

This comprehensive comparison for 2026 delves deep into what makes each platform unique, examining their core philosophies, fee structures, investment methodologies, tax-saving strategies, account offerings, user experience, and overall value proposition. Our goal is to equip you with the knowledge necessary to decide which robo-advisor aligns best with your financial goals and investment style.

TL;DR: Wealthfront vs Betterment Quick Take

- Choose Wealthfront If: You have a higher balance (especially over $100,000) and prioritize advanced tax optimization features like Direct Indexing, sophisticated planning tools, and a robust high-yield cash management account. You’re comfortable with a purely algorithmic approach and seek maximal automation for long-term growth.

- Choose Betterment If: You’re a beginner investor with a smaller starting balance, value optional access to human financial advisors, want a traditional checking account alongside investing, and appreciate a user-friendly platform focused on goal-based planning and behavioral finance.

Table of Contents

- Introduction to Wealthfront vs Betterment

- Core Investment Philosophies and Offerings

- Fees and Pricing: A Head-to-Head Comparison

- Investment Strategies and Portfolio Construction

- Account Types: Beyond the Basics

- Planning Tools and Financial Advice

- User Experience and Mobile Apps

- Detailed Comparison: Wealthfront vs Betterment

- Wealthfront vs Betterment: Which One is Right for You?

- The Future of Robo-Advisors in 2026 and Beyond

- Conclusion

- Frequently Asked Questions

Introduction to Wealthfront vs Betterment

Robo-advisors have revolutionized personal investing by leveraging technology to provide automated, algorithm-driven financial planning services. They offer diversified portfolios, often at a lower cost than traditional financial advisors, making professional-grade investing accessible. In 2026, Wealthfront and Betterment remain at the forefront of this innovation, each carving out a distinct niche in the market.

Wealthfront, founded in 2008, initially targeted tech-savvy investors with a strong emphasis on passive investing, sophisticated tax-loss harvesting, and comprehensive financial planning tools. It positions itself as a digital wealth manager, offering advanced features typically reserved for high-net-worth individuals.

Betterment, launched in 2010, focuses on simplicity, goal-based investing, and a blend of automated advice with optional human assistance. It aims to make investing easy and accessible for everyone, guiding users through their financial journey with behavioral economics principles.

Both platforms excel at automating portfolio management, rebalancing, and dividend reinvestment. However, their underlying strategies, premium offerings, and overall user experiences present clear differentiators that warrant a detailed examination. Understanding these differences is key to deciding whether Wealthfront or Betterment is the superior choice for your investment objectives.

Wealthfront vs Betterment: Core Investment Philosophies and Offerings

At their heart, both Wealthfront and Betterment aim to help individuals grow their wealth through intelligent, diversified investing. However, their foundational approaches and the emphasis they place on certain features differ significantly, catering to distinct investor preferences.

Betterment’s Approach: Diversification and Behavioral Nudges

Betterment operates on the philosophy of making investing intuitive and accessible, particularly for those new to the financial markets. Their core investment strategy revolves around Modern Portfolio Theory (MPT), constructing globally diversified portfolios primarily using low-cost Exchange Traded Funds (ETFs). These portfolios are tailored to your risk tolerance, which is determined through a series of questions during onboarding.

- Goal-Based Investing: Betterment excels at helping users define and track multiple financial goals, whether it’s saving for retirement, a down payment on a home, or a child’s education. The platform allocates your investments across different portfolios based on each goal’s timeline and risk profile.

- Behavioral Finance: Betterment incorporates principles of behavioral economics to help investors stay on track. This includes features like automatic deposits, reminders, and clear progress tracking to minimize emotional decision-making.

- Simplicity and Automation: The platform is designed for ease of use, automating rebalancing, dividend reinvestment, and basic tax-loss harvesting. This “set it and forget it” approach is ideal for busy individuals.

- Optional Human Advice: A key differentiator is Betterment’s willingness to integrate human advice, offering various tiers that provide access to certified financial planners for specific advice or comprehensive planning.

Wealthfront’s Strategy: Sophisticated Algorithms and Advanced Tax Efficiency

Wealthfront positions itself as an advanced digital financial advisor, appealing to investors who seek sophisticated strategies and maximal tax efficiency, often with larger portfolios. Its philosophy centers on optimizing every aspect of the investment process through powerful algorithms and proprietary technology.

- Passive Investing with Active Optimization: While committed to passive, index-based investing, Wealthfront actively seeks to optimize returns through sophisticated strategies like advanced tax-loss harvesting, Direct Indexing, and portfolio line of credit.

- Comprehensive Financial Planning Engine: Wealthfront’s “Path” planning tool integrates all your financial accounts (even those outside Wealthfront) to give a holistic view of your financial future, projecting outcomes for retirement, homeownership, and college savings. It’s designed to simulate scenarios and offer actionable advice based on your aggregated data.

- Robo-Advisory Focus: Wealthfront historically maintained a pure robo-advisor model, emphasizing algorithmic solutions over direct human interaction for core investment management, though it has introduced premium planning services with human CFP access for complex needs.

- Advanced Tax Strategies: This is a cornerstone of Wealthfront’s offering, particularly its advanced forms of tax-loss harvesting and Direct Indexing for larger portfolios, which aim to significantly boost after-tax returns.

Fees and Pricing: A Head-to-Head Comparison

When comparing Wealthfront vs Betterment, understanding their fee structures is paramount. While both offer competitive pricing compared to traditional advisors, nuances in their models can lead to different total costs, especially as your assets grow or if you seek premium services.

Management Fees: What You’ll Pay Annually

Both platforms employ a simple annual advisory fee, calculated as a percentage of your Assets Under Management (AUM). This fee covers portfolio management, rebalancing, and core features.

- Wealthfront: Charges a flat 0.25% annual advisory fee on all investment accounts. There are no trading commissions.

- Betterment: Also charges a flat 0.25% annual advisory fee for its Digital plan. For those seeking human advice, Betterment Premium is available at 0.40% annually (for balances over $100,000), offering unlimited phone calls and emails with CFP® professionals.

At first glance, the standard 0.25% fee appears identical. However, the availability and cost of human advice within the fee structure is a key differentiator. If you anticipate needing financial planning assistance, Betterment’s tiered model might be more straightforward, though Wealthfront offers a separate planning service.

Expense Ratios of Underlying Investments

In addition to the advisory fee, investors also pay the expense ratios of the underlying ETFs or individual stocks within their portfolios. These are charged by the fund providers, not Wealthfront or Betterment, but they are an unavoidable cost of investing.

- Wealthfront: Typically uses ETFs with average expense ratios ranging from 0.07% to 0.16%. For Direct Indexing, there are no ETF expense ratios on the directly owned stocks, but the program itself has a management fee (included in the 0.25% advisory fee) and transaction costs are covered.

- Betterment: Also utilizes low-cost ETFs, with average expense ratios generally falling between 0.07% and 0.17%, depending on the portfolio and asset allocation.

Both platforms do an excellent job of selecting highly efficient, low-cost funds, so the difference in underlying expense ratios is usually negligible and not a primary factor in choosing between them.

Premium Services and Additional Costs

As investors’ needs grow more complex, both platforms offer services beyond their basic advisory. These often come with additional costs or different fee structures.

- Wealthfront:

- Premium Financial Planning: Wealthfront offers access to certified financial planners for specific complex situations. This is typically a separate, one-time fee service rather than an ongoing percentage of AUM, focusing on specific planning needs like estate planning or complex equity compensation. Details and costs are provided upon consultation.

- Portfolio Line of Credit: Available for balances over $25,000, allowing users to borrow against their investment portfolio. Interest rates are competitive and fluctuate with market conditions.

- Betterment:

- Betterment Premium: For balances over $100,000, the management fee increases to 0.40% annually, providing unlimited access to CFP® professionals for advice on life events, retirement, and more.

- Financial Advice Packages: For those with lower balances or specific needs, Betterment offers one-time advice packages (e.g., college planning, retirement planning) at a fixed fee, typically ranging from a few hundred dollars.

- Cash Reserve & Checking: No advisory fees for these services. Interest is earned on Cash Reserve, and checking account transactions are fee-free.

Impact of Account Balance on Fees

The total cost can vary significantly based on your investment amount and whether you opt for premium services.

For example, with a $50,000 portfolio:

- Wealthfront: You’d pay $125 in annual management fees (0.25% of $50,000).

- Betterment (Digital): You’d pay $125 in annual management fees (0.25% of $50,000).

With a $150,000 portfolio:

- Wealthfront: You’d pay $375 in annual management fees (0.25% of $150,000). Here, you also gain access to Direct Indexing and potentially more sophisticated tax strategies.

- Betterment (Digital): You’d pay $375 in annual management fees.

- Betterment (Premium): You could opt for Premium at 0.40%, costing $600 annually, but gaining unlimited access to human advisors.

For investors with over $100,000, Betterment’s Premium offering becomes a direct cost consideration if human advice is desired. Wealthfront keeps its core investment management fee at 0.25% regardless of balance, but its premium planning is separate. Your preference for a pure algorithmic approach versus hybrid human/robo advice will heavily influence which fee structure you find more appealing.

[INLINE IMAGE 1: place after second H2 | alt=”wealthfront vs betterment concept illustration”]

Investment Strategies and Portfolio Construction

Beyond fees, the core investment methodology employed by each robo-advisor is critical. Both Wealthfront and Betterment leverage modern portfolio theory and passive investing, but they differ in the sophistication of their tax strategies and the breadth of their investment options.

Diversification and ETF Portfolios

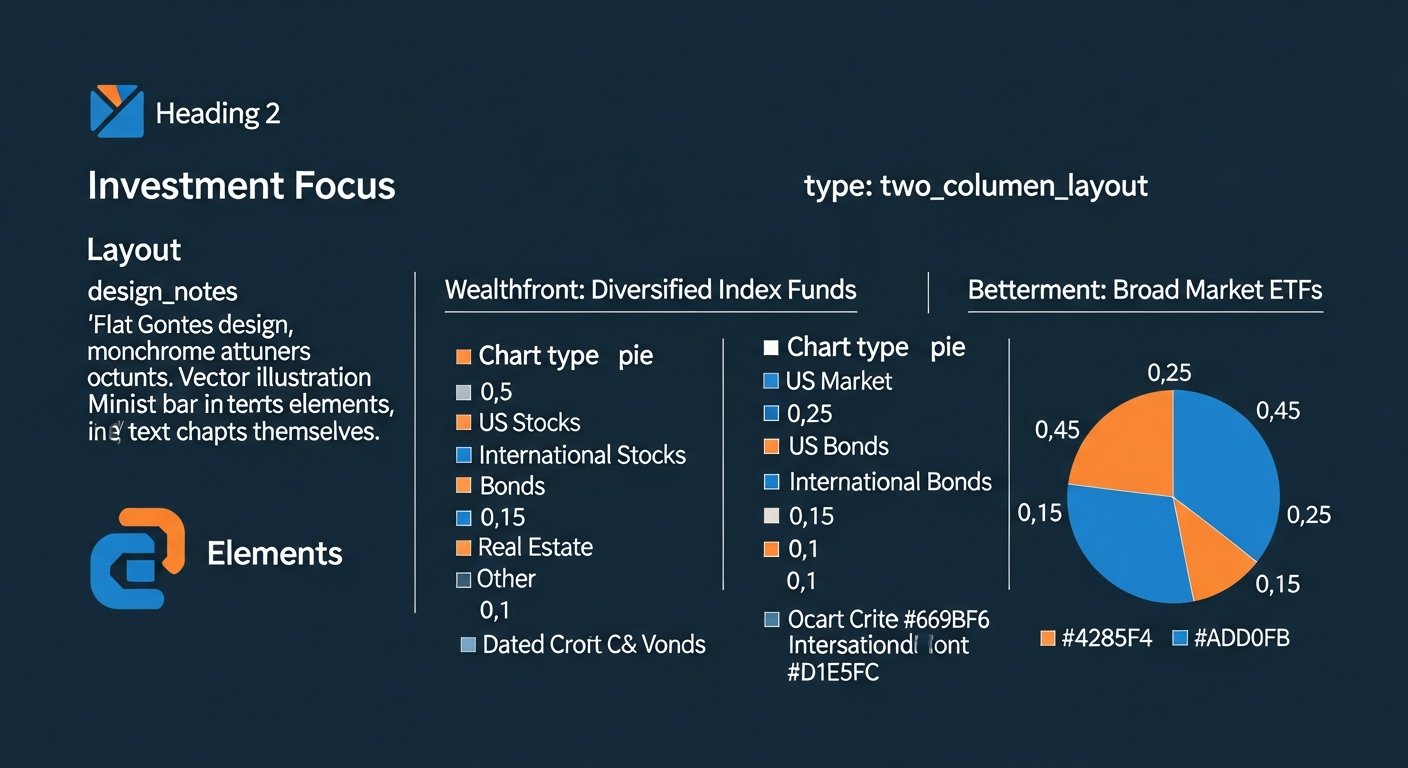

Both platforms build globally diversified portfolios using low-cost ETFs across various asset classes:

- Core Assets: Typically include US stocks, international stocks, emerging markets stocks, US bonds, international bonds, and real estate (REITs).

- Risk Assessment: During onboarding, both assess your risk tolerance through questionnaires and recommend a suitable asset allocation (e.g., 80% stocks / 20% bonds).

- Automatic Rebalancing: Portfolios are automatically rebalanced when they drift significantly from target allocations, ensuring your risk profile remains consistent.

The specific ETFs used by Wealthfront and Betterment are highly similar, focusing on broad market exposure with low expense ratios. Neither platform attempts to “beat the market” through active stock picking; instead, they aim to capture market returns efficiently.

Tax-Loss Harvesting: Betterment’s Standard vs. Wealthfront’s Advanced

Tax-loss harvesting (TLH) is a crucial strategy offered by both robo-advisors. It involves selling investments at a loss to offset capital gains and potentially up to $3,000 of ordinary income annually, then reinvesting in similar (but not “substantially identical”) assets to maintain diversification.

- Betterment’s Tax-Loss Harvesting:

- Offered as a standard feature for all taxable accounts.

- Performs TLH at the ETF level. If one ETF in your portfolio drops, Betterment will sell it and buy a highly correlated but different ETF to replace it.

- Effective for basic tax deferral and reduction.

- Wealthfront’s Advanced Tax-Loss Harvesting:

- Also a standard feature for all taxable accounts.

- Wealthfront’s approach is often considered more aggressive and potentially more impactful. For smaller balances, it performs daily TLH at the ETF level.

- For balances over $100,000, Wealthfront introduces “Stock-Level Tax-Loss Harvesting” which is part of their Direct Indexing service (see below), greatly enhancing TLH opportunities.

The difference here is significant for larger taxable portfolios. Wealthfront’s ability to harvest losses at the individual stock level potentially generates greater tax savings than Betterment’s ETF-level approach.

Direct Indexing (Wealthfront) and Its Benefits

Direct Indexing is a premium tax-optimization feature unique to Wealthfront among major robo-advisors, available for taxable accounts with at least $100,000. Instead of buying a single ETF that tracks an index (like the S&P 500), Wealthfront purchases the individual stocks within that index directly.

- Enhanced Tax-Loss Harvesting: By owning individual stocks, Wealthfront can sell specific underperforming stocks at a loss without selling the entire index, dramatically increasing the frequency and magnitude of tax-loss harvesting opportunities. This often leads to “tax alpha” – additional returns generated purely from tax savings.

- Customization: Direct Indexing allows for more granular customization, such as excluding specific companies or industries from your portfolio, aligning with personal values.

- Lower Expense Ratios: Since you own individual stocks instead of an ETF, you avoid the expense ratio of the ETF. While this benefit can be offset by transaction costs, Wealthfront states their 0.25% fee covers these.

For high-net-worth investors with significant taxable assets, Wealthfront’s Direct Indexing can be a powerful tool to boost after-tax returns, making it a compelling advantage over Betterment for this specific segment.

Socially Responsible Investing (SRI) and ESG Options

Both Wealthfront and Betterment recognize the growing demand for investments that align with personal values and offer socially responsible investing (SRI) or Environmental, Social, and Governance (ESG) portfolios.

- Betterment SRI Portfolios: Offers multiple SRI options. You can choose from “Broad Impact” (focused on all ESG factors), “Climate Impact” (targeting companies reducing carbon emissions), and “Social Impact” (promoting minority empowerment and gender diversity). These portfolios invest in ETFs that screen companies based on ESG criteria.

- Wealthfront Socially Responsible Investing: Provides an SRI portfolio option that invests in ETFs screened for companies with strong environmental, social, and governance practices, while avoiding those involved in fossil fuels, tobacco, and controversial weapons. For Direct Indexing clients, the ability to exclude specific companies offers a higher degree of customization for ethical investing.

Both platforms offer robust options here, allowing investors to put their money where their values are without sacrificing diversification.

Risk Assessment and Portfolio Customization

Determining an appropriate risk level is fundamental to automated investing. Both platforms use questionnaires to gauge your comfort with market fluctuations and your time horizon.

- Betterment: Guides users to select a risk level for each financial goal, allowing for different allocations across multiple objectives (e.g., lower risk for a short-term down payment goal, higher risk for long-term retirement).

- Wealthfront: Assigns a single risk score based on your answers but allows for some manual adjustment if you feel your initial score doesn’t accurately reflect your preferences. Its “Path” tool also helps visualize how different risk levels impact your financial projections.

While the initial assessment is similar, Wealthfront’s ability to factor in external accounts into its planning tool provides a more holistic view of your overall financial risk exposure, which can be beneficial for comprehensive planning.

Account Types: Beyond the Basics

A comprehensive financial strategy involves more than just a single investment account. Both Wealthfront and Betterment offer a range of account types to help you save and invest for various goals, but their offerings in cash management and specialized accounts differ.

Taxable Brokerage Accounts

Both platforms offer individual and joint taxable brokerage accounts. These are flexible, allowing you to withdraw funds at any time, but profits are subject to capital gains taxes.

- Wealthfront: Provides individual, joint, and trust accounts. Its advanced tax-loss harvesting and Direct Indexing features are most impactful within these taxable accounts, maximizing after-tax returns.

- Betterment: Offers individual, joint, and trust accounts. Its standard tax-loss harvesting applies to these accounts.

Retirement Accounts (IRAs, Roth IRAs, 401k Rollovers)

Retirement savings are a cornerstone of financial planning, and both robo-advisors support common retirement vehicles.

- Wealthfront: Supports Traditional, Roth, SEP, and Solo 401(k) IRAs, along with 401(k) rollovers. Wealthfront’s Path planning tool integrates these accounts to help project your retirement readiness across all your assets.

- Betterment: Offers Traditional, Roth, SEP, and Inherited IRAs, as well as 401(k) rollovers. Betterment’s goal-setting features make it easy to set up and track progress towards retirement.

The core offerings for retirement accounts are very similar. The main difference might lie in how each platform integrates these accounts into a broader financial plan and the sophistication of its projection tools.

Specialized Accounts: 529 Plans and HSAs

For more specific financial goals, both platforms extend their offerings to specialized accounts:

- 529 College Savings Plans: Both Wealthfront and Betterment offer 529 plans, allowing you to invest for future education expenses with potential tax benefits. These plans are state-sponsored, and each platform partners with specific states to offer their investment options.

- Health Savings Accounts (HSAs): Betterment was an early adopter in offering HSAs with integrated investing options, allowing users to invest their HSA funds for long-term growth. Wealthfront has since introduced its own HSA offering, enabling users to invest their health savings in diversified portfolios. HSAs are often referred to as “triple tax-advantaged” accounts, making them powerful for long-term savings.

The availability of these specialized accounts ensures that both platforms can cater to a wider array of financial planning needs, from education to healthcare savings.

Cash Management: High-Yield Savings and Checking Options

The integration of banking and investment services is a growing trend. This is where Wealthfront vs Betterment show distinct approaches.

- Wealthfront Cash Account:

- Offers a high-yield cash account with a competitive interest rate.

- Provides FDIC insurance up to $8 million through partner banks (as of 2026).

- Includes a debit card for transactions but is not a full-fledged checking account (e.g., no bill pay, limited check writing, though direct deposit is supported).

- Designed more as a high-yield savings alternative than a primary checking solution.

- Betterment Cash Reserve & Checking:

- Cash Reserve: A high-yield savings account that offers competitive interest rates and extended FDIC insurance through partner banks.

- Checking Account: Betterment offers a full checking account with a Visa debit card, ATM fee refunds worldwide, and no monthly fees. It supports direct deposit and bill pay, making it a viable primary checking solution.

For users seeking an integrated banking and investing experience, Betterment’s full checking account is a strong advantage. Wealthfront’s Cash Account is excellent for high-yield savings, but it doesn’t replace a traditional checking account for everyday transactions in the same way Betterment’s offering does.

[INLINE IMAGE 2: place after fourth H2 | alt=”wealthfront vs betterment comparison illustration”]

Planning Tools and Financial Advice

Beyond automated investing, a key aspect of robo-advisors is their ability to help users plan for their financial future. This involves everything from setting goals to projecting outcomes and, for some, offering access to human expertise.

Goal-Setting and Projection Tools

Both platforms excel at helping users define and work towards their financial objectives.

- Betterment: Its entire interface is built around goal-based investing. Users create specific goals (e.g., retirement, down payment, emergency fund), and Betterment tailors portfolios and savings advice for each. Its projection tools show how current savings rates and investment performance impact the likelihood of reaching each goal.

- Wealthfront’s “Path” Planning Tool: This is a powerful, comprehensive planning engine. It connects to all your financial accounts (checking, savings, credit cards, mortgages, student loans, other investment accounts) to provide a holistic view of your finances. Path then projects various scenarios (e.g., “Can I retire early?”, “Can I afford this house?”) and offers personalized advice based on your aggregated data. It’s an exceptionally robust tool for detailed financial scenario planning.

While Betterment’s goal-setting is intuitive and effective, Wealthfront’s Path tool offers a more integrated and sophisticated approach to comprehensive financial planning, especially for those with complex financial pictures and multiple external accounts.

For a deeper dive into financial planning apps, explore our comprehensive guide.

Access to Human Financial Advisors

The level of human interaction is one of the most significant differentiators between Wealthfront and Betterment.

- Betterment: Has embraced a hybrid model, offering tiered access to human financial advisors.

- Betterment Digital (0.25% AUM): Primarily automated, but offers one-time advice packages for a fixed fee.

- Betterment Premium (0.40% AUM, for balances >$100,000): Provides unlimited phone and email access to a team of CFP® professionals for advice on retirement, investing, and other life

Wealthfront vs Betterment: The Ultimate Robo-Advisor Showdown for Smart Investing in 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

In the ever-evolving landscape of personal finance technology, choosing the right robo-advisor can significantly impact your financial future. Two names consistently rise to the top of the list for their innovative approaches to automated investing: Wealthfront vs Betterment. These pioneers have democratized sophisticated investment strategies, making them accessible to a broad range of investors, from beginners to seasoned wealth accumulators.

This comprehensive comparison for 2026 delves deep into what makes each platform unique, examining their core philosophies, fee structures, investment methodologies, tax-saving strategies, account offerings, user experience, and overall value proposition. Our goal is to equip you with the knowledge necessary to decide which robo-advisor aligns best with your financial goals and investment style.

TL;DR: Wealthfront vs Betterment Quick Take

- Choose Wealthfront If: You have a higher balance (especially over $100,000) and prioritize advanced tax optimization features like Direct Indexing, sophisticated planning tools, and a robust high-yield cash management account. You’re comfortable with a purely algorithmic approach and seek maximal automation for long-term growth.

- Choose Betterment If: You’re a beginner investor with a smaller starting balance, value optional access to human financial advisors, want a traditional checking account alongside investing, and appreciate a user-friendly platform focused on goal-based planning and behavioral finance.

Table of Contents

- Introduction to Wealthfront vs Betterment

- Core Investment Philosophies and Offerings

- Fees and Pricing: A Head-to-Head Comparison

- Investment Strategies and Portfolio Construction

- Account Types: Beyond the Basics

- Planning Tools and Financial Advice

- User Experience and Mobile Apps

- Detailed Comparison: Wealthfront vs Betterment

- Wealthfront vs Betterment: Which One is Right for You?

- The Future of Robo-Advisors in 2026 and Beyond

- Conclusion

- Frequently Asked Questions

Introduction to Wealthfront vs Betterment

Robo-advisors have revolutionized personal investing by leveraging technology to provide automated, algorithm-driven financial planning services. They offer diversified portfolios, often at a lower cost than traditional financial advisors, making professional-grade investing accessible. In 2026, Wealthfront and Betterment remain at the forefront of this innovation, each carving out a distinct niche in the market.

Wealthfront, founded in 2008, initially targeted tech-savvy investors with a strong emphasis on passive investing, sophisticated tax-loss harvesting, and comprehensive financial planning tools. It positions itself as a digital wealth manager, offering advanced features typically reserved for high-net-worth individuals.

Betterment, launched in 2010, focuses on simplicity, goal-based investing, and a blend of automated advice with optional human assistance. It aims to make investing easy and accessible for everyone, guiding users through their financial journey with behavioral economics principles.

Both platforms excel at automating portfolio management, rebalancing, and dividend reinvestment. However, their underlying strategies, premium offerings, and overall user experiences present clear differentiators that warrant a detailed examination. Understanding these differences is key to deciding whether Wealthfront or Betterment is the superior choice for your investment objectives.

Wealthfront vs Betterment: Core Investment Philosophies and Offerings

At their heart, both Wealthfront and Betterment aim to help individuals grow their wealth through intelligent, diversified investing. However, their foundational approaches and the emphasis they place on certain features differ significantly, catering to distinct investor preferences.

Betterment’s Approach: Diversification and Behavioral Nudges

Betterment operates on the philosophy of making investing intuitive and accessible, particularly for those new to the financial markets. Their core investment strategy revolves around Modern Portfolio Theory (MPT), constructing globally diversified portfolios primarily using low-cost Exchange Traded Funds (ETFs). These portfolios are tailored to your risk tolerance, which is determined through a series of questions during onboarding.

- Goal-Based Investing: Betterment excels at helping users define and track multiple financial goals, whether it’s saving for retirement, a down payment on a home, or a child’s education. The platform allocates your investments across different portfolios based on each goal’s timeline and risk profile.

- Behavioral Finance: Betterment incorporates principles of behavioral economics to help investors stay on track. This includes features like automatic deposits, reminders, and clear progress tracking to minimize emotional decision-making.

- Simplicity and Automation: The platform is designed for ease of use, automating rebalancing, dividend reinvestment, and basic tax-loss harvesting. This “set it and forget it” approach is ideal for busy individuals.

- Optional Human Advice: A key differentiator is Betterment’s willingness to integrate human advice, offering various tiers that provide access to certified financial planners for specific advice or comprehensive planning.

Wealthfront’s Strategy: Sophisticated Algorithms and Advanced Tax Efficiency

Wealthfront positions itself as an advanced digital financial advisor, appealing to investors who seek sophisticated strategies and maximal tax efficiency, often with larger portfolios. Its philosophy centers on optimizing every aspect of the investment process through powerful algorithms and proprietary technology.

- Passive Investing with Active Optimization: While committed to passive, index-based investing, Wealthfront actively seeks to optimize returns through sophisticated strategies like advanced tax-loss harvesting, Direct Indexing, and portfolio line of credit.

- Comprehensive Financial Planning Engine: Wealthfront’s “Path” planning tool integrates all your financial accounts (even those outside Wealthfront) to give a holistic view of your financial future, projecting outcomes for retirement, homeownership, and college savings. It’s designed to simulate scenarios and offer actionable advice based on your aggregated data.

- Robo-Advisory Focus: Wealthfront historically maintained a pure robo-advisor model, emphasizing algorithmic solutions over direct human interaction for core investment management, though it has introduced premium planning services with human CFP access for complex needs.

- Advanced Tax Strategies: This is a cornerstone of Wealthfront’s offering, particularly its advanced forms of tax-loss harvesting and Direct Indexing for larger portfolios, which aim to significantly boost after-tax returns.

Fees and Pricing: A Head-to-Head Comparison

When comparing Wealthfront vs Betterment, understanding their fee structures is paramount. While both offer competitive pricing compared to traditional advisors, nuances in their models can lead to different total costs, especially as your assets grow or if you seek premium services.

Management Fees: What You’ll Pay Annually

Both platforms employ a simple annual advisory fee, calculated as a percentage of your Assets Under Management (AUM). This fee covers portfolio management, rebalancing, and core features.

- Wealthfront: Charges a flat 0.25% annual advisory fee on all investment accounts. There are no trading commissions.

- Betterment: Also charges a flat 0.25% annual advisory fee for its Digital plan. For those seeking human advice, Betterment Premium is available at 0.40% annually (for balances over $100,000), offering unlimited phone calls and emails with CFP® professionals.

At first glance, the standard 0.25% fee appears identical. However, the availability and cost of human advice within the fee structure is a key differentiator. If you anticipate needing financial planning assistance, Betterment’s tiered model might be more straightforward, though Wealthfront offers a separate planning service.

Expense Ratios of Underlying Investments

In addition to the advisory fee, investors also pay the expense ratios of the underlying ETFs or individual stocks within their portfolios. These are charged by the fund providers, not Wealthfront or Betterment, but they are an unavoidable cost of investing.

- Wealthfront: Typically uses ETFs with average expense ratios ranging from 0.07% to 0.16%. For Direct Indexing, there are no ETF expense ratios on the directly owned stocks, but the program itself has a management fee (included in the 0.25% advisory fee) and transaction costs are covered.

- Betterment: Also utilizes low-cost ETFs, with average expense ratios generally falling between 0.07% and 0.17%, depending on the portfolio and asset allocation.

Both platforms do an excellent job of selecting highly efficient, low-cost funds, so the difference in underlying expense ratios is usually negligible and not a primary factor in choosing between them.

Premium Services and Additional Costs

As investors’ needs grow more complex, both platforms offer services beyond their basic advisory. These often come with additional costs or different fee structures.

- Wealthfront:

- Premium Financial Planning: Wealthfront offers access to certified financial planners for specific complex situations. This is typically a separate, one-time fee service rather than an ongoing percentage of AUM, focusing on specific planning needs like estate planning or complex equity compensation. Details and costs are provided upon consultation.

- Portfolio Line of Credit: Available for balances over $25,000, allowing users to borrow against their investment portfolio. Interest rates are competitive and fluctuate with market conditions.

- Betterment:

- Betterment Premium: For balances over $100,000, the management fee increases to 0.40% annually, providing unlimited access to CFP® professionals for advice on life events, retirement, and more.

- Financial Advice Packages: For those with lower balances or specific needs, Betterment offers one-time advice packages (e.g., college planning, retirement planning) at a fixed fee, typically ranging from a few hundred dollars.

- Cash Reserve & Checking: No advisory fees for these services. Interest is earned on Cash Reserve, and checking account transactions are fee-free.

Impact of Account Balance on Fees

The total cost can vary significantly based on your investment amount and whether you opt for premium services.

For example, with a $50,000 portfolio:- Wealthfront: You’d pay $125 in annual management fees (0.25% of $50,000).

- Betterment (Digital): You’d pay $125 in annual management fees (0.25% of $50,000).

With a $150,000 portfolio:

- Wealthfront: You’d pay $375 in annual management fees (0.25% of $150,000). Here, you also gain access to Direct Indexing and potentially more sophisticated tax strategies.

- Betterment (Digital): You’d pay $375 in annual management fees.

- Betterment (Premium): You could opt for Premium at 0.40%, costing $600 annually, but gaining unlimited access to human advisors.

For investors with over $100,000, Betterment’s Premium offering becomes a direct cost consideration if human advice is desired. Wealthfront keeps its core investment management fee at 0.25% regardless of balance, but its premium planning is separate. Your preference for a pure algorithmic approach versus hybrid human/robo advice will heavily influence which fee structure you find more appealing.

[INLINE IMAGE 1: place after second H2 | alt=”wealthfront vs betterment concept illustration”]

Investment Strategies and Portfolio Construction

Beyond fees, the core investment methodology employed by each robo-advisor is critical. Both Wealthfront and Betterment leverage modern portfolio theory and passive investing, but they differ in the sophistication of their tax strategies and the breadth of their investment options.

Diversification and ETF Portfolios

Both platforms build globally diversified portfolios using low-cost ETFs across various asset classes:

- Core Assets: Typically include US stocks, international stocks, emerging markets stocks, US bonds, international bonds, and real estate (REITs).

- Risk Assessment: During onboarding, both assess your risk tolerance through questionnaires and recommend a suitable asset allocation (e.g., 80% stocks / 20% bonds).

- Automatic Rebalancing: Portfolios are automatically rebalanced when they drift significantly from target allocations, ensuring your risk profile remains consistent.

The specific ETFs used by Wealthfront and Betterment are highly similar, focusing on broad market exposure with low expense ratios. Neither platform attempts to “beat the market” through active stock picking; instead, they aim to capture market returns efficiently.

Tax-Loss Harvesting: Betterment’s Standard vs. Wealthfront’s Advanced

Tax-loss harvesting (TLH) is a crucial strategy offered by both robo-advisors. It involves selling investments at a loss to offset capital gains and potentially up to $3,000 of ordinary income annually, then reinvesting in similar (but not “substantially identical”) assets to maintain diversification.

- Betterment’s Tax-Loss Harvesting:

- Offered as a standard feature for all taxable accounts.

- Performs TLH at the ETF level. If one ETF in your portfolio drops, Betterment will sell it and buy a highly correlated but different ETF to replace it.

- Effective for basic tax deferral and reduction.

- Wealthfront’s Advanced Tax-Loss Harvesting:

- Also a standard feature for all taxable accounts.

- Wealthfront’s approach is often considered more aggressive and potentially more impactful. For smaller balances, it performs daily TLH at the ETF level.

- For balances over $100,000, Wealthfront introduces “Stock-Level Tax-Loss Harvesting” which is part of their Direct Indexing service (see below), greatly enhancing TLH opportunities.

The difference here is significant for larger taxable portfolios. Wealthfront’s ability to harvest losses at the individual stock level potentially generates greater tax savings than Betterment’s ETF-level approach.

Direct Indexing (Wealthfront) and Its Benefits

Direct Indexing is a premium tax-optimization feature unique to Wealthfront among major robo-advisors, available for taxable accounts with at least $100,000. Instead of buying a single ETF that tracks an index (like the S&P 500), Wealthfront purchases the individual stocks within that index directly.

- Enhanced Tax-Loss Harvesting: By owning individual stocks, Wealthfront can sell specific underperforming stocks at a loss without selling the entire index, dramatically increasing the frequency and magnitude of tax-loss harvesting opportunities. This often leads to “tax alpha” – additional returns generated purely from tax savings.

- Customization: Direct Indexing allows for more granular customization, such as excluding specific companies or industries from your portfolio, aligning with personal values.

- Lower Expense Ratios: Since you own individual stocks instead of an ETF, you avoid the expense ratio of the ETF. While this benefit can be offset by transaction costs, Wealthfront states their 0.25% fee covers these.

For high-net-worth investors with significant taxable assets, Wealthfront’s Direct Indexing can be a powerful tool to boost after-tax returns, making it a compelling advantage over Betterment for this specific segment.

Socially Responsible Investing (SRI) and ESG Options

Both Wealthfront and Betterment recognize the growing demand for investments that align with personal values and offer socially responsible investing (SRI) or Environmental, Social, and Governance (ESG) portfolios.

- Betterment SRI Portfolios: Offers multiple SRI options. You can choose from “Broad Impact” (focused on all ESG factors), “Climate Impact” (targeting companies reducing carbon emissions), and “Social Impact” (promoting minority empowerment and gender diversity). These portfolios invest in ETFs that screen companies based on ESG criteria.

- Wealthfront Socially Responsible Investing: Provides an SRI portfolio option that invests in ETFs screened for companies with strong environmental, social, and governance practices, while avoiding those involved in fossil fuels, tobacco, and controversial weapons. For Direct Indexing clients, the ability to exclude specific companies offers a higher degree of customization for ethical investing.

Both platforms offer robust options here, allowing investors to put their money where their values are without sacrificing diversification.

Risk Assessment and Portfolio Customization

Determining an appropriate risk level is fundamental to automated investing. Both platforms use questionnaires to gauge your comfort with market fluctuations and your time horizon.

- Betterment: Guides users to select a risk level for each financial goal, allowing for different allocations across multiple objectives (e.g., lower risk for a short-term down payment goal, higher risk for long-term retirement).

- Wealthfront: Assigns a single risk score based on your answers but allows for some manual adjustment if you feel your initial score doesn’t accurately reflect your preferences. Its “Path” tool also helps visualize how different risk levels impact your financial projections.

While the initial assessment is similar, Wealthfront’s ability to factor in external accounts into its planning tool provides a more holistic view of your overall financial risk exposure, which can be beneficial for comprehensive planning.

Account Types: Beyond the Basics

A comprehensive financial strategy involves more than just a single investment account. Both Wealthfront and Betterment offer a range of account types to help you save and invest for various goals, but their offerings in cash management and specialized accounts differ.

Taxable Brokerage Accounts

Both platforms offer individual and joint taxable brokerage accounts. These are flexible, allowing you to withdraw funds at any time, but profits are subject to capital gains taxes.

- Wealthfront: Provides individual, joint, and trust accounts. Its advanced tax-loss harvesting and Direct Indexing features are most impactful within these taxable accounts, maximizing after-tax returns.

- Betterment: Offers individual, joint, and trust accounts. Its standard tax-loss harvesting applies to these accounts.

Retirement Accounts (IRAs, Roth IRAs, 401k Rollovers)

Retirement savings are a cornerstone of financial planning, and both robo-advisors support common retirement vehicles.

- Wealthfront: Supports Traditional, Roth, SEP, and Solo 401(k) IRAs, along with 401(k) rollovers. Wealthfront’s Path planning tool integrates these accounts to help project your retirement readiness across all your assets.

- Betterment: Offers Traditional, Roth, SEP, and Inherited IRAs, as well as 401(k) rollovers. Betterment’s goal-setting features make it easy to set up and track progress towards retirement.

The core offerings for retirement accounts are very similar. The main difference might lie in how each platform integrates these accounts into a broader financial plan and the sophistication of its projection tools.

Specialized Accounts: 529 Plans and HSAs

For more specific financial goals, both platforms extend their offerings to specialized accounts:

- 529 College Savings Plans: Both Wealthfront and Betterment offer 529 plans, allowing you to invest for future education expenses with potential tax benefits. These plans are state-sponsored, and each platform partners with specific states to offer their investment options.

- Health Savings Accounts (HSAs): Betterment was an early adopter in offering HSAs with integrated investing options, allowing users to invest their HSA funds for long-term growth. Wealthfront has since introduced its own HSA offering, enabling users to invest their health savings in diversified portfolios. HSAs are often referred to as “triple tax-advantaged” accounts, making them powerful for long-term savings.

The availability of these specialized accounts ensures that both platforms can cater to a wider array of financial planning needs, from education to healthcare savings.

Cash Management: High-Yield Savings and Checking Options

The integration of banking and investment services is a growing trend. This is where Wealthfront vs Betterment show distinct approaches.

- Wealthfront Cash Account:

- Offers a high-yield cash account with a competitive interest rate.

- Provides FDIC insurance up to $8 million through partner banks (as of 2026).

- Includes a debit card for transactions but is not a full-fledged checking account (e.g., no bill pay, limited check writing, though direct deposit is supported).

- Designed more as a high-yield savings alternative than a primary checking solution.

- Betterment Cash Reserve & Checking:

- Cash Reserve: A high-yield savings account that offers competitive interest rates and extended FDIC insurance through partner banks.

- Checking Account: Betterment offers a full checking account with a Visa debit card, ATM fee refunds worldwide, and no monthly fees. It supports direct deposit and bill pay, making it a viable primary checking solution.

For users seeking an integrated banking and investing experience, Betterment’s full checking account is a strong advantage. Wealthfront’s Cash Account is excellent for high-yield savings, but it doesn’t replace a traditional checking account for everyday transactions in the same way Betterment’s offering does.

[INLINE IMAGE 2: place after fourth H2 | alt=”wealthfront vs betterment comparison illustration”]

Planning Tools and Financial Advice

Beyond automated investing, a key aspect of robo-advisors is their ability to help users plan for their financial future. This involves everything from setting goals to projecting outcomes and, for some, offering access to human expertise.

Goal-Setting and Projection Tools

Both platforms excel at helping users define and work towards their financial objectives.

- Betterment: Its entire interface is built around goal-based investing. Users create specific goals (e.g., retirement, down payment, emergency fund), and Betterment tailors portfolios and savings advice for each. Its projection tools show how current savings rates and investment performance impact the likelihood of reaching each goal.

- Wealthfront’s “Path” Planning Tool: This is a powerful, comprehensive planning engine. It connects to all your financial accounts (checking, savings, credit cards, mortgages, student loans, other investment accounts) to provide a holistic view of your finances. Path then projects various scenarios (e.g., “Can I retire early?”, “Can I afford this house?”) and offers personalized advice based on your aggregated data. It’s an exceptionally robust tool for detailed financial scenario planning.

While Betterment’s goal-setting is intuitive and effective, Wealthfront’s Path tool offers a more integrated and sophisticated approach to comprehensive financial planning, especially for those with complex financial pictures and multiple external accounts.

For a deeper dive into financial planning apps, explore our comprehensive guide.Access to Human Financial Advisors

The level of human interaction is one of the most significant differentiators between Wealthfront and Betterment.

- Betterment: Has embraced a hybrid model, offering tiered access to human financial advisors.

- Betterment Digital (0.25% AUM): Primarily automated, but offers one-time advice packages for a fixed fee.

- Betterment Premium (0.40% AUM, for balances >$100,000): Provides unlimited phone and email access to a team of CFP® professionals for advice on retirement, investing, and other life