How Do Robo-Advisors Work? Unlocking the Mechanics of Automated Investing for 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

In the rapidly evolving landscape of personal finance, robo-advisors have emerged as a transformative force, democratizing access to professional investment management that was once exclusive to the wealthy. As of 2026, these digital platforms are no longer a niche offering but a mainstream solution for millions seeking efficient, low-cost ways to grow their wealth. But beyond the slick interfaces and promises of automation, a fundamental question often arises: exactly how do robo-advisors work?

This comprehensive guide from fin3go delves deep into the inner workings of robo-advisors, peeling back the layers of algorithms, technology, and financial theory that power them. We’ll explore everything from the initial user onboarding process to sophisticated portfolio management techniques like rebalancing and tax-loss harvesting. Whether you’re a seasoned investor curious about digital advancements or a newcomer looking for an accessible entry point into the market, understanding the mechanics of robo-advisors is crucial for making informed financial decisions in the modern era.

From their origins as simple automated portfolio rebalancers to their current incarnation as sophisticated financial planning tools, robo-advisors represent a significant paradigm shift. They leverage cutting-edge technology, including artificial intelligence and machine learning, to provide personalized investment advice and management at a fraction of the cost of traditional human advisors. This article aims to demystify these platforms, providing clarity on their operation, benefits, limitations, and what the future holds for automated investing.

Understanding the Core Concept of Robo-Advisors: More Than Just Automation

At its heart, a robo-advisor is a digital platform that provides automated, algorithm-driven financial planning services with little to no human supervision. The “robo” in their name signifies the automated, technology-driven nature of their operations, distinguishing them from traditional financial advisors who primarily offer face-to-face, human-led advice. However, labeling them merely as “automated” oversimplifies the intricate systems and thoughtful design that underpin their functionality. They are, in essence, a sophisticated fusion of financial wisdom and computational power.

What is a Robo-Advisor? Demystifying the Digital Financial Manager

A robo-advisor serves as a digital stand-in for a human financial advisor, but instead of relying on individual human judgment for every decision, it uses complex algorithms to manage investments. These algorithms are built upon established financial theories and principles, such as Modern Portfolio Theory (MPT), which emphasizes diversification and asset allocation. When you interact with a robo-advisor, you’re engaging with a highly programmed system designed to optimize your portfolio based on specific inputs.

Key services typically offered by a robo-advisor include:

- Automated Portfolio Creation: Based on your financial goals and risk tolerance.

- Diversified Investment Strategies: Often utilizing low-cost Exchange Traded Funds (ETFs) and mutual funds.

- Automatic Rebalancing: Adjusting your portfolio back to its target asset allocation.

- Tax Optimization: Features like tax-loss harvesting to minimize your tax liability.

- Goal-Based Planning: Helping you save for retirement, a down payment, or other life events.

Unlike traditional brokers who execute trades based on your instructions, robo-advisors take a more holistic approach, managing your portfolio proactively in alignment with your defined objectives.

The Shift from Traditional to Digital Advice: A Paradigm Change

For decades, professional financial advice was largely the domain of high-net-worth individuals, given the substantial fees and minimum asset requirements of human advisors. The advent of robo-advisors has dramatically altered this landscape. This shift wasn’t just about making advice cheaper; it was about making it accessible, convenient, and transparent for a broader demographic.

The driving forces behind this transition include:

- Technological Advancements: The proliferation of high-speed internet, powerful computing, and sophisticated algorithms made complex financial modeling feasible for mass application.

- Demand for Convenience: Modern investors, accustomed to digital interactions in other aspects of their lives, sought similar ease and accessibility for their financial management.

- Cost Efficiency: Automating many aspects of portfolio management drastically reduces overheads, allowing robo-advisors to offer services at a significantly lower cost.

- Democratization of Investing: Lower minimums and simplified processes opened the door to investing for individuals who previously found traditional services prohibitive or intimidating.

This paradigm shift has not entirely replaced human advisors but has created a complementary ecosystem where investors can choose the level of human interaction they desire, often at varying price points.

The Role of AI and Algorithms in Robo-Advisor Functionality

The “brain” of any robo-advisor lies in its sophisticated algorithms and, increasingly, artificial intelligence (AI) and machine learning (ML) capabilities. These technologies perform several critical functions:

- Risk Assessment: Algorithms analyze user responses to questionnaires to quantify risk tolerance and financial goals.

- Portfolio Construction: Based on the risk profile, algorithms select a diversified portfolio of investments designed to meet the user’s objectives.

- Market Monitoring: AI systems continuously monitor market conditions and portfolio performance.

- Automated Adjustments: Algorithms automatically trigger actions like rebalancing or tax-loss harvesting when pre-defined conditions are met.

- Personalization: While initially rule-based, newer AI models are learning to offer more nuanced recommendations based on individual behavior and changing life circumstances.

The beauty of this algorithmic approach is its objectivity and consistency. Unlike humans who can be swayed by emotions or biases, algorithms adhere strictly to their programmed logic, ensuring disciplined and rational investment decisions. This consistency is a cornerstone of how robo-advisors work effectively to manage wealth over the long term.

The Onboarding Journey: From Data Input to Portfolio Recommendation

The initial interaction with a robo-advisor is a crucial phase that sets the stage for your entire investment experience. Far from being a mere sign-up form, the onboarding process is a carefully designed digital interview aimed at understanding your unique financial profile, goals, and psychological comfort with risk. This information is the bedrock upon which the robo-advisor’s algorithms build your personalized investment strategy.

[INLINE IMAGE 1: place after second H2 | alt=”how do robo-advisors work concept illustration”]

Initial Questionnaire and Goal Setting: Defining Your Investment Path

The first step typically involves a detailed questionnaire. This isn’t just a formality; it’s the data input phase where you communicate your financial aspirations and current situation to the algorithm. Common questions revolve around:

- Investment Goals: Are you saving for retirement, a down payment on a house, a child’s education, or simply general wealth accumulation? Each goal has a different time horizon and potential risk profile.

- Time Horizon: When do you anticipate needing the money? A longer time horizon generally allows for more aggressive investments, as there’s more time to recover from market downturns.

- Current Financial Situation: Questions about your income, savings, debts, and existing investments help the robo-advisor understand your capacity for saving and investing.

- Knowledge of Investing: Some platforms gauge your familiarity with investment concepts to tailor explanations and recommendations appropriately.

The clarity and honesty of your answers at this stage are paramount, as they directly influence the effectiveness of the subsequent algorithmic recommendations. Many robo-advisors also allow you to set multiple goals, each with its own time horizon and risk profile, enabling a more granular approach to your financial planning.

Risk Tolerance Assessment: Gauging Your Comfort with Volatility

Perhaps the most critical component of the onboarding process is the risk tolerance assessment. This goes beyond simply asking “How much risk are you willing to take?” Robo-advisors employ various psychological and behavioral finance techniques within their questionnaires to accurately gauge your comfort level with market volatility and potential losses. Questions often probe:

- Reaction to Market Downturns: What would you do if your portfolio dropped by 10% or 20%? Would you sell, hold, or buy more?

- Investment Experience: Your past experience with investing can indicate your understanding of market fluctuations.

- Financial Stability: Individuals with stable incomes and substantial emergency funds may be more comfortable with higher risk.

- Loss Aversion: Questions designed to understand your emotional response to potential losses versus potential gains.

Based on these responses, the algorithm assigns you a risk score, which is then translated into a specific asset allocation model. A higher risk tolerance might lead to a portfolio with a larger proportion of equities (stocks), while a lower tolerance would lean towards more conservative assets like bonds and cash. It’s essential to answer these questions truthfully, as misrepresenting your risk tolerance could lead to significant discomfort during market swings or, conversely, a portfolio that doesn’t adequately grow your wealth.

Financial Profile Analysis: A Holistic View for Tailored Advice

Beyond individual goals and risk tolerance, robo-advisors also conduct a broader financial profile analysis. This involves understanding the complete picture of your financial health. This might include information about:

- Age: A significant factor in determining time horizon and risk capacity. Younger investors typically have a longer runway for recovery from market dips.

- Employment Status and Income Stability: Influences your ability to contribute regularly and weather financial shocks.

- Dependents: Financial responsibilities like children or elderly parents can impact disposable income and risk capacity.

- Existing Debts: High-interest debts (e.g., credit card debt) might suggest a more conservative approach until those are managed.

Some advanced robo-advisors integrate with your bank accounts or other financial apps to pull in real-time data, offering an even more comprehensive and dynamic understanding of your financial situation. This holistic view ensures that the investment recommendations are not just theoretically sound but practically aligned with your overall financial wellbeing.

The Algorithmic Recommendation Engine: From Data to Diversification

Once all the necessary data is collected, the robo-advisor’s algorithmic recommendation engine kicks into gear. This sophisticated software processes your goals, risk tolerance, and financial profile to generate a personalized investment portfolio. The process typically involves:

- Asset Class Selection: The algorithm identifies appropriate asset classes (e.g., U.S. stocks, international stocks, various types of bonds, real estate, commodities) based on your risk profile.

- Target Asset Allocation: It then determines the optimal percentage allocation to each asset class. For instance, a moderate investor might receive a portfolio with 60% stocks and 40% bonds.

- Fund Selection: Within each asset class, the algorithm selects specific low-cost investment vehicles, predominantly Exchange Traded Funds (ETFs) and sometimes mutual funds. These funds are chosen for their broad market exposure, low expense ratios, and alignment with the portfolio’s overall strategy.

- Portfolio Construction: The selected funds are then combined to form your diversified investment portfolio.

The entire process is designed to be efficient, objective, and grounded in proven financial principles. The output is a clear, actionable investment plan, often presented with projections and explanations of why certain assets were chosen. This seamless transition from data input to a tailored portfolio is a cornerstone of how robo-advisors deliver value to their users.

Crafting Your Digital Portfolio: Asset Allocation and Diversification

The core philosophy behind nearly every robo-advisor’s investment strategy revolves around two fundamental principles: asset allocation and diversification. These concepts, rooted deeply in modern financial theory, are not merely buzzwords but the bedrock of prudent, long-term wealth building. Robo-advisors excel at implementing these principles systematically and consistently, removing the emotional biases that often derail individual investors.

Modern Portfolio Theory in Action: The Scientific Basis

Many robo-advisors build their investment strategies on the principles of Modern Portfolio Theory (MPT), developed by Nobel laureate Harry Markowitz. MPT posits that investors can construct portfolios to maximize expected return for a given level of market risk, or conversely, minimize risk for a given level of expected return. The key insight is that the risk and return characteristics of individual assets are less important than how they behave together within a portfolio.

How MPT manifests in robo-advisor portfolios:

- Optimal Portfolios: Algorithms identify an “efficient frontier” of portfolios that offer the best possible risk-adjusted returns.

- Correlation Analysis: Investments are chosen not just for their individual potential but for how they correlate with other assets. Assets with low or negative correlations can help reduce overall portfolio volatility.

- Long-Term Horizon: MPT is a long-term strategy, aligning perfectly with the typical set-it-and-forget-it approach of robo-advisors designed for sustained growth rather than short-term speculation.

By applying MPT, robo-advisors aim to create robust portfolios that can weather various market conditions, providing a smoother ride for investors compared to concentrating investments in a few high-flying stocks.

Diversification Across Asset Classes: Spreading the Risk

Diversification is the strategy of spreading your investments across various asset classes to minimize risk. The adage “don’t put all your eggs in one basket” perfectly encapsulates this principle. Robo-advisors achieve broad diversification by investing in a range of asset classes, typically through low-cost Exchange Traded Funds (ETFs) or mutual funds.

Common asset classes included in robo-advisor portfolios:

- Domestic Equities (U.S. Stocks): Provides exposure to the growth of the U.S. economy and corporate profits.

- International Equities (Developed & Emerging Markets): Offers diversification beyond U.S. borders, tapping into global growth opportunities and reducing dependence on a single economy.

- Domestic Bonds (U.S. Bonds): Provides stability and income, acting as a buffer during stock market downturns. Includes government, corporate, and municipal bonds.

- International Bonds: Further diversifies fixed-income exposure.

- Real Estate (via REITs): Offers exposure to the real estate market without direct property ownership.

- Commodities (Less common, but some include): Such as gold, which can act as a hedge against inflation or geopolitical uncertainty.

The allocation to each asset class is dynamically adjusted based on your risk profile. A conservative investor might have a higher percentage of bonds, while a growth-oriented investor would lean more heavily into equities.

Global Market Exposure: Tapping into Worldwide Growth

One of the significant advantages of robo-advisors is their inherent ability to provide global diversification with relative ease. Rather than limiting investments to domestic markets, most platforms ensure significant exposure to international equities and bonds. This is crucial because different economies and markets perform differently over time.

Benefits of global market exposure:

- Reduced Volatility: A downturn in one country’s stock market may be offset by gains in another.

- Access to Growth: Emerging markets, in particular, can offer higher growth potential than more mature economies.

- Currency Diversification: Investing internationally can also provide exposure to different currencies, which can be beneficial during periods of currency fluctuation.

Robo-advisors typically achieve this through globally diversified ETFs that track indices in various developed and emerging markets, ensuring that your portfolio isn’t overly reliant on the performance of a single national economy.

Customization and Ethical Investing Options: Beyond the Standard Template

While often perceived as rigid, many robo-advisors offer increasing levels of customization. This is particularly evident in the growing trend of Socially Responsible Investing (SRI) or Environmental, Social, and Governance (ESG) investing. Investors who want their portfolios to reflect their values can often select portfolios that:

- Exclude certain industries: Such as fossil fuels, tobacco, or firearms.

- Focus on companies with high ESG ratings: Investing in companies demonstrating strong environmental stewardship, positive social impact, and sound corporate governance.

- Target specific impact themes: Like renewable energy or sustainable agriculture.

Furthermore, some hybrid robo-advisors or those catering to higher net worth individuals may allow for specific stock exclusions or preferences. This evolution showcases how robo-advisor technology advances to meet diverse investor needs, moving beyond a one-size-fits-all model while still maintaining the automated efficiency that defines their core service.

Automated Portfolio Management: Set It and Forget It?

Once your portfolio is constructed, the beauty of a robo-advisor truly shines through its automated management capabilities. This is where the “set it and forget it” promise largely comes to fruition, though a deeper understanding reveals a sophisticated, continuous process designed to keep your investments on track towards your goals without requiring constant manual intervention. These automated processes are key to maintaining the integrity of your investment strategy over time and optimizing returns.

[INLINE IMAGE 2: place after fourth H2 | alt=”how do robo-advisors work comparison illustration”]

Rebalancing Strategies: Maintaining Target Asset Allocation

Market fluctuations are a constant. As some investments perform better than others, your portfolio’s original asset allocation (e.g., 60% stocks, 40% bonds) will naturally drift. For instance, if stocks have a strong year, they might grow to represent 65% of your portfolio, throwing off your desired risk profile. This is where automatic rebalancing comes in.

Robo-advisors employ precise rebalancing strategies to bring your portfolio back to its target allocation. This typically happens in one of two ways:

- Time-Based Rebalancing: The portfolio is automatically rebalanced on a fixed schedule (e.g., quarterly, semi-annually, or annually). This ensures periodic realignment regardless of market conditions.

- Threshold-Based Rebalancing: The portfolio is rebalanced only when an asset class deviates by a certain percentage from its target allocation (e.g., if stocks move more than 5% above or below their target). This can be more tax-efficient as it only triggers trades when necessary.

The rebalancing process involves selling portions of assets that have grown disproportionately and buying more of those that have underperformed, effectively “trimming the winners” and “buying the dip.” This disciplined approach helps manage risk and ensures your portfolio continues to align with your long-term goals and risk tolerance, preventing it from becoming too risky or too conservative over time.

Tax-Loss Harvesting Explained: Maximizing After-Tax Returns

One of the most valuable automated features offered by many robo-advisors, especially for taxable investment accounts, is tax-loss harvesting. This sophisticated strategy aims to reduce your current year’s tax liability by selling investments at a loss to offset capital gains and, potentially, a portion of your ordinary income.

How it works:

- Identify Losses: The algorithm continuously monitors your portfolio for investments that have declined in value below their purchase price.

- Sell and Replace: If an investment shows a significant loss, the robo-advisor sells it. Immediately, it buys a similar (but not “substantially identical” to avoid wash sale rules) investment to maintain your portfolio’s asset allocation and market exposure.

- Offset Gains: The realized loss can then be used to offset any capital gains you might have from other investments.

- Offset Income: If your capital losses exceed your capital gains, you can typically use up to $3,000 of the remaining loss to offset your ordinary income each year, carrying forward any additional losses to future tax years.

Tax-loss harvesting is incredibly difficult and time-consuming for individual investors to perform manually, especially with diverse portfolios. The automation provided by robo-advisors makes this advanced tax strategy accessible and efficient, significantly enhancing after-tax returns over the long run. It’s a prime example of how robo-advisor optimization features work to your benefit.

Dividend Reinvestment: Compounding Your Growth

Many investments, particularly stocks and some ETFs, pay dividends – a portion of a company’s earnings distributed to shareholders. For long-term investors, reinvesting these dividends can be a powerful driver of compounding growth. Robo-advisors typically automate this process.

Instead of distributing dividend payments as cash, the robo-advisor automatically uses these funds to purchase additional shares of the underlying investments. This means:

- More Shares: You acquire more shares without making new contributions.

- Compounding Effect: These new shares then earn their own dividends, which are also reinvested, leading to exponential growth over time.

- No Fees: Often, there are no additional transaction fees for these small, automated purchases.

This hands-off approach ensures that every penny of your investment is continuously working for you, maximizing the power of compound interest without any effort on your part.

Performance Monitoring and Reporting: Transparency and Insights

While robo-advisors handle the day-to-day management, they also provide robust tools for monitoring your portfolio’s performance and understanding its status. Users typically have access to an online dashboard or mobile app that displays:

- Portfolio Value: Real-time or near real-time updates on your total account value.

- Performance History: Graphs and charts showing your returns over various periods (daily, monthly, annually, inception-to-date).

- Asset Allocation Breakdown: A visual representation of your current holdings across different asset classes.

- Contribution History: A record of your deposits and withdrawals.

- Fee Transparency: Clear reporting on the fees you’ve paid.

Many platforms also provide regular statements and sometimes personalized insights or educational content based on your portfolio’s performance or market events. This transparency ensures that even though the management is automated, you remain fully informed and in control of your financial journey, understanding precisely how your robo-advisor is working for you.

The Cost-Benefit Equation: Fees and Accessibility

One of the most compelling arguments for using a robo-advisor centers on its cost-effectiveness compared to traditional financial advisory services. The automated nature of these platforms significantly reduces overheads, allowing them to pass those savings on to clients in the form of lower fees. However, understanding the full cost-benefit equation requires looking beyond just the headline management fee to encompass all potential charges and the accessibility they provide.

Understanding Robo-Advisor Fee Structures: What You Pay For

Robo-advisor fees are typically structured as a percentage of assets under management (AUM) per year. This simplicity is a major selling point. While traditional advisors might charge 1% to 2% (or more) of AUM, robo-advisors generally fall into a much lower range.

Typical robo-advisor fee ranges:

- Pure Digital (Basic): 0.25% to 0.50% of AUM annually. For example, on a $10,000 portfolio, this would be $25-$50 per year.

- Hybrid (with Human Advisor Access): 0.40% to 0.89% of AUM annually. The higher fee reflects the inclusion of human guidance.

Some platforms might have tiered pricing, where the percentage fee decreases as your AUM grows. Others might offer flat monthly fees, particularly for smaller balances. It’s crucial to understand that this management fee covers the core services like portfolio creation, rebalancing, and often tax-loss harvesting.

Expense Ratios of ETFs and Funds: The Underlying Costs

Beyond the robo-advisor’s management fee, investors also incur the expense ratios of the underlying Exchange Traded Funds (ETFs) or mutual funds within their portfolio. An expense ratio is an annual fee charged by the fund itself, expressed as a percentage of the assets invested in that fund. These fees are typically very low for the passive, broadly diversified index ETFs commonly used by robo-advisors.

For example:

- A U.S. stock ETF might have an expense ratio of 0.03% to 0.07%.

- An international stock ETF might range from 0.07% to 0.20%.

- A bond ETF could be in the 0.04% to 0.15% range.

While seemingly small, these expense ratios are in addition to the robo-advisor’s AUM fee. So, if a robo-advisor charges 0.25% and your portfolio consists of ETFs with an average expense ratio of 0.10%, your total annual cost would be approximately 0.35%. Robo-advisors often emphasize using “low-cost” ETFs to minimize this additional layer of fees, ensuring that more of your money remains invested and growing.

Comparing Costs: Robo vs. Human Advisors vs. DIY

To truly appreciate the cost efficiency of robo-advisors, it’s helpful to compare their fee structures against traditional options:

| Investment Option | Typical Annual Cost | Service Level | Minimum Investment |

|---|---|---|---|

| Pure Digital Robo-Advisor | 0.25% – 0.50% AUM + low ETF expense ratios (0.05% – 0.20%) | Automated portfolio management, rebalancing, tax-loss harvesting, goal tracking. No human advice. | $0 – $500 |

| Hybrid Robo-Advisor | 0.40% – 0.89% AUM + low ETF expense ratios | All pure digital services PLUS access to human financial advisors for consultations. | $5,000 – $25,000 |

| Traditional Human Advisor | 1.00% – 2.00% AUM (or flat fee, hourly) + varying fund expense ratios | Personalized, comprehensive financial planning, investment management, behavioral coaching, estate planning. | $50,000 – $250,000+ |

| DIY Investing (Self-Directed) | Typically only ETF/fund expense ratios (0.05% – 0.20%) + potential trading commissions (if applicable) | Full control over investments, no advisory fees. Requires significant personal knowledge and time. | Varies (can be $0 with fractional shares) |

As the table illustrates, robo-advisors occupy a compelling middle ground, offering professional-grade management at a significantly lower cost than human advisors, while also providing more automation and guidance than purely DIY approaches. This accessibility makes them particularly attractive for new investors or those with smaller portfolios who might not meet the minimums for traditional services.

Minimum Investment Requirements: Lowering the Barrier to Entry

Another key aspect of accessibility is the typically low, or even non-existent, minimum investment requirements for robo-advisors. Many platforms offer accounts with a $0 minimum to start, allowing almost anyone to begin investing. Others might have modest minimums, such as $100 or $500.

This contrasts sharply with traditional financial advisors, who often require minimums of $50,000, $100,000, or even $250,000 or more. By lowering these barriers, robo-advisors have opened up the world of professional investment management to a much wider audience, fulfilling a critical role in financial inclusion. It exemplifies how fintech is democratizing investing, making wealth accumulation more attainable for everyday individuals.

Types of Robo-Advisors: Pure Digital vs. Hybrid Models

The robo-advisor landscape is not monolithic. While the core principle of automated investment management remains, different platforms cater to varying investor needs and preferences by offering distinct service models. The primary distinction lies between “pure digital” robo-advisors, which are fully automated, and “hybrid” models that integrate human financial advice, providing a spectrum of choices for investors.

Pure Digital Robo-Advisors: Full Automation and Cost Efficiency

Pure digital robo-advisors represent the foundational model of automated investing. Their services are almost entirely delivered through algorithms and technology, with minimal or no direct human interaction for investment advice. This model emphasizes efficiency, low costs, and ease of use.

Key characteristics of pure digital robo-advisors:

- Fully Automated: From portfolio construction to rebalancing and tax-loss harvesting, all investment decisions and actions are carried out by algorithms.

- Lowest Fees: Typically charge the lowest AUM fees (e.g., 0.25% to 0.50%) due to reduced overhead from human personnel.

- Lower Minimums: Often have $0 or very low minimum investment requirements, making them highly accessible.

- User-Friendly Interface: Designed for intuitive self-service via web platforms and mobile apps.

- Ideal For: Investors who are comfortable with technology, prefer a hands-off approach, have straightforward financial situations, and are primarily driven by cost efficiency. They are excellent for beginners seeking to dip their toes into investing or for seasoned investors looking for a low-cost solution for a specific goal.

Examples of pure digital robo-advisors often include platforms that pioneered the space and remain dedicated to maximizing automation to drive down costs for clients.

Hybrid Robo-Advisors: The Best of Both Worlds?

Hybrid robo-advisors blend the technological efficiency of automated investing with the personalized touch and strategic guidance of human financial advisors. This model acknowledges that while automation excels at portfolio management, some investors still value the ability to consult with a human expert for complex financial planning questions, behavioral coaching, or reassurance during turbulent markets.

Key characteristics of hybrid robo-advisors:

- Automated Management + Human Access: They provide all the automated features of a pure digital robo-advisor but add access to Certified Financial Planners (CFPs) or other qualified advisors.

- Higher Fees: Reflecting the added value of human expertise, fees are typically higher than pure digital models (e.g., 0.40% to 0.89% AUM) but still lower than traditional human-only advisors.

- Higher Minimums: Often require higher minimum investments (e.g., $5,000 to $25,000) to justify the cost of providing human access.

- Consultation Models: Human access can range from on-demand video calls to dedicated advisor relationships, depending on the platform and service tier.

- Ideal For: Investors with more complex financial situations, those who need reassurance and guidance during market volatility, individuals seeking help with broader financial planning (e.g., estate planning, college savings strategies), or those who simply prefer a human touch alongside automation.

The hybrid model caters to a significant segment of the market that seeks a balance between cost-effectiveness and personalized advice, representing a natural evolution in how robo-advisors work to meet diverse investor needs.

Niche and Specialized Robo-Advisors: Tailoring to Specific Needs

Beyond the pure digital and hybrid distinctions, the market has also seen the emergence of specialized robo-advisors that cater to specific investor needs or ethical preferences.

- Socially Responsible Investing (SRI/ESG Focus): These platforms prioritize investments in companies that meet specific environmental, social, and governance criteria, allowing investors to align their portfolios with their values.

- Faith-Based Investing: Some robo-advisors offer portfolios screened according to religious principles, such as Sharia-compliant investments.

- Specific Goal-Focused: While most offer goal-based planning, some specialize even further, such as those primarily focused on college savings (529 plans) or retirement planning.

- High-Net-Worth Offerings: A few platforms cater to affluent investors, offering more sophisticated strategies, access to alternative investments, and often a higher degree of personalization and dedicated human support, sometimes blurring the lines with family offices.

These niche players demonstrate the adaptability of the robo-advisor model, showing that the core technology can be customized to serve a broad spectrum of unique financial and ethical requirements. The evolution of these specialized services illustrates the expanding capabilities of fintech investment platforms and their ability to address specific segments of the market more effectively.

Advantages and Limitations: Weighing Your Options

Robo-advisors offer a compelling proposition for many investors, but like any financial tool, they come with a distinct set of advantages and limitations. A clear-eyed assessment of these factors is essential for determining if a robo-advisor is the right fit for your individual financial journey. Understanding both the strengths and weaknesses provides a comprehensive answer to how do robo-advisors work in practice for different people.

Key Benefits: Accessibility, Cost, Automation, Objectivity

The primary appeal of robo-advisors stems from several significant benefits:

- Accessibility:

- Low Minimums: Many platforms allow you to start investing with very little capital, sometimes as low as $0 or $100. This democratizes professional investment management, making it available to a broad audience, including young investors and those new to the market.

- Easy Setup: The onboarding process is typically straightforward and can be completed online in minutes, removing the friction often associated with opening traditional brokerage accounts.

- Cost-Effectiveness:

- Lower Fees: Annual management fees are significantly lower than those charged by traditional human financial advisors (e.g., 0.25% –

How Do Robo-Advisors Work? Unlocking the Mechanics of Automated Investing for 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

In the rapidly evolving landscape of personal finance, robo-advisors have emerged as a transformative force, democratizing access to professional investment management that was once exclusive to the wealthy. As of 2026, these digital platforms are no longer a niche offering but a mainstream solution for millions seeking efficient, low-cost ways to grow their wealth. But beyond the slick interfaces and promises of automation, a fundamental question often arises: exactly how do robo-advisors work?

This comprehensive guide from fin3go delves deep into the inner workings of robo-advisors, peeling back the layers of algorithms, technology, and financial theory that power them. We’ll explore everything from the initial user onboarding process to sophisticated portfolio management techniques like rebalancing and tax-loss harvesting. Whether you’re a seasoned investor curious about digital advancements or a newcomer looking for an accessible entry point into the market, understanding the mechanics of robo-advisors is crucial for making informed financial decisions in the modern era.

From their origins as simple automated portfolio rebalancers to their current incarnation as sophisticated financial planning tools, robo-advisors represent a significant paradigm shift. They leverage cutting-edge technology, including artificial intelligence and machine learning, to provide personalized investment advice and management at a fraction of the cost of traditional human advisors. This article aims to demystify these platforms, providing clarity on their operation, benefits, limitations, and what the future holds for automated investing.

Understanding the Core Concept of Robo-Advisors: More Than Just Automation

At its heart, a robo-advisor is a digital platform that provides automated, algorithm-driven financial planning services with little to no human supervision. The “robo” in their name signifies the automated, technology-driven nature of their operations, distinguishing them from traditional financial advisors who primarily offer face-to-face, human-led advice. However, labeling them merely as “automated” oversimplifies the intricate systems and thoughtful design that underpin their functionality. They are, in essence, a sophisticated fusion of financial wisdom and computational power.

What is a Robo-Advisor? Demystifying the Digital Financial Manager

A robo-advisor serves as a digital stand-in for a human financial advisor, but instead of relying on individual human judgment for every decision, it uses complex algorithms to manage investments. These algorithms are built upon established financial theories and principles, such as Modern Portfolio Theory (MPT), which emphasizes diversification and asset allocation. When you interact with a robo-advisor, you’re engaging with a highly programmed system designed to optimize your portfolio based on specific inputs.

Key services typically offered by a robo-advisor include:

- Automated Portfolio Creation: Based on your financial goals and risk tolerance.

- Diversified Investment Strategies: Often utilizing low-cost Exchange Traded Funds (ETFs) and mutual funds.

- Automatic Rebalancing: Adjusting your portfolio back to its target asset allocation.

- Tax Optimization: Features like tax-loss harvesting to minimize your tax liability.

- Goal-Based Planning: Helping you save for retirement, a down payment, or other life events.

Unlike traditional brokers who execute trades based on your instructions, robo-advisors take a more holistic approach, managing your portfolio proactively in alignment with your defined objectives.

The Shift from Traditional to Digital Advice: A Paradigm Change

For decades, professional financial advice was largely the domain of high-net-worth individuals, given the substantial fees and minimum asset requirements of human advisors. The advent of robo-advisors has dramatically altered this landscape. This shift wasn’t just about making advice cheaper; it was about making it accessible, convenient, and transparent for a broader demographic.

The driving forces behind this transition include:

- Technological Advancements: The proliferation of high-speed internet, powerful computing, and sophisticated algorithms made complex financial modeling feasible for mass application.

- Demand for Convenience: Modern investors, accustomed to digital interactions in other aspects of their lives, sought similar ease and accessibility for their financial management.

- Cost Efficiency: Automating many aspects of portfolio management drastically reduces overheads, allowing robo-advisors to offer services at a significantly lower cost.

- Democratization of Investing: Lower minimums and simplified processes opened the door to investing for individuals who previously found traditional services prohibitive or intimidating.

This paradigm shift has not entirely replaced human advisors but has created a complementary ecosystem where investors can choose the level of human interaction they desire, often at varying price points.

The Role of AI and Algorithms in Robo-Advisor Functionality

The “brain” of any robo-advisor lies in its sophisticated algorithms and, increasingly, artificial intelligence (AI) and machine learning (ML) capabilities. These technologies perform several critical functions:

- Risk Assessment: Algorithms analyze user responses to questionnaires to quantify risk tolerance and financial goals.

- Portfolio Construction: Based on the risk profile, algorithms select a diversified portfolio of investments designed to meet the user’s objectives.

- Market Monitoring: AI systems continuously monitor market conditions and portfolio performance.

- Automated Adjustments: Algorithms automatically trigger actions like rebalancing or tax-loss harvesting when pre-defined conditions are met.

- Personalization: While initially rule-based, newer AI models are learning to offer more nuanced recommendations based on individual behavior and changing life circumstances.

The beauty of this algorithmic approach is its objectivity and consistency. Unlike humans who can be swayed by emotions or biases, algorithms adhere strictly to their programmed logic, ensuring disciplined and rational investment decisions. This consistency is a cornerstone of how robo-advisors work effectively to manage wealth over the long term.

The Onboarding Journey: From Data Input to Portfolio Recommendation

The initial interaction with a robo-advisor is a crucial phase that sets the stage for your entire investment experience. Far from being a mere sign-up form, the onboarding process is a carefully designed digital interview aimed at understanding your unique financial profile, goals, and psychological comfort with risk. This information is the bedrock upon which the robo-advisor’s algorithms build your personalized investment strategy.

[INLINE IMAGE 1: place after second H2 | alt=”how do robo-advisors work concept illustration”]

Initial Questionnaire and Goal Setting: Defining Your Investment Path

The first step typically involves a detailed questionnaire. This isn’t just a formality; it’s the data input phase where you communicate your financial aspirations and current situation to the algorithm. Common questions revolve around:

- Investment Goals: Are you saving for retirement, a down payment on a house, a child’s education, or simply general wealth accumulation? Each goal has a different time horizon and potential risk profile.

- Time Horizon: When do you anticipate needing the money? A longer time horizon generally allows for more aggressive investments, as there’s more time to recover from market downturns.

- Current Financial Situation: Questions about your income, savings, debts, and existing investments help the robo-advisor understand your capacity for saving and investing.

- Knowledge of Investing: Some platforms gauge your familiarity with investment concepts to tailor explanations and recommendations appropriately.

The clarity and honesty of your answers at this stage are paramount, as they directly influence the effectiveness of the subsequent algorithmic recommendations. Many robo-advisors also allow you to set multiple goals, each with its own time horizon and risk profile, enabling a more granular approach to your financial planning.

Risk Tolerance Assessment: Gauging Your Comfort with Volatility

Perhaps the most critical component of the onboarding process is the risk tolerance assessment. This goes beyond simply asking “How much risk are you willing to take?” Robo-advisors employ various psychological and behavioral finance techniques within their questionnaires to accurately gauge your comfort level with market volatility and potential losses. Questions often probe:

- Reaction to Market Downturns: What would you do if your portfolio dropped by 10% or 20%? Would you sell, hold, or buy more?

- Investment Experience: Your past experience with investing can indicate your understanding of market fluctuations.

- Financial Stability: Individuals with stable incomes and substantial emergency funds may be more comfortable with higher risk.

- Loss Aversion: Questions designed to understand your emotional response to potential losses versus potential gains.

Based on these responses, the algorithm assigns you a risk score, which is then translated into a specific asset allocation model. A higher risk tolerance might lead to a portfolio with a larger proportion of equities (stocks), while a lower tolerance would lean towards more conservative assets like bonds and cash. It’s essential to answer these questions truthfully, as misrepresenting your risk tolerance could lead to significant discomfort during market swings or, conversely, a portfolio that doesn’t adequately grow your wealth.

Financial Profile Analysis: A Holistic View for Tailored Advice

Beyond individual goals and risk tolerance, robo-advisors also conduct a broader financial profile analysis. This involves understanding the complete picture of your financial health. This might include information about:

- Age: A significant factor in determining time horizon and risk capacity. Younger investors typically have a longer runway for recovery from market dips.

- Employment Status and Income Stability: Influences your ability to contribute regularly and weather financial shocks.

- Dependents: Financial responsibilities like children or elderly parents can impact disposable income and risk capacity.

- Existing Debts: High-interest debts (e.g., credit card debt) might suggest a more conservative approach until those are managed.

Some advanced robo-advisors integrate with your bank accounts or other financial apps to pull in real-time data, offering an even more comprehensive and dynamic understanding of your financial situation. This holistic view ensures that the investment recommendations are not just theoretically sound but practically aligned with your overall financial wellbeing.

The Algorithmic Recommendation Engine: From Data to Diversification

Once all the necessary data is collected, the robo-advisor’s algorithmic recommendation engine kicks into gear. This sophisticated software processes your goals, risk tolerance, and financial profile to generate a personalized investment portfolio. The process typically involves:

- Asset Class Selection: The algorithm identifies appropriate asset classes (e.g., U.S. stocks, international stocks, various types of bonds, real estate, commodities) based on your risk profile.

- Target Asset Allocation: It then determines the optimal percentage allocation to each asset class. For instance, a moderate investor might receive a portfolio with 60% stocks and 40% bonds.

- Fund Selection: Within each asset class, the algorithm selects specific low-cost investment vehicles, predominantly Exchange Traded Funds (ETFs) and sometimes mutual funds. These funds are chosen for their broad market exposure, low expense ratios, and alignment with the portfolio’s overall strategy.

- Portfolio Construction: The selected funds are then combined to form your diversified investment portfolio.

The entire process is designed to be efficient, objective, and grounded in proven financial principles. The output is a clear, actionable investment plan, often presented with projections and explanations of why certain assets were chosen. This seamless transition from data input to a tailored portfolio is a cornerstone of how robo-advisors deliver value to their users.

Crafting Your Digital Portfolio: Asset Allocation and Diversification

The core philosophy behind nearly every robo-advisor’s investment strategy revolves around two fundamental principles: asset allocation and diversification. These concepts, rooted deeply in modern financial theory, are not merely buzzwords but the bedrock of prudent, long-term wealth building. Robo-advisors excel at implementing these principles systematically and consistently, removing the emotional biases that often derail individual investors.

Modern Portfolio Theory in Action: The Scientific Basis

Many robo-advisors build their investment strategies on the principles of Modern Portfolio Theory (MPT), developed by Nobel laureate Harry Markowitz. MPT posits that investors can construct portfolios to maximize expected return for a given level of market risk, or conversely, minimize risk for a given level of expected return. The key insight is that the risk and return characteristics of individual assets are less important than how they behave together within a portfolio.

How MPT manifests in robo-advisor portfolios:

- Optimal Portfolios: Algorithms identify an “efficient frontier” of portfolios that offer the best possible risk-adjusted returns.

- Correlation Analysis: Investments are chosen not just for their individual potential but for how they correlate with other assets. Assets with low or negative correlations can help reduce overall portfolio volatility.

- Long-Term Horizon: MPT is a long-term strategy, aligning perfectly with the typical set-it-and-forget-it approach of robo-advisors designed for sustained growth rather than short-term speculation.

By applying MPT, robo-advisors aim to create robust portfolios that can weather various market conditions, providing a smoother ride for investors compared to concentrating investments in a few high-flying stocks.

Diversification Across Asset Classes: Spreading the Risk

Diversification is the strategy of spreading your investments across various asset classes to minimize risk. The adage “don’t put all your eggs in one basket” perfectly encapsulates this principle. Robo-advisors achieve broad diversification by investing in a range of asset classes, typically through low-cost Exchange Traded Funds (ETFs) or mutual funds.

Common asset classes included in robo-advisor portfolios:

- Domestic Equities (U.S. Stocks): Provides exposure to the growth of the U.S. economy and corporate profits.

- International Equities (Developed & Emerging Markets): Offers diversification beyond U.S. borders, tapping into global growth opportunities and reducing dependence on a single economy.

- Domestic Bonds (U.S. Bonds): Provides stability and income, acting as a buffer during stock market downturns. Includes government, corporate, and municipal bonds.

- International Bonds: Further diversifies fixed-income exposure.

- Real Estate (via REITs): Offers exposure to the real estate market without direct property ownership.

- Commodities (Less common, but some include): Such as gold, which can act as a hedge against inflation or geopolitical uncertainty.

The allocation to each asset class is dynamically adjusted based on your risk profile. A conservative investor might have a higher percentage of bonds, while a growth-oriented investor would lean more heavily into equities.

Global Market Exposure: Tapping into Worldwide Growth

One of the significant advantages of robo-advisors is their inherent ability to provide global diversification with relative ease. Rather than limiting investments to domestic markets, most platforms ensure significant exposure to international equities and bonds. This is crucial because different economies and markets perform differently over time.

Benefits of global market exposure:

- Reduced Volatility: A downturn in one country’s stock market may be offset by gains in another.

- Access to Growth: Emerging markets, in particular, can offer higher growth potential than more mature economies.

- Currency Diversification: Investing internationally can also provide exposure to different currencies, which can be beneficial during periods of currency fluctuation.

Robo-advisors typically achieve this through globally diversified ETFs that track indices in various developed and emerging markets, ensuring that your portfolio isn’t overly reliant on the performance of a single national economy.

Customization and Ethical Investing Options: Beyond the Standard Template

While often perceived as rigid, many robo-advisors offer increasing levels of customization. This is particularly evident in the growing trend of Socially Responsible Investing (SRI) or Environmental, Social, and Governance (ESG) investing. Investors who want their portfolios to reflect their values can often select portfolios that:

- Exclude certain industries: Such as fossil fuels, tobacco, or firearms.

- Focus on companies with high ESG ratings: Investing in companies demonstrating strong environmental stewardship, positive social impact, and sound corporate governance.

- Target specific impact themes: Like renewable energy or sustainable agriculture.

Furthermore, some hybrid robo-advisors or those catering to higher net worth individuals may allow for specific stock exclusions or preferences. This evolution showcases how robo-advisor technology advances to meet diverse investor needs, moving beyond a one-size-fits-all model while still maintaining the automated efficiency that defines their core service.

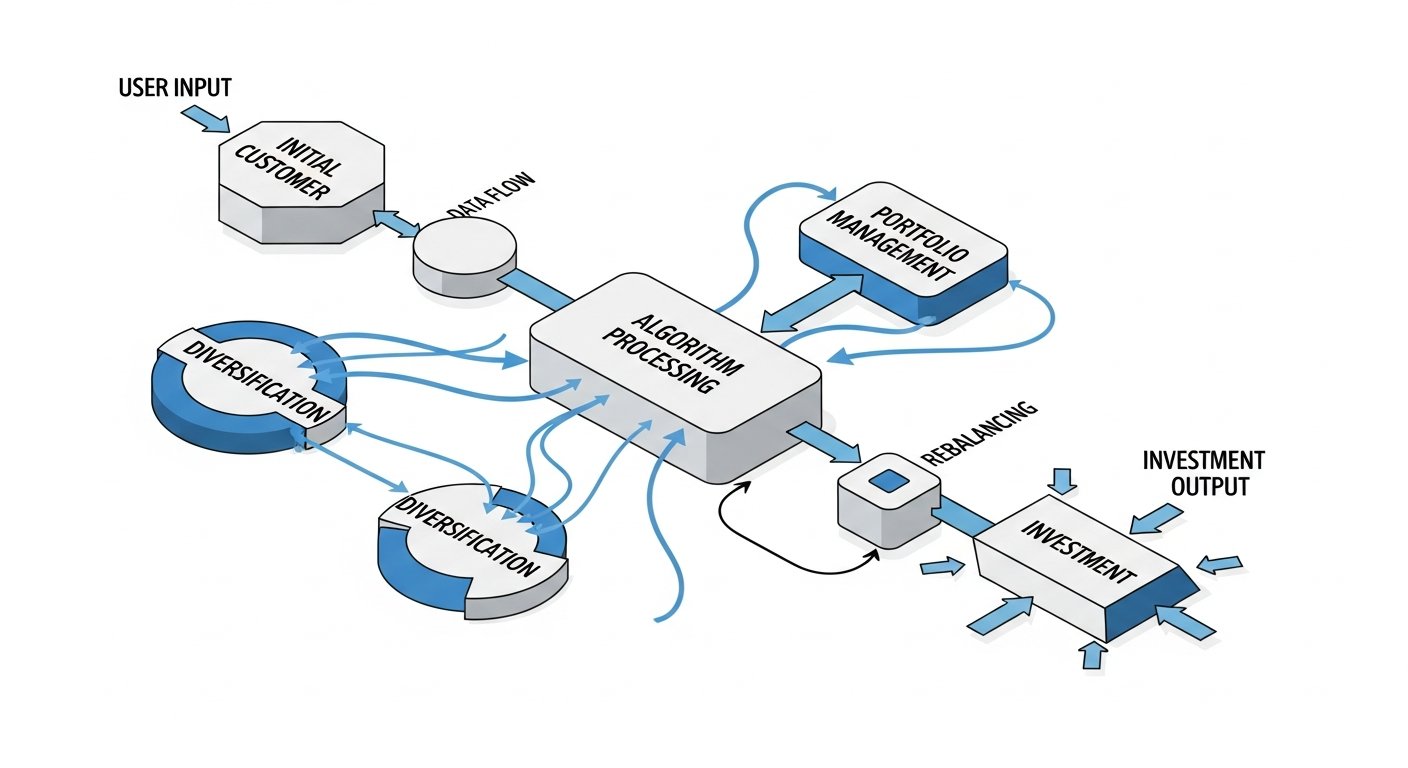

Automated Portfolio Management: Set It and Forget It?

Once your portfolio is constructed, the beauty of a robo-advisor truly shines through its automated management capabilities. This is where the “set it and forget it” promise largely comes to fruition, though a deeper understanding reveals a sophisticated, continuous process designed to keep your investments on track towards your goals without requiring constant manual intervention. These automated processes are key to maintaining the integrity of your investment strategy over time and optimizing returns.

[INLINE IMAGE 2: place after fourth H2 | alt=”how do robo-advisors work comparison illustration”]

Rebalancing Strategies: Maintaining Target Asset Allocation

Market fluctuations are a constant. As some investments perform better than others, your portfolio’s original asset allocation (e.g., 60% stocks, 40% bonds) will naturally drift. For instance, if stocks have a strong year, they might grow to represent 65% of your portfolio, throwing off your desired risk profile. This is where automatic rebalancing comes in.

Robo-advisors employ precise rebalancing strategies to bring your portfolio back to its target allocation. This typically happens in one of two ways:

- Time-Based Rebalancing: The portfolio is automatically rebalanced on a fixed schedule (e.g., quarterly, semi-annually, or annually). This ensures periodic realignment regardless of market conditions.

- Threshold-Based Rebalancing: The portfolio is rebalanced only when an asset class deviates by a certain percentage from its target allocation (e.g., if stocks move more than 5% above or below their target). This can be more tax-efficient as it only triggers trades when necessary.

The rebalancing process involves selling portions of assets that have grown disproportionately and buying more of those that have underperformed, effectively “trimming the winners” and “buying the dip.” This disciplined approach helps manage risk and ensures your portfolio continues to align with your long-term goals and risk tolerance, preventing it from becoming too risky or too conservative over time.

Tax-Loss Harvesting Explained: Maximizing After-Tax Returns

One of the most valuable automated features offered by many robo-advisors, especially for taxable investment accounts, is tax-loss harvesting. This sophisticated strategy aims to reduce your current year’s tax liability by selling investments at a loss to offset capital gains and, potentially, a portion of your ordinary income.

How it works:

- Identify Losses: The algorithm continuously monitors your portfolio for investments that have declined in value below their purchase price.

- Sell and Replace: If an investment shows a significant loss, the robo-advisor sells it. Immediately, it buys a similar (but not “substantially identical” to avoid wash sale rules) investment to maintain your portfolio’s asset allocation and market exposure.

- Offset Gains: The realized loss can then be used to offset any capital gains you might have from other investments.

- Offset Income: If your capital losses exceed your capital gains, you can typically use up to $3,000 of the remaining loss to offset your ordinary income each year, carrying forward any additional losses to future tax years.

Tax-loss harvesting is incredibly difficult and time-consuming for individual investors to perform manually, especially with diverse portfolios. The automation provided by robo-advisors makes this advanced tax strategy accessible and efficient, significantly enhancing after-tax returns over the long run. It’s a prime example of how robo-advisor optimization features work to your benefit.

Dividend Reinvestment: Compounding Your Growth

Many investments, particularly stocks and some ETFs, pay dividends – a portion of a company’s earnings distributed to shareholders. For long-term investors, reinvesting these dividends can be a powerful driver of compounding growth. Robo-advisors typically automate this process.

Instead of distributing dividend payments as cash, the robo-advisor automatically uses these funds to purchase additional shares of the underlying investments. This means:

- More Shares: You acquire more shares without making new contributions.

- Compounding Effect: These new shares then earn their own dividends, which are also reinvested, leading to exponential growth over time.

- No Fees: Often, there are no additional transaction fees for these small, automated purchases.

This hands-off approach ensures that every penny of your investment is continuously working for you, maximizing the power of compound interest without any effort on your part.

Performance Monitoring and Reporting: Transparency and Insights

While robo-advisors handle the day-to-day management, they also provide robust tools for monitoring your portfolio’s performance and understanding its status. Users typically have access to an online dashboard or mobile app that displays:

- Portfolio Value: Real-time or near real-time updates on your total account value.

- Performance History: Graphs and charts showing your returns over various periods (daily, monthly, annually, inception-to-date).

- Asset Allocation Breakdown: A visual representation of your current holdings across different asset classes.

- Contribution History: A record of your deposits and withdrawals.

- Fee Transparency: Clear reporting on the fees you’ve paid.

Many platforms also provide regular statements and sometimes personalized insights or educational content based on your portfolio’s performance or market events. This transparency ensures that even though the management is automated, you remain fully informed and in control of your financial journey, understanding precisely how your robo-advisor is working for you.

The Cost-Benefit Equation: Fees and Accessibility

One of the most compelling arguments for using a robo-advisor centers on its cost-effectiveness compared to traditional financial advisory services. The automated nature of these platforms significantly reduces overheads, allowing them to pass those savings on to clients in the form of lower fees. However, understanding the full cost-benefit equation requires looking beyond just the headline management fee to encompass all potential charges and the accessibility they provide.

Understanding Robo-Advisor Fee Structures: What You Pay For

Robo-advisor fees are typically structured as a percentage of assets under management (AUM) per year. This simplicity is a major selling point. While traditional advisors might charge 1% to 2% (or more) of AUM, robo-advisors generally fall into a much lower range.

Typical robo-advisor fee ranges:

- Pure Digital (Basic): 0.25% to 0.50% of AUM annually. For example, on a $10,000 portfolio, this would be $25-$50 per year.

- Hybrid (with Human Advisor Access): 0.40% to 0.89% of AUM annually. The higher fee reflects the inclusion of human guidance.

Some platforms might have tiered pricing, where the percentage fee decreases as your AUM grows. Others might offer flat monthly fees, particularly for smaller balances. It’s crucial to understand that this management fee covers the core services like portfolio creation, rebalancing, and often tax-loss harvesting.

Expense Ratios of ETFs and Funds: The Underlying Costs

Beyond the robo-advisor’s management fee, investors also incur the expense ratios of the underlying Exchange Traded Funds (ETFs) or mutual funds within their portfolio. An expense ratio is an annual fee charged by the fund itself, expressed as a percentage of the assets invested in that fund. These fees are typically very low for the passive, broadly diversified index ETFs commonly used by robo-advisors.

For example:

- A U.S. stock ETF might have an expense ratio of 0.03% to 0.07%.

- An international stock ETF might range from 0.07% to 0.20%.

- A bond ETF could be in the 0.04% to 0.15% range.

While seemingly small, these expense ratios are in addition to the robo-advisor’s AUM fee. So, if a robo-advisor charges 0.25% and your portfolio consists of ETFs with an average expense ratio of 0.10%, your total annual cost would be approximately 0.35%. Robo-advisors often emphasize using “low-cost” ETFs to minimize this additional layer of fees, ensuring that more of your money remains invested and growing.

Comparing Costs: Robo vs. Human Advisors vs. DIY

To truly appreciate the cost efficiency of robo-advisors, it’s helpful to compare their fee structures against traditional options:

Investment Option Typical Annual Cost Service Level Minimum Investment Pure Digital Robo-Advisor 0.25% – 0.50% AUM + low ETF expense ratios (0.05% – 0.20%) Automated portfolio management, rebalancing, tax-loss harvesting, goal tracking. No human advice. $0 – $500 Hybrid Robo-Advisor 0.40% – 0.89% AUM + low ETF expense ratios All pure digital services PLUS access to human financial advisors for consultations. $5,000 – $25,000 Traditional Human Advisor 1.00% – 2.00% AUM (or flat fee, hourly) + varying fund expense ratios Personalized, comprehensive financial planning, investment management, behavioral coaching, estate planning. $50,000 – $250,000+ DIY Investing (Self-Directed) Typically only ETF/fund expense ratios (0.05% – 0.20%) + potential trading commissions (if applicable) Full control over investments, no advisory fees. Requires significant personal knowledge and time. Varies (can be $0 with fractional shares) As the table illustrates, robo-advisors occupy a compelling middle ground, offering professional-grade management at a significantly lower cost than human advisors, while also providing more automation and guidance than purely DIY approaches. This accessibility makes them particularly attractive for new investors or those with smaller portfolios who might not meet the minimums for traditional services.

Minimum Investment Requirements: Lowering the Barrier to Entry

Another key aspect of accessibility is the typically low, or even non-existent, minimum investment requirements for robo-advisors. Many platforms offer accounts with a $0 minimum to start, allowing almost anyone to begin investing. Others might have modest minimums, such as $100 or $500.

This contrasts sharply with traditional financial advisors, who often require minimums of $50,000, $100,000, or even $250,000 or more. By lowering these barriers, robo-advisors have opened up the world of professional investment management to a much wider audience, fulfilling a critical role in financial inclusion. It exemplifies how fintech is democratizing investing, making wealth accumulation more attainable for everyday individuals.

Types of Robo-Advisors: Pure Digital vs. Hybrid Models

The robo-advisor landscape is not monolithic. While the core principle of automated investment management remains, different platforms cater to varying investor needs and preferences by offering distinct service models. The primary distinction lies between “pure digital” robo-advisors, which are fully automated, and “hybrid” models that integrate human financial advice, providing a spectrum of choices for investors.

Pure Digital Robo-Advisors: Full Automation and Cost Efficiency

Pure digital robo-advisors represent the foundational model of automated investing. Their services are almost entirely delivered through algorithms and technology, with minimal or no direct human interaction for investment advice. This model emphasizes efficiency, low costs, and ease of use.

Key characteristics of pure digital robo-advisors:

- Fully Automated: From portfolio construction to rebalancing and tax-loss harvesting, all investment decisions and actions are carried out by algorithms.

- Lowest Fees: Typically charge the lowest AUM fees (e.g., 0.25% to 0.50%) due to reduced overhead from human personnel.

- Lower Minimums: Often have $0 or very low minimum investment requirements, making them highly accessible.

- User-Friendly Interface: Designed for intuitive self-service via web platforms and mobile apps.

- Ideal For: Investors who are comfortable with technology, prefer a hands-off approach, have straightforward financial situations, and are primarily driven by cost efficiency. They are excellent for beginners seeking to dip their toes into investing or for seasoned investors looking for a low-cost solution for a specific goal.

Examples of pure digital robo-advisors often include platforms that pioneered the space and remain dedicated to maximizing automation to drive down costs for clients.

Hybrid Robo-Advisors: The Best of Both Worlds?

Hybrid robo-advisors blend the technological efficiency of automated investing with the personalized touch and strategic guidance of human financial advisors. This model acknowledges that while automation excels at portfolio management, some investors still value the ability to consult with a human expert for complex financial planning questions, behavioral coaching, or reassurance during turbulent markets.

Key characteristics of hybrid robo-advisors:

- Automated Management + Human Access: They provide all the automated features of a pure digital robo-advisor but add access to Certified Financial Planners (CFPs) or other qualified advisors.

- Higher Fees: Reflecting the added value of human expertise, fees are typically higher than pure digital models (e.g., 0.40% to 0.89% AUM) but still lower than traditional human-only advisors.

- Higher Minimums: Often require higher minimum investments (e.g., $5,000 to $25,000) to justify the cost of providing human access.

- Consultation Models: Human access can range from on-demand video calls to dedicated advisor relationships, depending on the platform and service tier.

- Ideal For: Investors with more complex financial situations, those who need reassurance and guidance during market volatility, individuals seeking help with broader financial planning (e.g., estate planning, college savings strategies), or those who simply prefer a human touch alongside automation.

The hybrid model caters to a significant segment of the market that seeks a balance between cost-effectiveness and personalized advice, representing a natural evolution in how robo-advisors work to meet diverse investor needs.

Niche and Specialized Robo-Advisors: Tailoring to Specific Needs

Beyond the pure digital and hybrid distinctions, the market has also seen the emergence of specialized robo-advisors that cater to specific investor needs or ethical preferences.

- Socially Responsible Investing (SRI/ESG Focus): These platforms prioritize investments in companies that meet specific environmental, social, and governance criteria, allowing investors to align their portfolios with their values.

- Faith-Based Investing: Some robo-advisors offer portfolios screened according to religious principles, such as Sharia-compliant investments.

- Specific Goal-Focused: While most offer goal-based planning, some specialize even further, such as those primarily focused on college savings (529 plans) or retirement planning.

- High-Net-Worth Offerings: A few platforms cater to affluent investors, offering more sophisticated strategies, access to alternative investments, and often a higher degree of personalization and dedicated human support, sometimes blurring the lines with family offices.

These niche players demonstrate the adaptability of the robo-advisor model, showing that the core technology can be customized to serve a broad spectrum of unique financial and ethical requirements. The evolution of these specialized services illustrates the expanding capabilities of fintech investment platforms and their ability to address specific segments of the market more effectively.

Advantages and Limitations: Weighing Your Options

Robo-advisors offer a compelling proposition for many investors, but like any financial tool, they come with a distinct set of advantages and limitations. A clear-eyed assessment of these factors is essential for determining if a robo-advisor is the right fit for your individual financial journey. Understanding both the strengths and weaknesses provides a comprehensive answer to how do robo-advisors work in practice for different people.

Key Benefits: Accessibility, Cost, Automation, Objectivity

The primary appeal of robo-advisors stems from several significant benefits:

- Accessibility:

- Low Minimums: Many platforms allow you to start investing with very little capital, sometimes as low as $0 or $100. This democratizes professional investment management, making it available to a broad audience, including young investors and those new to the market.

- Easy Setup: The onboarding process is typically straightforward and can be completed online in minutes, removing the friction often associated with opening traditional brokerage accounts.

- Cost-Effectiveness:

- Lower Fees: Annual management fees are significantly lower than those charged by traditional human financial advisors (e.g., 0.25% –

- Lower Fees: Annual management fees are significantly lower than those charged by traditional human financial advisors (e.g., 0.25% –