How Fintech Companies Make Money: Unpacking the Digital Finance Revenue Models of 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

The financial world has undergone a seismic shift, propelled by the relentless innovation of financial technology, or fintech. Once the exclusive domain of traditional banks and legacy institutions, financial services are now being reimagined, democratized, and delivered with unprecedented speed and accessibility thanks to a burgeoning ecosystem of fintech companies. From sleek mobile banking apps and lightning-fast payment processors to sophisticated AI-driven investment platforms and innovative lending solutions, fintech has reshaped how individuals and businesses manage their money.

But beyond the slick user interfaces and promises of convenience, a fundamental question often arises: how do fintech companies make money? Unlike traditional banks with their often transparent, albeit sometimes complex, fee structures and interest margins, fintech’s revenue generation can appear more nuanced, leveraging a diverse palette of business models. Understanding these monetization strategies is crucial not only for investors and industry insiders but also for consumers who wish to grasp the true cost and value proposition of the digital financial tools they increasingly rely upon.

This comprehensive guide delves deep into the economic engine driving the fintech revolution. We will explore the foundational pillars of fintech revenue, examine how different verticals adapt these models, and look ahead at emerging trends that will define profitability in 2026 and beyond. Prepare to uncover the intricate mechanisms that transform technological innovation into sustainable financial success.

The Foundational Pillars of Fintech Revenue Generation

At its core, every business needs a sustainable model for generating income. Fintech companies, while disruptive in their approach, are no exception. They’ve innovated on existing financial models and created entirely new ones, leveraging technology to reduce costs, expand reach, and offer superior user experiences. Here are the primary revenue streams that form the backbone of the fintech industry:

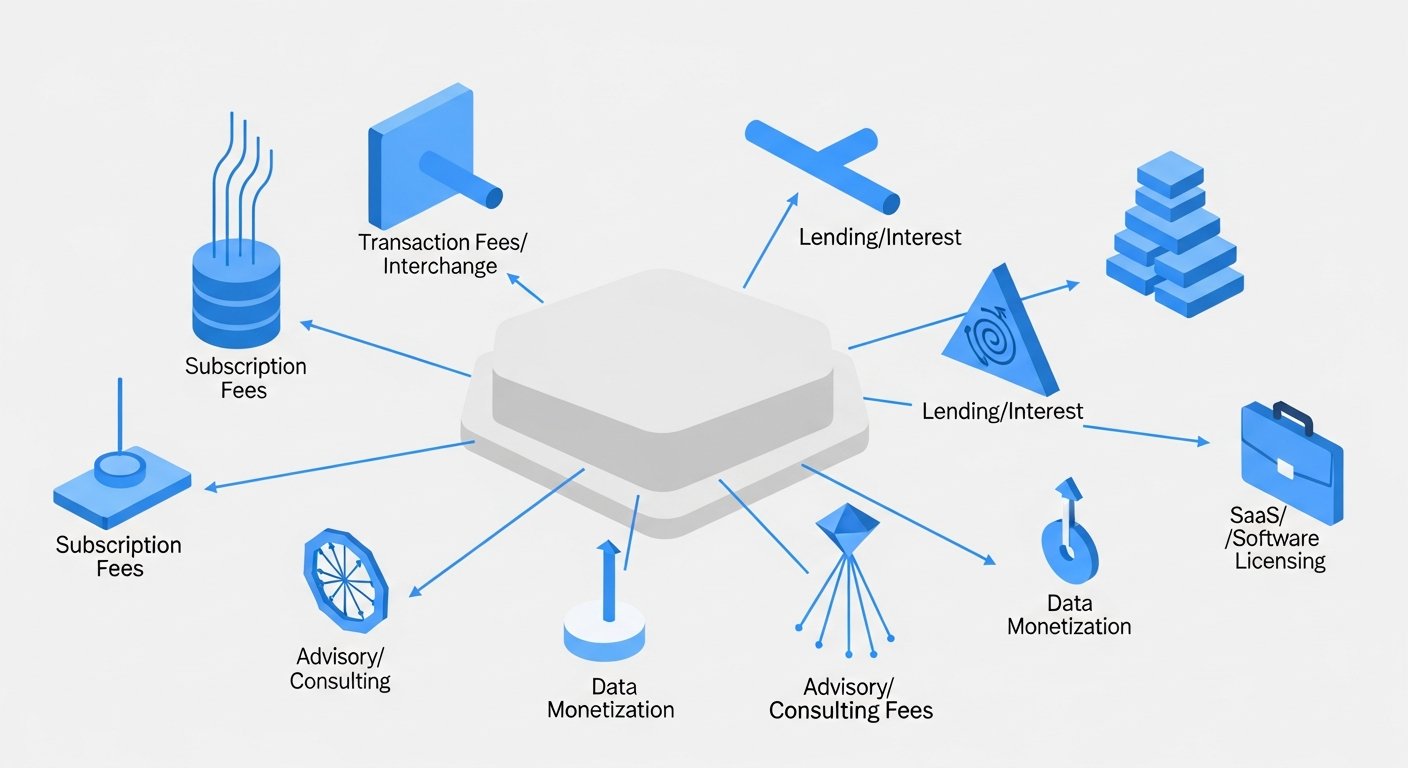

Transaction Fees: The Bread and Butter

Many fintech companies thrive on transaction volume. This is perhaps the most straightforward and pervasive monetization strategy. Every time a user executes a specific action – be it sending money, making a payment, trading a stock, or exchanging currency – the fintech company may levy a small fee. This model is particularly prevalent in:

- Payment Processors: Companies like Stripe, PayPal, and Square (Block) charge merchants a percentage of each transaction, plus a small fixed fee, for processing credit card, debit card, or digital wallet payments. These fees compensate for the service of securely facilitating money movement between parties.

- Remittance Services: Platforms facilitating international money transfers often charge a fixed fee per transfer or a percentage of the amount sent. They might also embed a slight margin in the exchange rate.

- Trading Platforms: Online brokers and cryptocurrency exchanges charge commissions on trades (though many have moved to commission-free models, monetizing through other means we’ll discuss).

The beauty of transaction fees lies in their scalability. As user adoption grows and transaction volumes increase, revenue scales proportionally, often with minimal additional overhead for each new transaction.

Subscription Models: Recurring Value for Premium Access

The subscription economy has permeated nearly every industry, and fintech is no exception. Companies offer access to premium features, enhanced services, or exclusive content in exchange for a recurring monthly or annual fee. This provides predictable revenue streams and fosters stronger customer loyalty through ongoing value delivery.

- Budgeting & Personal Finance Apps: While many offer free basic versions, premium tiers might unlock advanced budgeting tools, credit monitoring, investment insights, or ad-free experiences.

- Digital Banks (Neobanks): Some challenger banks offer tiered accounts, with higher-end subscriptions providing benefits like higher interest rates on savings, travel insurance, discounted foreign exchange rates, or metal cards.

- Investment Platforms: While basic trading might be free, subscriptions could grant access to advanced analytics, expert research, dedicated advisors, or automated tax-loss harvesting.

- SaaS for Businesses: Business-focused fintechs often charge monthly subscriptions for accounting software, payroll services, expense management platforms, or specialized payment gateways.

Subscription models emphasize long-term customer relationships, as users are motivated to retain services that consistently add value to their financial lives.

Interest Income: The Classic Financial Play Reimagined

While often associated with traditional banks, generating income from interest remains a crucial component of many fintech business models, particularly those involved in lending or holding customer deposits.

- Lending Platforms: Peer-to-peer (P2P) lenders, online personal loan providers, and small business lenders earn money by charging interest rates on the loans they originate. The spread between their funding costs (if they borrow capital) and the interest charged to borrowers forms their profit margin.

- Digital Banks & Neobanks: Like traditional banks, neobanks often earn interest on customer deposits by investing them in low-risk securities or lending them out. Some also offer high-yield savings accounts, effectively passing on a portion of this interest back to the customer to attract deposits.

- “Buy Now, Pay Later” (BNPL) Services: While some BNPL models are interest-free for consumers, many charge interest on deferred payments, especially for longer repayment periods, similar to traditional installment loans.

Fintechs leverage technology to assess credit risk more efficiently and disburse loans faster, often reaching segments underserved by traditional lenders.

Interchange Fees: Powering Payments, Quietly

If you’ve ever used a debit or credit card, you’ve indirectly contributed to interchange fees. These are small fees (a percentage of the transaction amount) paid by the merchant’s bank (the acquiring bank) to the customer’s bank (the issuing bank) whenever a card payment is processed. While not a direct fee to the consumer, these fees are a significant revenue stream for many fintechs.

- Digital Banks (Neobanks): Many neobanks issue their own debit cards. Each time a customer uses their neobank card, the neobank earns a portion of the interchange fee. This is a primary driver of profitability for many “free” digital banking accounts.

- Prepaid Card Providers: Companies that offer prepaid debit cards or virtual cards also benefit from interchange fees generated from card usage.

Interchange fees are a high-volume, low-margin business that can become very lucrative as a fintech scales its user base and card transaction volume.

Data Monetization: The New Gold

In the digital age, data is a valuable commodity. Fintech companies, by virtue of handling vast amounts of financial transaction data, gain unique insights into consumer behavior, spending patterns, and market trends. This data, often anonymized and aggregated, can be a powerful revenue source.

- Aggregated Insights for Businesses: Fintechs might sell anonymized, aggregated spending data to market research firms, retailers, or financial institutions for trend analysis and strategic planning.

- Lead Generation & Referrals: With a deep understanding of user financial profiles, fintechs can identify suitable candidates for other financial products (e.g., mortgages, insurance, new credit cards) and earn referral fees from partner institutions.

- Risk Assessment & Fraud Prevention: The data collected helps fintechs build more accurate credit scoring models and sophisticated fraud detection systems, which they can sometimes license to other businesses.

It’s critical that any data monetization adheres to stringent privacy regulations and ethical guidelines, ensuring customer trust and compliance with laws like GDPR and CCPA.

Premium Features & Upselling

Beyond explicit subscriptions, many fintechs offer a base service for free and then monetize by offering advanced features, faster processing, or additional services for an extra cost. This often takes the form of one-time fees or a freemium model.

- Expedited Transfers: While standard transfers might be free, users might pay a small fee for instant or same-day processing.

- Credit Building Tools: Some budgeting apps or credit platforms offer features like secured credit cards or direct reporting to credit bureaus for a fee.

- Virtual Card Generation: For enhanced security or spending control, generating multiple virtual cards might incur a small charge.

This strategy allows companies to acquire a large user base with a free offering and then convert a segment of those users into paying customers who value the enhanced services.

[INLINE IMAGE 1: place after second H2 | alt=”how fintech companies make money concept illustration”]

Monetization Strategies Across Key Fintech Verticals

While the foundational pillars provide a general framework, the specific application and emphasis of these revenue models vary significantly across different fintech sectors. Each vertical leverages technology to solve unique pain points and, in doing so, develops tailored monetization strategies.

Digital Banking (Neobanks) & Challenger Banks

Neobanks, or challenger banks, operate entirely online, offering banking services without physical branches. They attract customers with user-friendly apps, low fees, and innovative features. Their primary revenue sources include:

- Interchange Fees: As discussed, neobanks issue debit cards, and each time a user swipes or taps, they earn a portion of the interchange fee. This is often the largest single revenue driver for many free-tier neobanks.

- Subscription Fees: Many neobanks offer premium accounts with monthly fees that unlock benefits like higher interest on savings, cashback rewards, travel insurance, or advanced budgeting tools.

- Interest on Deposits: Like traditional banks, neobanks invest customer deposits, earning a spread between what they pay out in interest (if anything) and what they earn from their investments.

- Lending Products: As they grow, many neobanks expand into lending, offering personal loans, overdraft facilities, or credit cards, generating interest income.

- Referral Fees & Partnerships: Neobanks often partner with other financial service providers (e.g., insurance, investment platforms) and earn referral fees when their customers sign up through their platform.

- Value-Added Services (SaaS for Businesses): For business accounts, neobanks might offer paid features like integrated invoicing, payroll management, or advanced analytics.

Examples include Revolut, Chime, N26, and Monzo, each with slightly different emphasis on these revenue streams, often balancing free core services with paid premium offerings.

Lending & Credit Platforms

Fintech lending platforms use technology to streamline loan applications, accelerate credit assessment, and disburse funds more efficiently than traditional lenders. Their revenue models are generally more straightforward:

- Interest on Loans: This is the primary revenue source. Platforms charge borrowers interest on personal loans, small business loans, mortgages, or lines of credit. The interest rate varies based on the borrower’s creditworthiness and market conditions.

- Origination Fees: A one-time fee charged to the borrower at the time a loan is issued, typically a percentage of the loan amount. This covers the administrative costs of processing the loan.

- Servicing Fees: For platforms that act as servicers for loans originated by others (e.g., P2P lending platforms where individual investors fund loans), they might charge a fee for managing repayments, collections, and customer service.

- Late Fees & Penalties: While not a core revenue strategy, these fees are levied when borrowers fail to make timely payments, covering administrative costs and incentivizing prompt repayment.

- Securitization: Larger fintech lenders might package and sell their loans to institutional investors, generating revenue from the sale of these asset-backed securities.

The innovation here lies in using alternative data and AI for credit scoring, allowing them to serve segments often ignored by traditional banks or offer more competitive rates.

Explore how AI is revolutionizing credit scoring for fintech lenders.

Investment & Wealth Management (Robo-Advisors & Trading Apps)

This sector democratizes investing, making it accessible to a broader audience through automated platforms and commission-free trading. Their monetization often combines multiple approaches:

- Management Fees (AUM Fees): Robo-advisors (e.g., Betterment, Wealthfront) charge a small percentage of the assets under management (AUM) annually. This fee covers portfolio management, rebalancing, and financial planning tools. This is often their most significant revenue stream.

- Payment for Order Flow (PFOF): For “commission-free” trading apps (e.g., Robinhood), PFOF is a major revenue source. They route customer orders to market makers, who pay the broker for the opportunity to execute those trades. While controversial, it allows these platforms to offer seemingly free trading.

- Premium Subscriptions: Users might pay for access to advanced research, real-time market data, margin trading, dedicated financial advisors, or specialized investment strategies.

- Interest on Uninvested Cash: Similar to neobanks, these platforms can earn interest on customer cash balances that are awaiting investment or withdrawal.

- Lending Against Securities (Margin Lending): Some platforms offer margin accounts, allowing users to borrow against their investment portfolios, generating interest income for the platform.

- Account Fees: While less common for basic accounts, some platforms may charge fees for specific actions like wire transfers, paper statements, or inactivity.

Payments & Remittance Services

This is arguably one of the most visible fintech sectors, encompassing everything from mobile wallets to international money transfer services. Their revenue models are heavily reliant on transaction volume and added value:

- Transaction Fees: As mentioned, this is paramount. Payment processors charge merchants, and remittance services charge senders/receivers a percentage or fixed fee for each transaction.

- Foreign Exchange (FX) Spreads: For international transfers, companies often apply a small margin to the exchange rate, making money on the difference between the wholesale rate and the rate offered to the customer.

- Merchant Services Fees: Beyond basic transaction processing, providers might charge for point-of-sale (POS) hardware, software subscriptions, analytics, or fraud prevention tools offered to businesses.

- Value-Added Services: This could include loyalty programs, gift card sales, bill payment services, or even lending to merchants based on their transaction history.

- Interchange Fees: If the payment company issues its own debit or credit cards (e.g., a mobile wallet with a linked card), they earn interchange fees from card usage.

The constant drive in this sector is to make payments faster, cheaper, and more seamless, attracting a large user base to capitalize on low-margin, high-volume transactions.

Insurtech: Disrupting the Insurance Industry

Insurtech companies leverage technology to innovate how insurance products are designed, distributed, and managed. This includes everything from AI-powered risk assessment to on-demand insurance policies. Their revenue models are closely tied to the traditional insurance paradigm but enhanced by technology:

- Premiums: Directly earning money from selling insurance policies to consumers or businesses. Insurtechs aim to use better data and AI to underwrite policies more accurately, potentially reducing fraud and improving claims processing efficiency.

- Brokerage/Agency Fees: Some insurtechs act as digital brokers, earning commissions from insurance carriers for selling their policies. They often offer a more streamlined, personalized digital experience.

- Policy Management Fees (SaaS): For B2B insurtechs, this might involve charging insurance companies for software solutions that enhance policy administration, claims processing, or customer engagement.

- Data Analytics & Licensing: Companies with superior risk modeling or fraud detection algorithms might license their technology or sell anonymized data insights to other insurers.

Insurtech aims to reduce the high operational costs of traditional insurers and offer more tailored, often usage-based, insurance products, leading to more competitive pricing and new revenue opportunities.

Proptech: Innovations in Real Estate Finance

Proptech, or property technology, applies digital innovation to the real estate sector, including how properties are bought, sold, rented, managed, and financed. While a broad category, fintech aspects within proptech primarily focus on financial transactions:

- Transaction Fees: For platforms facilitating digital property transactions, fractional ownership, or online mortgage applications, a fee may be charged per successful deal.

- SaaS for Real Estate Professionals: Offering subscription-based software for property management, rental applications, virtual tours, or real estate CRM systems to agents, brokers, and landlords.

- Lending & Mortgage Brokerage: Fintechs specializing in mortgages or real estate-backed loans earn interest on these loans or collect origination fees. Digital mortgage brokers earn commissions from lenders.

- Property Investment Platforms: Platforms that allow individuals to invest in real estate (e.g., REITs, fractional ownership) may charge management fees or transaction fees on investments.

- Advisory & Valuation Services: Using AI and big data to provide more accurate property valuations or investment advice for a fee.

Proptech is simplifying complex real estate financial processes, making investment more accessible and transactions more efficient.

[INLINE IMAGE 2: place after fourth H2 | alt=”how fintech companies make money comparison illustration”]

Advanced and Emerging Monetization Models

The fintech landscape is constantly evolving, with new technologies and business models emerging to capture value in innovative ways. These advanced strategies often blur the lines between traditional financial services and cutting-edge tech.

Embedded Finance: The Invisible Revenue Stream

Embedded finance refers to the seamless integration of financial services into non-financial platforms or applications. Think about ordering a ride-share and having the payment automatically processed, or buying a product online and having a “Buy Now, Pay Later” option pop up at checkout. The monetization here often involves:

- Revenue Share: The financial service provider shares a portion of the transaction fees, interest income, or subscription revenue with the non-financial platform where the service is embedded.

- Increased Conversion & Loyalty: While not direct revenue, providing seamless financial options can boost sales and customer loyalty for the embedding platform, which in turn benefits the fintech providing the embedded service through increased usage.

- Data Insights: Embedded finance generates rich contextual data that can be monetized for personalized offers or risk assessment.

This model creates incredibly frictionless user experiences and opens vast new markets for financial products, positioning financial services as a utility rather than a standalone offering.

Banking-as-a-Service (BaaS) and Fintech-as-a-Service (FaaS)

BaaS allows non-bank businesses (fintechs or even non-financial companies) to offer banking products and services to their customers by leveraging a licensed bank’s infrastructure through APIs. FaaS extends this concept to other fintech functionalities beyond traditional banking.

- Usage-Based Fees: BaaS providers charge their clients (e.g., a neobank or a retail brand) for each API call, account created, transaction processed, or card issued.

- Subscription Fees: Clients might pay a recurring fee for access to the BaaS platform, development tools, and ongoing support.

- Revenue Share: In some cases, the BaaS provider might take a percentage of the revenue generated by the client’s financial products (e.g., a cut of interchange fees).

This model enables rapid innovation and market entry for new fintechs by significantly reducing regulatory hurdles and infrastructure costs, while the BaaS provider earns from enabling this ecosystem.

Blockchain, Cryptocurrency, and Decentralized Finance (DeFi)

This frontier of fintech uses distributed ledger technology to create transparent, immutable, and often permissionless financial systems. Monetization strategies here are still evolving but include:

- Trading Fees: Cryptocurrency exchanges charge fees for buying, selling, and swapping digital assets. These can be percentage-based or tiered.

- Staking Rewards: Users “stake” their cryptocurrency to support network operations and receive rewards, a portion of which may be facilitated and taken by a platform.

- Lending & Borrowing Protocols: DeFi platforms facilitate lending and borrowing of cryptocurrencies, earning a spread on interest rates or protocol fees.

- Liquidity Provision Fees: Decentralized exchanges (DEXs) reward users for providing liquidity to trading pairs, and the platform earns a share of transaction fees.

- NFT Royalties & Marketplace Fees: Platforms for non-fungible tokens (NFTs) earn a percentage of initial sales and secondary market royalties.

- Node Operation & Validation: Some entities earn by running validation nodes on blockchain networks, receiving network fees or newly minted tokens.

This space is characterized by rapid innovation, often driven by tokenomics and community governance models that create novel ways to generate and distribute value.

Learn more about the fundamentals of blockchain technology in finance.

AI and Machine Learning-Driven Insights

AI is not just a tool; it’s becoming a revenue driver. Fintechs are leveraging AI and ML to offer superior services, leading to new monetization opportunities:

- Predictive Analytics & Risk Scoring: Licensing advanced AI-driven credit scoring models or fraud detection systems to other financial institutions.

- Personalized Financial Advice: Offering premium access to AI-powered personalized budgeting, investment recommendations, or wealth management strategies.

- Automated Customer Support (Chatbots): While primarily a cost-saving measure, highly efficient AI support can be part of a premium service offering or reduce churn, indirectly supporting revenue.

- Algorithmic Trading & Optimization: Platforms that offer AI-driven trading strategies or portfolio optimization tools as a subscription or for a performance fee.

The ability to extract actionable insights from vast datasets and automate complex financial processes positions AI as a core component of future fintech monetization.

B2B Fintech Solutions

Many fintechs operate behind the scenes, providing critical services to other businesses, including traditional banks, small businesses, and other fintechs. Their revenue models are typically SaaS-based:

- Software-as-a-Service (SaaS): Charging recurring subscription fees for platforms that handle payroll, expense management, accounting integration, compliance management, or treasury functions.

- API Access Fees: Providing access to specialized APIs for identity verification (KYC), payment initiation, data aggregation, or regulatory reporting.

- Consulting & Implementation Services: Offering expertise and support for integrating complex fintech solutions into existing enterprise systems.

The B2B fintech market is massive, offering high-value contracts and predictable recurring revenue streams, though often requiring longer sales cycles.

Operational Costs and Profitability Challenges for Fintechs

While fintechs have innovative revenue streams, they also face unique and significant operational costs and challenges that impact their path to profitability. Understanding these expenses is crucial for assessing their long-term viability.

Customer Acquisition Costs (CAC)

Acquiring new customers in the highly competitive financial services market is expensive. Fintechs often spend heavily on digital marketing, referral programs, partnerships, and brand building to attract users away from incumbents and other challengers. High CAC can severely delay profitability, especially for companies offering low-margin or free services in their initial phase.

Regulatory Compliance and Security

Operating in the financial sector means navigating a labyrinth of regulations. Fintechs must invest heavily in legal teams, compliance officers, and robust systems to meet requirements such as anti-money laundering (AML), Know Your Customer (KYC), consumer protection, and data privacy. Furthermore, safeguarding sensitive financial data from cyber threats requires continuous investment in cutting-edge security infrastructure and expertise. Non-compliance or a security breach can lead to massive fines, reputational damage, and loss of customer trust.

Technology Infrastructure and Innovation

At their core, fintechs are technology companies. They require substantial ongoing investment in developing and maintaining their platforms, incorporating new features, scaling their infrastructure, and leveraging advanced technologies like AI and blockchain. This includes cloud computing costs, developer salaries, and R&D expenses to stay ahead in a rapidly evolving tech landscape. The expectation of seamless, always-on service means significant investment in robust, scalable, and resilient systems.

Competition and Market Saturation

The success of early fintechs has led to a flood of new entrants, intensifying competition across almost every vertical. This fierce competition often drives down prices, increases customer acquisition costs, and forces companies to continuously innovate or risk being left behind. Market saturation means that simply offering a “better app” is no longer enough; fintechs must find truly differentiated value propositions and sustainable niche markets.

The Regulatory Landscape and Its Impact on Revenue

Regulation is both a burden and a potential competitive advantage for fintechs. While compliance costs are high, navigating the regulatory maze successfully builds trust and opens doors to new markets. The global regulatory environment for fintech is complex and constantly evolving.

Navigating Licensing and Compliance

Depending on the services offered, fintechs may require various licenses (e.g., banking, lending, money transmission, investment advisory). Obtaining and maintaining these licenses is a costly and time-consuming process. Each jurisdiction often has its own set of rules, making international expansion particularly challenging. Strict compliance with these licensing requirements is non-negotiable and impacts operational scope and revenue streams.

Consumer Protection and Data Privacy (GDPR, CCPA, etc.)

Laws like the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) in the U.S. mandate stringent rules for how companies collect, store, and process personal data. For fintechs handling highly sensitive financial information, compliance with these data privacy regulations is paramount. Non-compliance can result in substantial fines and erode customer trust, directly impacting user acquisition and retention, and thus revenue potential. Ethical data monetization strategies are crucial.

Anti-Money Laundering (AML) and Know Your Customer (KYC)

Fintechs are on the front lines of combating financial crime. Robust AML and KYC procedures are mandatory to prevent illicit activities like money laundering and terrorist financing. Investing in advanced identity verification technologies, transaction monitoring systems, and dedicated compliance teams is a significant operational cost but also a legal imperative. Failure to comply can lead to severe penalties and even the cessation of operations.

Open Banking and API Regulations

Initiatives like Open Banking (prevalent in the UK and Europe) mandate that traditional banks securely share customer financial data with third-party fintechs (with customer consent) via APIs. This creates opportunities for fintechs to build innovative new services based on aggregated financial data, such as personalized budgeting tools or lending platforms with richer credit insights. While it fosters innovation and creates new revenue avenues, it also introduces new regulatory complexities around data access, security, and consent management.

Understand the impact of Open Banking on personal finance.

Comparative Analysis: Traditional Finance vs. Fintech Revenue Models

To truly appreciate how fintech companies make money, it’s insightful to compare their approaches with the established models of traditional financial institutions. While there’s increasing convergence, fundamental differences persist.

Efficiency and Scalability

Traditional Finance: Often burdened by legacy infrastructure, extensive branch networks, and manual processes. Their scalability is typically linear, requiring significant capital investment (e.g., opening new branches) to expand services. Revenue models often rely on higher margins per transaction or customer.

Fintech: Built on cloud-native infrastructure, leveraging APIs and automation. They boast superior operational efficiency and often achieve exponential scalability with minimal additional cost per user, especially for digital-only services. Their revenue models often thrive on high volume and lower individual margins.

Customer Experience and Retention

Traditional Finance: Customer experience can be inconsistent, often requiring physical visits for complex issues. Retention relies on established brand trust and bundled services, sometimes making it difficult for customers to switch.

Fintech: Prioritize intuitive, mobile-first user interfaces and instant digital support. They aim for seamless experiences, attracting and retaining customers through convenience, personalization, and competitive pricing. Customer loyalty can be high if the value proposition is strong, but switching costs are often lower.

Risk Management Approaches

Traditional Finance: Rely on historical data, established credit bureaus, and often a more conservative approach to risk, sometimes leading to exclusion of certain customer segments.

Fintech: Utilize alternative data sources, machine learning, and AI for real-time risk assessment, allowing for more granular and often more inclusive lending or underwriting. This can lead to better risk-adjusted returns or access to new markets, though it also presents new challenges in model validation and bias detection.

Future Trajectories

Traditional Finance: Increasingly investing in digital transformation, acquiring fintechs, or partnering with them to remain competitive. Their future involves hybrid models, combining physical presence with digital capabilities.

Fintech: Many are maturing, seeking sustainable profitability beyond rapid growth. Their future involves deeper integration into the broader economy (embedded finance), expansion into B2B services, and navigating an increasingly complex regulatory landscape as they grow into systemically important institutions.

Here’s a simplified comparison of typical revenue models:

| Revenue Model | Traditional Banks (Typical Focus) | Fintech Companies (Typical Focus) | Key Differentiator |

|---|---|---|---|

| Interest Income | High on loans (mortgages, business loans), low on deposits. Significant net interest margin. | High on specific lending products, often leveraging alternative data. Interest on deposits for neobanks. | Fintechs use technology for faster, more granular risk assessment and lower overhead. |

| Transaction Fees | Account maintenance fees, ATM fees, overdraft fees, wire transfer fees. | Interchange fees (neobanks), payment processing fees (merchants), remittance fees, trading commissions (some platforms). | Fintechs focus on high-volume, low-margin digital transactions; traditional banks on more sporadic, higher-fee services. |

| Subscription/Advisory Fees | Wealth management fees for high-net-worth clients, premium account tiers. | Premium app features, robo-advisor AUM fees, SaaS for B2B solutions. | Fintechs democratize premium features and services for a broader audience. |

| Data Monetization | Limited direct monetization, primarily for internal risk and marketing. | Anonymized data analytics for market insights, lead generation, risk modeling. | Fintechs are digital-first, making data collection and analysis a core asset. |

| Value-Added Services | Insurance, investment products through subsidiaries, financial planning. | Embedded finance, BaaS, API licensing, specific tools for niche markets. | Fintechs integrate services seamlessly into user journeys, often through partnerships. |

The Future of Fintech Monetization: Trends to Watch in 2026 and Beyond

The fintech industry is a dynamic ecosystem, and its revenue models are continually evolving. Looking ahead to 2026 and beyond, several key trends will shape how these companies generate profit.

Hyper-Personalization and AI

The ability to deliver hyper-personalized financial products and advice, powered by AI and machine learning, will become a significant differentiator and monetization opportunity. Fintechs will move beyond generic offerings to anticipate individual needs, offering tailored savings goals, personalized investment strategies, and proactive financial health nudges. This level of personalization can command premium fees or significantly boost retention and usage of core services, indirectly increasing transaction-based revenue.

Sustainability and ESG Fintech

As environmental, social, and governance (ESG) concerns grow in importance, fintechs that integrate sustainability into their core offerings will attract a new generation of conscious consumers and investors. Monetization could come from premium features that track carbon footprint, investment products focused on green companies, or certifications for sustainable business practices. Fintech platforms enabling impact investing or transparent donation processing will also see increased traction, potentially earning platform fees.

Global Expansion and Cross-Border Payments

The demand for fast, affordable, and transparent cross-border payments and financial services will continue to accelerate. Fintechs specializing in international remittances, multi-currency accounts, and global B2B payments will capitalize on this trend. Their revenue will come from transaction fees, favorable exchange rate spreads, and potentially premium subscriptions for businesses needing advanced international treasury management tools. Emerging markets, in particular, offer immense untapped potential for fintech expansion.

The Evolution of Embedded Finance

Embedded finance is still in its nascent stages. In the future, financial services will become so deeply integrated into everyday life that they become almost invisible. This means more diverse revenue-sharing agreements between fintech providers and non-financial platforms across retail, healthcare, automotive, and other industries. The focus will shift from selling standalone financial products to facilitating seamless financial experiences, with monetization tied to the value generated within those experiences rather than explicit financial transactions.

Discover the latest innovations in embedded finance applications.

Regulatory Sandboxes and Innovation

Regulatory bodies worldwide are increasingly establishing “sandboxes” or innovation hubs to allow fintechs to test new products and services in a controlled environment. This collaborative approach can accelerate market entry for novel business models and reduce compliance costs in the initial stages. As regulations adapt to innovation, more clarity will emerge, potentially fostering new, government-sanctioned monetization opportunities for groundbreaking fintech solutions.

Conclusion: The Dynamic and Profitable World of Fintech

The question of “how fintech companies make money” reveals a fascinating landscape of innovation, strategic adaptation, and technological prowess. From the foundational pillars of transaction and subscription fees to the intricate webs of embedded finance and the burgeoning opportunities in blockchain, fintechs are redefining profitability in the financial sector.

Their success hinges on leveraging technology to offer superior user experiences, greater efficiency, and more personalized services, often at a lower cost than traditional incumbents. While challenges such as high customer acquisition costs, intense competition, and a complex regulatory environment persist, the industry’s agility and relentless pursuit of innovation suggest a bright and continually evolving future.

As we move through 2026 and beyond, fintech will continue to reshape personal finance, banking, credit, and investments. Understanding their diverse revenue models provides critical insight into the forces driving this transformation, empowering both consumers and industry professionals to navigate the digital financial landscape with greater clarity and confidence. The fintech revolution isn’t just about technological change; it’s about fundamentally rethinking how value is created, exchanged, and sustained in

How Fintech Companies Make Money: Unpacking the Digital Finance Revenue Models of 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

The financial world has undergone a seismic shift, propelled by the relentless innovation of financial technology, or fintech. Once the exclusive domain of traditional banks and legacy institutions, financial services are now being reimagined, democratized, and delivered with unprecedented speed and accessibility thanks to a burgeoning ecosystem of fintech companies. From sleek mobile banking apps and lightning-fast payment processors to sophisticated AI-driven investment platforms and innovative lending solutions, fintech has reshaped how individuals and businesses manage their money.

But beyond the slick user interfaces and promises of convenience, a fundamental question often arises: how do fintech companies make money? Unlike traditional banks with their often transparent, albeit sometimes complex, fee structures and interest margins, fintech’s revenue generation can appear more nuanced, leveraging a diverse palette of business models. Understanding these monetization strategies is crucial not only for investors and industry insiders but also for consumers who wish to grasp the true cost and value proposition of the digital financial tools they increasingly rely upon.

This comprehensive guide delves deep into the economic engine driving the fintech revolution. We will explore the foundational pillars of fintech revenue, examine how different verticals adapt these models, and look ahead at emerging trends that will define profitability in 2026 and beyond. Prepare to uncover the intricate mechanisms that transform technological innovation into sustainable financial success.

The Foundational Pillars of Fintech Revenue Generation

At its core, every business needs a sustainable model for generating income. Fintech companies, while disruptive in their approach, are no exception. They’ve innovated on existing financial models and created entirely new ones, leveraging technology to reduce costs, expand reach, and offer superior user experiences. Here are the primary revenue streams that form the backbone of the fintech industry:

Transaction Fees: The Bread and Butter

Many fintech companies thrive on transaction volume. This is perhaps the most straightforward and pervasive monetization strategy. Every time a user executes a specific action – be it sending money, making a payment, trading a stock, or exchanging currency – the fintech company may levy a small fee. This model is particularly prevalent in:

- Payment Processors: Companies like Stripe, PayPal, and Square (Block) charge merchants a percentage of each transaction, plus a small fixed fee, for processing credit card, debit card, or digital wallet payments. These fees compensate for the service of securely facilitating money movement between parties.

- Remittance Services: Platforms facilitating international money transfers often charge a fixed fee per transfer or a percentage of the amount sent. They might also embed a slight margin in the exchange rate.

- Trading Platforms: Online brokers and cryptocurrency exchanges charge commissions on trades (though many have moved to commission-free models, monetizing through other means we’ll discuss).

The beauty of transaction fees lies in their scalability. As user adoption grows and transaction volumes increase, revenue scales proportionally, often with minimal additional overhead for each new transaction.

Subscription Models: Recurring Value for Premium Access

The subscription economy has permeated nearly every industry, and fintech is no exception. Companies offer access to premium features, enhanced services, or exclusive content in exchange for a recurring monthly or annual fee. This provides predictable revenue streams and fosters stronger customer loyalty through ongoing value delivery.

- Budgeting & Personal Finance Apps: While many offer free basic versions, premium tiers might unlock advanced budgeting tools, credit monitoring, investment insights, or ad-free experiences.

- Digital Banks (Neobanks): Some challenger banks offer tiered accounts, with higher-end subscriptions providing benefits like higher interest rates on savings, travel insurance, discounted foreign exchange rates, or metal cards.

- Investment Platforms: While basic trading might be free, subscriptions could grant access to advanced analytics, expert research, dedicated advisors, or automated tax-loss harvesting.

- SaaS for Businesses: Business-focused fintechs often charge monthly subscriptions for accounting software, payroll services, expense management platforms, or specialized payment gateways.

Subscription models emphasize long-term customer relationships, as users are motivated to retain services that consistently add value to their financial lives.

Interest Income: The Classic Financial Play Reimagined

While often associated with traditional banks, generating income from interest remains a crucial component of many fintech business models, particularly those involved in lending or holding customer deposits.

- Lending Platforms: Peer-to-peer (P2P) lenders, online personal loan providers, and small business lenders earn money by charging interest rates on the loans they originate. The spread between their funding costs (if they borrow capital) and the interest charged to borrowers forms their profit margin.

- Digital Banks & Neobanks: Like traditional banks, neobanks often earn interest on customer deposits by investing them in low-risk securities or lending them out. Some also offer high-yield savings accounts, effectively passing on a portion of this interest back to the customer to attract deposits.

- “Buy Now, Pay Later” (BNPL) Services: While some BNPL models are interest-free for consumers, many charge interest on deferred payments, especially for longer repayment periods, similar to traditional installment loans.

Fintechs leverage technology to assess credit risk more efficiently and disburse loans faster, often reaching segments underserved by traditional lenders.

Interchange Fees: Powering Payments, Quietly

If you’ve ever used a debit or credit card, you’ve indirectly contributed to interchange fees. These are small fees (a percentage of the transaction amount) paid by the merchant’s bank (the acquiring bank) to the customer’s bank (the issuing bank) whenever a card payment is processed. While not a direct fee to the consumer, these fees are a significant revenue stream for many fintechs.

- Digital Banks (Neobanks): Many neobanks issue their own debit cards. Each time a customer uses their neobank card, the neobank earns a portion of the interchange fee. This is a primary driver of profitability for many “free” digital banking accounts.

- Prepaid Card Providers: Companies that offer prepaid debit cards or virtual cards also benefit from interchange fees generated from card usage.

Interchange fees are a high-volume, low-margin business that can become very lucrative as a fintech scales its user base and card transaction volume.

Data Monetization: The New Gold

In the digital age, data is a valuable commodity. Fintech companies, by virtue of handling vast amounts of financial transaction data, gain unique insights into consumer behavior, spending patterns, and market trends. This data, often anonymized and aggregated, can be a powerful revenue source.

- Aggregated Insights for Businesses: Fintechs might sell anonymized, aggregated spending data to market research firms, retailers, or financial institutions for trend analysis and strategic planning.

- Lead Generation & Referrals: With a deep understanding of user financial profiles, fintechs can identify suitable candidates for other financial products (e.g., mortgages, insurance, new credit cards) and earn referral fees from partner institutions.

- Risk Assessment & Fraud Prevention: The data collected helps fintechs build more accurate credit scoring models and sophisticated fraud detection systems, which they can sometimes license to other businesses.

It’s critical that any data monetization adheres to stringent privacy regulations and ethical guidelines, ensuring customer trust and compliance with laws like GDPR and CCPA.

Premium Features & Upselling

Beyond explicit subscriptions, many fintechs offer a base service for free and then monetize by offering advanced features, faster processing, or additional services for an extra cost. This often takes the form of one-time fees or a freemium model.

- Expedited Transfers: While standard transfers might be free, users might pay a small fee for instant or same-day processing.

- Credit Building Tools: Some budgeting apps or credit platforms offer features like secured credit cards or direct reporting to credit bureaus for a fee.

- Virtual Card Generation: For enhanced security or spending control, generating multiple virtual cards might incur a small charge.

This strategy allows companies to acquire a large user base with a free offering and then convert a segment of those users into paying customers who value the enhanced services.

[INLINE IMAGE 1: place after second H2 | alt=”how fintech companies make money concept illustration”]

Monetization Strategies Across Key Fintech Verticals

While the foundational pillars provide a general framework, the specific application and emphasis of these revenue models vary significantly across different fintech sectors. Each vertical leverages technology to solve unique pain points and, in doing so, develops tailored monetization strategies.

Digital Banking (Neobanks) & Challenger Banks

Neobanks, or challenger banks, operate entirely online, offering banking services without physical branches. They attract customers with user-friendly apps, low fees, and innovative features. Their primary revenue sources include:

- Interchange Fees: As discussed, neobanks issue debit cards, and each time a user swipes or taps, they earn a portion of the interchange fee. This is often the largest single revenue driver for many free-tier neobanks.

- Subscription Fees: Many neobanks offer premium accounts with monthly fees that unlock benefits like higher interest on savings, cashback rewards, travel insurance, or advanced budgeting tools.

- Interest on Deposits: Like traditional banks, neobanks invest customer deposits, earning a spread between what they pay out in interest (if anything) and what they earn from their investments.

- Lending Products: As they grow, many neobanks expand into lending, offering personal loans, overdraft facilities, or credit cards, generating interest income.

- Referral Fees & Partnerships: Neobanks often partner with other financial service providers (e.g., insurance, investment platforms) and earn referral fees when their customers sign up through their platform.

- Value-Added Services (SaaS for Businesses): For business accounts, neobanks might offer paid features like integrated invoicing, payroll management, or advanced analytics.

Examples include Revolut, Chime, N26, and Monzo, each with slightly different emphasis on these revenue streams, often balancing free core services with paid premium offerings.

Lending & Credit Platforms

Fintech lending platforms use technology to streamline loan applications, accelerate credit assessment, and disburse funds more efficiently than traditional lenders. Their revenue models are generally more straightforward:

- Interest on Loans: This is the primary revenue source. Platforms charge borrowers interest on personal loans, small business loans, mortgages, or lines of credit. The interest rate varies based on the borrower’s creditworthiness and market conditions.

- Origination Fees: A one-time fee charged to the borrower at the time a loan is issued, typically a percentage of the loan amount. This covers the administrative costs of processing the loan.

- Servicing Fees: For platforms that act as servicers for loans originated by others (e.g., P2P lending platforms where individual investors fund loans), they might charge a fee for managing repayments, collections, and customer service.

- Late Fees & Penalties: While not a core revenue strategy, these fees are levied when borrowers fail to make timely payments, covering administrative costs and incentivizing prompt repayment.

- Securitization: Larger fintech lenders might package and sell their loans to institutional investors, generating revenue from the sale of these asset-backed securities.

The innovation here lies in using alternative data and AI for credit scoring, allowing them to serve segments often ignored by traditional banks or offer more competitive rates.

Explore how AI is revolutionizing credit scoring for fintech lenders.

Investment & Wealth Management (Robo-Advisors & Trading Apps)

This sector democratizes investing, making it accessible to a broader audience through automated platforms and commission-free trading. Their monetization often combines multiple approaches:

- Management Fees (AUM Fees): Robo-advisors (e.g., Betterment, Wealthfront) charge a small percentage of the assets under management (AUM) annually. This fee covers portfolio management, rebalancing, and financial planning tools. This is often their most significant revenue stream.

- Payment for Order Flow (PFOF): For “commission-free” trading apps (e.g., Robinhood), PFOF is a major revenue source. They route customer orders to market makers, who pay the broker for the opportunity to execute those trades. While controversial, it allows these platforms to offer seemingly free trading.

- Premium Subscriptions: Users might pay for access to advanced research, real-time market data, margin trading, dedicated financial advisors, or specialized investment strategies.

- Interest on Uninvested Cash: Similar to neobanks, these platforms can earn interest on customer cash balances that are awaiting investment or withdrawal.

- Lending Against Securities (Margin Lending): Some platforms offer margin accounts, allowing users to borrow against their investment portfolios, generating interest income for the platform.

- Account Fees: While less common for basic accounts, some platforms may charge fees for specific actions like wire transfers, paper statements, or inactivity.

Payments & Remittance Services

This is arguably one of the most visible fintech sectors, encompassing everything from mobile wallets to international money transfer services. Their revenue models are heavily reliant on transaction volume and added value:

- Transaction Fees: As mentioned, this is paramount. Payment processors charge merchants, and remittance services charge senders/receivers a percentage or fixed fee for each transaction.

- Foreign Exchange (FX) Spreads: For international transfers, companies often apply a small margin to the exchange rate, making money on the difference between the wholesale rate and the rate offered to the customer.

- Merchant Services Fees: Beyond basic transaction processing, providers might charge for point-of-sale (POS) hardware, software subscriptions, analytics, or fraud prevention tools offered to businesses.

- Value-Added Services: This could include loyalty programs, gift card sales, bill payment services, or even lending to merchants based on their transaction history.

- Interchange Fees: If the payment company issues its own debit or credit cards (e.g., a mobile wallet with a linked card), they earn interchange fees from card usage.

The constant drive in this sector is to make payments faster, cheaper, and more seamless, attracting a large user base to capitalize on low-margin, high-volume transactions.

Insurtech: Disrupting the Insurance Industry

Insurtech companies leverage technology to innovate how insurance products are designed, distributed, and managed. This includes everything from AI-powered risk assessment to on-demand insurance policies. Their revenue models are closely tied to the traditional insurance paradigm but enhanced by technology:

- Premiums: Directly earning money from selling insurance policies to consumers or businesses. Insurtechs aim to use better data and AI to underwrite policies more accurately, potentially reducing fraud and improving claims processing efficiency.

- Brokerage/Agency Fees: Some insurtechs act as digital brokers, earning commissions from insurance carriers for selling their policies. They often offer a more streamlined, personalized digital experience.

- Policy Management Fees (SaaS): For B2B insurtechs, this might involve charging insurance companies for software solutions that enhance policy administration, claims processing, or customer engagement.

- Data Analytics & Licensing: Companies with superior risk modeling or fraud detection algorithms might license their technology or sell anonymized data insights to other insurers.

Insurtech aims to reduce the high operational costs of traditional insurers and offer more tailored, often usage-based, insurance products, leading to more competitive pricing and new revenue opportunities.

Proptech: Innovations in Real Estate Finance

Proptech, or property technology, applies digital innovation to the real estate sector, including how properties are bought, sold, rented, managed, and financed. While a broad category, fintech aspects within proptech primarily focus on financial transactions:

- Transaction Fees: For platforms facilitating digital property transactions, fractional ownership, or online mortgage applications, a fee may be charged per successful deal.

- SaaS for Real Estate Professionals: Offering subscription-based software for property management, rental applications, virtual tours, or real estate CRM systems to agents, brokers, and landlords.

- Lending & Mortgage Brokerage: Fintechs specializing in mortgages or real estate-backed loans earn interest on these loans or collect origination fees. Digital mortgage brokers earn commissions from lenders.

- Property Investment Platforms: Platforms that allow individuals to invest in real estate (e.g., REITs, fractional ownership) may charge management fees or transaction fees on investments.

- Advisory & Valuation Services: Using AI and big data to provide more accurate property valuations or investment advice for a fee.

Proptech is simplifying complex real estate financial processes, making investment more accessible and transactions more efficient.

[INLINE IMAGE 2: place after fourth H2 | alt=”how fintech companies make money comparison illustration”]

Advanced and Emerging Monetization Models

The fintech landscape is constantly evolving, with new technologies and business models emerging to capture value in innovative ways. These advanced strategies often blur the lines between traditional financial services and cutting-edge tech.

Embedded Finance: The Invisible Revenue Stream

Embedded finance refers to the seamless integration of financial services into non-financial platforms or applications. Think about ordering a ride-share and having the payment automatically processed, or buying a product online and having a “Buy Now, Pay Later” option pop up at checkout. The monetization here often involves:

- Revenue Share: The financial service provider shares a portion of the transaction fees, interest income, or subscription revenue with the non-financial platform where the service is embedded.

- Increased Conversion & Loyalty: While not direct revenue, providing seamless financial options can boost sales and customer loyalty for the embedding platform, which in turn benefits the fintech providing the embedded service through increased usage.

- Data Insights: Embedded finance generates rich contextual data that can be monetized for personalized offers or risk assessment.

This model creates incredibly frictionless user experiences and opens vast new markets for financial products, positioning financial services as a utility rather than a standalone offering.

Banking-as-a-Service (BaaS) and Fintech-as-a-Service (FaaS)

BaaS allows non-bank businesses (fintechs or even non-financial companies) to offer banking products and services to their customers by leveraging a licensed bank’s infrastructure through APIs. FaaS extends this concept to other fintech functionalities beyond traditional banking.

- Usage-Based Fees: BaaS providers charge their clients (e.g., a neobank or a retail brand) for each API call, account created, transaction processed, or card issued.

- Subscription Fees: Clients might pay a recurring fee for access to the BaaS platform, development tools, and ongoing support.

- Revenue Share: In some cases, the BaaS provider might take a percentage of the revenue generated by the client’s financial products (e.g., a cut of interchange fees).

This model enables rapid innovation and market entry for new fintechs by significantly reducing regulatory hurdles and infrastructure costs, while the BaaS provider earns from enabling this ecosystem.

Blockchain, Cryptocurrency, and Decentralized Finance (DeFi)

This frontier of fintech uses distributed ledger technology to create transparent, immutable, and often permissionless financial systems. Monetization strategies here are still evolving but include:

- Trading Fees: Cryptocurrency exchanges charge fees for buying, selling, and swapping digital assets. These can be percentage-based or tiered.

- Staking Rewards: Users “stake” their cryptocurrency to support network operations and receive rewards, a portion of which may be facilitated and taken by a platform.

- Lending & Borrowing Protocols: DeFi platforms facilitate lending and borrowing of cryptocurrencies, earning a spread on interest rates or protocol fees.

- Liquidity Provision Fees: Decentralized exchanges (DEXs) reward users for providing liquidity to trading pairs, and the platform earns a share of transaction fees.

- NFT Royalties & Marketplace Fees: Platforms for non-fungible tokens (NFTs) earn a percentage of initial sales and secondary market royalties.

- Node Operation & Validation: Some entities earn by running validation nodes on blockchain networks, receiving network fees or newly minted tokens.

This space is characterized by rapid innovation, often driven by tokenomics and community governance models that create novel ways to generate and distribute value.

Learn more about the fundamentals of blockchain technology in finance.

AI and Machine Learning-Driven Insights

AI is not just a tool; it’s becoming a revenue driver. Fintechs are leveraging AI and ML to offer superior services, leading to new monetization opportunities:

- Predictive Analytics & Risk Scoring: Licensing advanced AI-driven credit scoring models or fraud detection systems to other financial institutions.

- Personalized Financial Advice: Offering premium access to AI-powered personalized budgeting, investment recommendations, or wealth management strategies.

- Automated Customer Support (Chatbots): While primarily a cost-saving measure, highly efficient AI support can be part of a premium service offering or reduce churn, indirectly supporting revenue.

- Algorithmic Trading & Optimization: Platforms that offer AI-driven trading strategies or portfolio optimization tools as a subscription or for a performance fee.

The ability to extract actionable insights from vast datasets and automate complex financial processes positions AI as a core component of future fintech monetization.

B2B Fintech Solutions

Many fintechs operate behind the scenes, providing critical services to other businesses, including traditional banks, small businesses, and other fintechs. Their revenue models are typically SaaS-based:

- Software-as-a-Service (SaaS): Charging recurring subscription fees for platforms that handle payroll, expense management, accounting integration, compliance management, or treasury functions.

- API Access Fees: Providing access to specialized APIs for identity verification (KYC), payment initiation, data aggregation, or regulatory reporting.

- Consulting & Implementation Services: Offering expertise and support for integrating complex fintech solutions into existing enterprise systems.

The B2B fintech market is massive, offering high-value contracts and predictable recurring revenue streams, though often requiring longer sales cycles.

Operational Costs and Profitability Challenges for Fintechs

While fintechs have innovative revenue streams, they also face unique and significant operational costs and challenges that impact their path to profitability. Understanding these expenses is crucial for assessing their long-term viability.

Customer Acquisition Costs (CAC)

Acquiring new customers in the highly competitive financial services market is expensive. Fintechs often spend heavily on digital marketing, referral programs, partnerships, and brand building to attract users away from incumbents and other challengers. High CAC can severely delay profitability, especially for companies offering low-margin or free services in their initial phase.

Regulatory Compliance and Security

Operating in the financial sector means navigating a labyrinth of regulations. Fintechs must invest heavily in legal teams, compliance officers, and robust systems to meet requirements such as anti-money laundering (AML), Know Your Customer (KYC), consumer protection, and data privacy. Furthermore, safeguarding sensitive financial data from cyber threats requires continuous investment in cutting-edge security infrastructure and expertise. Non-compliance or a security breach can lead to massive fines, reputational damage, and loss of customer trust.

Technology Infrastructure and Innovation

At their core, fintechs are technology companies. They require substantial ongoing investment in developing and maintaining their platforms, incorporating new features, scaling their infrastructure, and leveraging advanced technologies like AI and blockchain. This includes cloud computing costs, developer salaries, and R&D expenses to stay ahead in a rapidly evolving tech landscape. The expectation of seamless, always-on service means significant investment in robust, scalable, and resilient systems.

Competition and Market Saturation

The success of early fintechs has led to a flood of new entrants, intensifying competition across almost every vertical. This fierce competition often drives down prices, increases customer acquisition costs, and forces companies to continuously innovate or risk being left behind. Market saturation means that simply offering a “better app” is no longer enough; fintechs must find truly differentiated value propositions and sustainable niche markets.

The Regulatory Landscape and Its Impact on Revenue

Regulation is both a burden and a potential competitive advantage for fintechs. While compliance costs are high, navigating the regulatory maze successfully builds trust and opens doors to new markets. The global regulatory environment for fintech is complex and constantly evolving.

Navigating Licensing and Compliance

Depending on the services offered, fintechs may require various licenses (e.g., banking, lending, money transmission, investment advisory). Obtaining and maintaining these licenses is a costly and time-consuming process. Each jurisdiction often has its own set of rules, making international expansion particularly challenging. Strict compliance with these licensing requirements is non-negotiable and impacts operational scope and revenue streams.

Consumer Protection and Data Privacy (GDPR, CCPA, etc.)

Laws like the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) in the U.S. mandate stringent rules for how companies collect, store, and process personal data. For fintechs handling highly sensitive financial information, compliance with these data privacy regulations is paramount. Non-compliance can result in substantial fines and erode customer trust, directly impacting user acquisition and retention, and thus revenue potential. Ethical data monetization strategies are crucial.

Anti-Money Laundering (AML) and Know Your Customer (KYC)

Fintechs are on the front lines of combating financial crime. Robust AML and KYC procedures are mandatory to prevent illicit activities like money laundering and terrorist financing. Investing in advanced identity verification technologies, transaction monitoring systems, and dedicated compliance teams is a significant operational cost but also a legal imperative. Failure to comply can lead to severe penalties and even the cessation of operations.

Open Banking and API Regulations

Initiatives like Open Banking (prevalent in the UK and Europe) mandate that traditional banks securely share customer financial data with third-party fintechs (with customer consent) via APIs. This creates opportunities for fintechs to build innovative new services based on aggregated financial data, such as personalized budgeting tools or lending platforms with richer credit insights. While it fosters innovation and creates new revenue avenues, it also introduces new regulatory complexities around data access, security, and consent management.

Understand the impact of Open Banking on personal finance.

Comparative Analysis: Traditional Finance vs. Fintech Revenue Models

To truly appreciate how fintech companies make money, it’s insightful to compare their approaches with the established models of traditional financial institutions. While there’s increasing convergence, fundamental differences persist.

Efficiency and Scalability

Traditional Finance: Often burdened by legacy infrastructure, extensive branch networks, and manual processes. Their scalability is typically linear, requiring significant capital investment (e.g., opening new branches) to expand services. Revenue models often rely on higher margins per transaction or customer.

Fintech: Built on cloud-native infrastructure, leveraging APIs and automation. They boast superior operational efficiency and often achieve exponential scalability with minimal additional cost per user, especially for digital-only services. Their revenue models often thrive on high volume and lower individual margins.

Customer Experience and Retention

Traditional Finance: Customer experience can be inconsistent, often requiring physical visits for complex issues. Retention relies on established brand trust and bundled services, sometimes making it difficult for customers to switch.

Fintech: Prioritize intuitive, mobile-first user interfaces and instant digital support. They aim for seamless experiences, attracting and retaining customers through convenience, personalization, and competitive pricing. Customer loyalty can be high if the value proposition is strong, but switching costs are often lower.

Risk Management Approaches

Traditional Finance: Rely on historical data, established credit bureaus, and often a more conservative approach to risk, sometimes leading to exclusion of certain customer segments.

Fintech: Utilize alternative data sources, machine learning, and AI for real-time risk assessment, allowing for more granular and often more inclusive lending or underwriting. This can lead to better risk-adjusted returns or access to new markets, though it also presents new challenges in model validation and bias detection.

Future Trajectories

Traditional Finance: Increasingly investing in digital transformation, acquiring fintechs, or partnering with them to remain competitive. Their future involves hybrid models, combining physical presence with digital capabilities.

Fintech: Many are maturing, seeking sustainable profitability beyond rapid growth. Their future involves deeper integration into the broader economy (embedded finance), expansion into B2B services, and navigating an increasingly complex regulatory landscape as they grow into systemically important institutions.

Here’s a simplified comparison of typical revenue models:

| Revenue Model | Traditional Banks (Typical Focus) | Fintech Companies (Typical Focus) | Key Differentiator |

|---|---|---|---|

| Interest Income | High on loans (mortgages, business loans), low on deposits. Significant net interest margin. | High on specific lending products, often leveraging alternative data. Interest on deposits for neobanks. | Fintechs use technology for faster, more granular risk assessment and lower overhead. |

| Transaction Fees | Account maintenance fees, ATM fees, overdraft fees, wire transfer fees. | Interchange fees (neobanks), payment processing fees (merchants), remittance fees, trading commissions (some platforms). | Fintechs focus on high-volume, low-margin digital transactions; traditional banks on more sporadic, higher-fee services. |

| Subscription/Advisory Fees | Wealth management fees for high-net-worth clients, premium account tiers. | Premium app features, robo-advisor AUM fees, SaaS for B2B solutions. | Fintechs democratize premium features and services for a broader audience. |

| Data Monetization | Limited direct monetization, primarily for internal risk and marketing. | Anonymized data analytics for market insights, lead generation, risk modeling. | Fintechs are digital-first, making data collection and analysis a core asset. |

| Value-Added Services | Insurance, investment products through subsidiaries, financial planning. | Embedded finance, BaaS, API licensing, specific tools for niche markets. | Fintechs integrate services seamlessly into user journeys, often through partnerships. |

The Future of Fintech Monetization: Trends to Watch in 2026 and Beyond

The fintech industry is a dynamic ecosystem, and its revenue models are continually evolving. Looking ahead to 2026 and beyond, several key trends will shape how these companies generate profit.

Hyper-Personalization and AI

The ability to deliver hyper-personalized financial products and advice, powered by AI and machine learning, will become a significant differentiator and monetization opportunity. Fintechs will move beyond generic offerings to anticipate individual needs, offering tailored savings goals, personalized investment strategies, and proactive financial health nudges. This level of personalization can command premium fees or significantly boost retention and usage of core services, indirectly increasing transaction-based revenue.

Sustainability and ESG Fintech

As environmental, social, and governance (ESG) concerns grow in importance, fintechs that integrate sustainability into their core offerings will attract a new generation of conscious consumers and investors. Monetization could come from premium features that track carbon footprint, investment products focused on green companies, or certifications for sustainable business practices. Fintech platforms enabling impact investing or transparent donation processing will also see increased traction, potentially earning platform fees.

Global Expansion and Cross-Border Payments

The demand for fast, affordable, and transparent cross-border payments and financial services will continue to accelerate. Fintechs specializing in international remittances, multi-currency accounts, and global B2B payments will capitalize on this trend. Their revenue will come from transaction fees, favorable exchange rate spreads, and potentially premium subscriptions for businesses needing advanced international treasury management tools. Emerging markets, in particular, offer immense untapped potential for fintech expansion.

The Evolution of Embedded Finance

Embedded finance is still in its nascent stages. In the future, financial services will become so deeply integrated into everyday life that they become almost invisible. This means more diverse revenue-sharing agreements between fintech providers and non-financial platforms across retail, healthcare, automotive, and other industries. The focus will shift from selling standalone financial products to facilitating seamless financial experiences, with monetization tied to the value generated within those experiences rather than explicit financial transactions.

Discover the latest innovations in embedded finance applications.

Regulatory Sandboxes and Innovation

Regulatory bodies worldwide are increasingly establishing “sandboxes” or innovation hubs to allow fintechs to test new products and services in a controlled environment. This collaborative approach can accelerate market entry for novel business models and reduce compliance costs in the initial stages. As regulations adapt to innovation, more clarity will emerge, potentially fostering new, government-sanctioned monetization opportunities for groundbreaking fintech solutions.

Conclusion: The Dynamic and Profitable World of Fintech

The question of “how fintech companies make money” reveals a fascinating landscape of innovation, strategic adaptation, and technological prowess. From the foundational pillars of transaction and subscription fees to the intricate webs of embedded finance and the burgeoning opportunities in blockchain, fintechs are redefining profitability in the financial sector.

Their success hinges on leveraging technology to offer superior user experiences, greater efficiency, and more personalized services, often at a lower cost than traditional incumbents. While challenges such as high customer acquisition costs, intense competition, and a complex regulatory environment persist, the industry’s agility and relentless pursuit of innovation suggest a bright and continually evolving future.

As we move through 2026 and beyond, fintech will continue to reshape personal finance, banking, credit, and investments. Understanding their diverse revenue models provides critical insight into the forces driving this transformation, empowering both consumers and industry professionals to navigate the digital financial landscape with greater clarity and confidence. The fintech revolution isn’t just about technological change; it’s about fundamentally rethinking how value is created, exchanged, and sustained in