What Exactly is Zero-Based Budgeting?

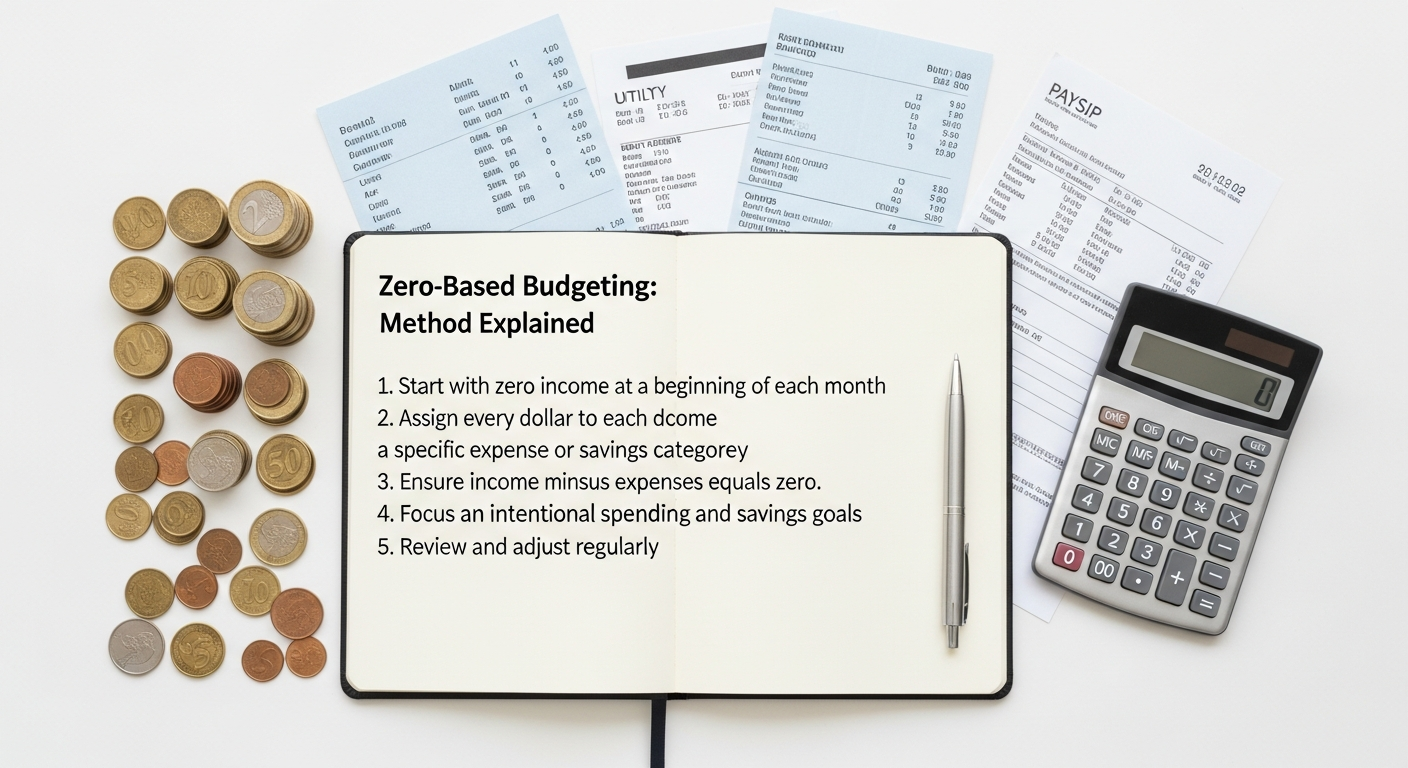

At its heart, the zero-based budgeting method is an approach where every dollar of income is assigned a specific job or category, resulting in your income minus your expenses equaling zero. Unlike traditional budgeting, which often starts with previous spending habits and adjusts them, ZBB begins each budgeting period (typically monthly) with a “blank slate” – a metaphorical zero. This means you justify every single expense, from your rent and groceries to your morning coffee and entertainment subscriptions, as if you were building your budget from scratch each time.

The core principle is simple yet profound: give every dollar a purpose. When your income for the month is $4,000, your budget must allocate that entire $4,000 across various categories – bills, savings, debt payments, discretionary spending – until nothing is left unaccounted for. This isn’t about spending all your money; it’s about intentionality. If you have $500 left after covering all your necessities and wants, that $500 doesn’t just sit in your checking account; it’s assigned a job, perhaps to an emergency fund, a specific savings goal, or an extra debt payment. The goal is not to have money left over at the end of the month, but to have allocated all your money purposefully at the beginning of the month.

This method forces a proactive stance on your finances. Instead of reacting to where your money went, you decide where it will go. It encourages a deep dive into your spending habits, questioning the necessity and value of every outflow. For Fin3go readers, accustomed to leveraging fintech for financial empowerment, zero-based budgeting provides the perfect strategic framework to maximize the utility of advanced tracking apps and automated savings tools. It’s a powerful tool for anyone looking to gain granular control over their finances, reduce financial anxiety, and accelerate their journey towards financial freedom.

The Core Principles and Philosophy Behind Zero-Based Budgeting

Beyond the simple equation of income – expenses = 0, zero-based budgeting is underpinned by several powerful principles that drive its effectiveness and make it a transformative personal finance strategy.

1. Intentionality and Purposeful Spending

The most fundamental principle of ZBB is intentionality. Every dollar you earn is a resource, and ZBB demands that you consciously decide its fate. This contrasts sharply with reactive spending, where money often dissipates without clear direction. With ZBB, you become the architect of your financial life, dictating where your money will go rather than wondering where it went. This purposeful allocation ensures that your spending aligns directly with your values and financial goals, whether that’s saving for a down payment, paying off student loans, or building an investment portfolio.

2. Justification for Every Expense

Another cornerstone of zero-based budgeting is the requirement to justify every expense. When you start from zero each month, you’re not simply carrying over last month’s budget categories and amounts. Instead, you’re asking yourself, “Do I really need this expense this month? Is this the best use of these funds?” This constant questioning acts as a powerful deterrent against automatic, unexamined spending. It encourages you to scrutinize subscriptions you no longer use, identify areas where you can cut back, and proactively look for ways to optimize your spending – perhaps by exploring methods for How To Negotiate Bills And Lower Expenses, for instance.

3. Proactive Planning Over Reactive Tracking

Traditional budgeting often involves tracking spending after it happens, providing a rearview mirror view of your finances. ZBB, however, is a forward-looking strategy. You plan where your money will go before the month begins, setting a clear roadmap for your financial actions. This proactive approach minimizes financial surprises and helps you anticipate potential shortfalls or surpluses, allowing you to make adjustments before they become problems. It shifts your mindset from merely observing your money to actively directing it.

4. Empowerment and Control

The philosophy of ZBB is deeply empowering. By giving every dollar a job, you gain an unprecedented level of control over your finances. This control translates into reduced financial stress and increased confidence. You know exactly where you stand, what you’re working towards, and how each financial decision impacts your overall plan. This sense of mastery over your money is a significant psychological benefit, fostering a healthier and more positive relationship with your financial resources.

5. Focus on Current Needs, Not Past Habits

ZBB encourages you to base your budget on your current financial reality and needs, rather not simply replicating past spending habits. Life changes – incomes fluctuate, priorities shift, and unexpected events occur. By starting from zero, you’re forced to reassess your budget in light of your present circumstances, ensuring that your financial plan is always relevant and optimized for your current situation. This adaptability is crucial for navigating the ever-changing landscape of personal finance effectively.

Embracing these principles means more than just balancing a ledger; it means cultivating a mindset of financial discipline, awareness, and intentionality that serves as a robust foundation for achieving any financial goal, from short-term savings to long-term wealth building.

Step-by-Step Guide: How to Implement Zero-Based Budgeting in Your Life

Step 1: Calculate Your Total Income

The very first step is to accurately determine how much money you expect to receive during the budgeting period, typically a month. This includes:

- Net Income: Your take-home pay after taxes, deductions, and contributions. If you have a variable income, consider using a conservative estimate or an average of the last few months.

- Other Income Sources: Freelance earnings, side hustles, rental income, alimony, child support, or any other regular income.

Be precise. This figure is the total amount you have available to allocate for the month. Let’s call this your “income pot.”

Step 2: List All Your Expenses

Now, create a comprehensive list of every single expense you anticipate for the month. This is where you dig deep. Think about:

- Fixed Expenses: These are usually the same amount each month. Examples include rent/mortgage, loan payments (car, student), insurance premiums, and subscriptions (Netflix, gym).

- Variable Expenses: These fluctuate from month to month. Examples include groceries, utilities (electricity, water, gas), transportation (gas, public transport), and dining out.

- Discretionary Expenses: These are non-essential but contribute to your quality of life. Examples include entertainment, hobbies, personal care, shopping, and gifts.

- Irregular Expenses: These don’t occur monthly but are predictable (e.g., annual car registration, semi-annual insurance payments). It’s wise to budget a small amount each month into a dedicated savings category for these.

Don’t forget to consider methods like How To Negotiate Bills And Lower Expenses during this step. Can you call your internet provider for a better rate? Can you switch insurance companies? Every dollar saved here is a dollar that can be put towards a more impactful goal.

Step 3: Assign Every Dollar a Job

This is the core of zero-based budgeting. Go through your list of expenses and assign a specific amount of money from your “income pot” to each category. Think of yourself as giving each dollar a task. Prioritize ruthlessly:

- Needs First: Allocate funds for essential living expenses like housing, food, utilities, transportation, and minimum debt payments.

- Savings and Debt Acceleration: Once needs are covered, allocate funds towards your financial goals. This could be building an emergency fund, saving for a down payment, retirement contributions, or making extra payments on high-interest debt.

- Wants and Discretionary Spending: Finally, allocate funds for your wants, such as entertainment, dining out, hobbies, and personal shopping. Be realistic, but also be prepared to make tough choices if your “wants” exceed your remaining funds.

The key here is that every dollar of your income must be assigned. If you have money left over after covering all your planned expenses, don’t just leave it unassigned. Give it a job! Perhaps it goes into an emergency fund, a specific savings goal, or an investment account. The goal is that your total income minus your total allocated expenses equals zero.

Step 4: Balance Your Budget (Income – Expenses = 0)

This step is critical. Add up all your assigned expenses and savings allocations. Compare this total to your total income.

- If your income – expenses > 0 (you have money left over): Go back and assign that remaining money a job. Put it towards extra debt payments, boost your savings goals, or create a new savings category.

- If your income – expenses < 0 (you’ve overspent your income): This means you’ve allocated more money than you have. You must go back and make cuts. Look at your discretionary spending first. Can you reduce dining out? Postpone a purchase? Find cheaper alternatives? This is often the hardest part, but it forces you to make conscious choices.

Keep adjusting until your income minus your total allocations equals exactly zero. This iterative process is what makes ZBB so powerful.

Step 5: Track and Adjust Regularly

Your budget isn’t a static document; it’s a living guide. Throughout the month:

- Track Your Spending: Use a spreadsheet, a budgeting app, or even pen and paper to record every transaction. Compare your actual spending to your budgeted amounts.

- Review and Adjust: At least once a week, and definitely at the end of the month, review your budget. Did you overspend in one category? Underspend in another? Life happens, and your budget needs to be flexible. If you have an unexpected expense, you’ll need to “roll with the punches” and adjust other categories to accommodate it, always striving to get back to zero. This regular review process is essential for maintaining control and ensures your budget remains relevant, much like the ongoing process of How To Create A Monthly Budget.

By diligently following these steps, you’ll transform your financial life from reactive to proactive, gaining unparalleled clarity and control over your money.

The Transformative Benefits of Zero-Based Budgeting

Adopting the zero-based budgeting method offers a cascade of benefits that extend far beyond simply balancing your books. It’s a transformative approach that can fundamentally alter your financial trajectory and overall well-being.

1. Unparalleled Financial Awareness and Clarity

One of the immediate and most profound benefits of ZBB is the crystal-clear picture it provides of your financial situation. By meticulously assigning every dollar, you gain an intimate understanding of where your money comes from and, more importantly, where every cent is going. This eliminates the “mystery” of disappearing funds and replaces it with a deep sense of awareness. You’ll know your true spending habits, identify financial leaks, and understand the real cost of your lifestyle choices.

2. Elimination of Wasteful Spending

Because ZBB requires you to justify every expense from scratch, it naturally exposes and helps eliminate wasteful spending. Those forgotten subscriptions, unused gym memberships, or impulse purchases become glaringly obvious when you have to explicitly budget for them. This constant scrutiny encourages you to cut out non-essential expenses, reallocate funds to more impactful areas, and truly question the value you receive for every dollar spent. It’s a powerful tool for optimizing your cash flow.

3. Accelerated Debt Repayment

For those burdened by debt, ZBB can be a game-changer. By identifying surplus funds and intentionally allocating them to debt repayment (e.g., student loans, credit card balances), you can significantly accelerate your path to becoming debt-free. The “every dollar has a job” philosophy ensures that any money not explicitly needed for necessities or savings is put to work against your liabilities, reducing interest paid and freeing up future cash flow faster.

4. Boosted Savings and Investment Potential

Just as ZBB accelerates debt repayment, it also supercharges your savings and investment efforts. When you deliberately assign funds to an emergency fund, retirement accounts, or specific savings goals (like a down payment on a house or a dream vacation), those goals become tangible and prioritized. There’s no “leftover” money that might be accidentally spent; instead, every dollar is intentionally directed towards building your financial future. This intentionality is a key ingredient for How To Build Generational Wealth, as it lays the foundation for consistent saving and strategic investing.

5. Greater Control and Reduced Financial Stress

The proactive nature of zero-based budgeting provides an immense sense of control over your finances. You are no longer a passive observer but an active manager of your money. This control translates directly into reduced financial stress and anxiety. Knowing exactly where you stand, having a plan for every dollar, and anticipating future financial needs can bring significant peace of mind, allowing you to focus on other aspects of your life without constant money worries.

6. Better Alignment of Spending with Values

ZBB forces you to confront your financial priorities. When you decide where every dollar goes, you’re essentially deciding what matters most to you. Do you value experiences over material possessions? Long-term security over immediate gratification? ZBB helps you align your spending with your core values, ensuring your money is supporting the life you truly want to live, rather than simply funding habits or external pressures.

In essence, zero-based budgeting isn’t just a method for managing money; it’s a strategic framework for mastering your financial life, leading to greater freedom, security, and the ability to achieve your most ambitious financial aspirations in 2026 and beyond.

Challenges and Considerations When Adopting ZBB

While the zero-based budgeting method offers significant advantages, it’s not without its challenges. Being aware of these potential hurdles can help you prepare and navigate them successfully.

1. Initial Time Commitment and Effort

The most common challenge is the significant time and effort required upfront. Creating your first zero-based budget involves a meticulous review of all your income sources and every single expense. This can be a lengthy process, especially if you haven’t tracked your spending closely before. It demands patience and a willingness to dig deep into your financial habits. However, this initial investment pays dividends in the long run through increased financial clarity.

2. Potential for Rigidity and Over-Categorization

Some users find ZBB to be overly rigid. If you create too many granular categories or try to stick to your budget with absolute inflexibility, it can feel restrictive and lead to frustration. Life is unpredictable, and unexpected expenses or changes in plans are inevitable. The key is to build flexibility into your budget, perhaps through a “miscellaneous” or “buffer” category, and to be willing to adjust your allocations throughout the month without feeling like you’ve failed.

3. Dealing with Unexpected Expenses

The “every dollar has a job” philosophy can make unexpected expenses seem particularly disruptive. If your car breaks down or an emergency vet bill arises, you’ll need to reallocate funds from other categories to cover it, which can be stressful. This highlights the critical importance of having a robust emergency fund before fully optimizing your zero-based budget. A well-funded emergency savings account acts as a buffer, preventing unexpected costs from derailing your entire monthly plan.

4. Maintaining Consistency and Motivation

Like any new habit, maintaining consistency with ZBB can be challenging. It requires regular tracking, review, and adjustment. The initial enthusiasm might wane, and it can be tempting to revert to less rigorous methods. Staying motivated often comes from seeing the positive results – reduced debt, increased savings, and a greater sense of control. Finding a budgeting tool that works for you and having an accountability partner can also help maintain momentum.

5. Variable Income Fluctuations

For individuals with variable income (e.g., freelancers, commission-based sales, gig workers), ZBB can present unique complexities. Accurately estimating monthly income to reach that “zero” balance can be difficult. Strategies for variable income earners include budgeting with a conservative income estimate, prioritizing essential expenses first, and using any income above the estimate to fund savings goals or future expenses.

6. Psychological Resistance to Scrutiny

For some, the deep dive into every expense can feel uncomfortable or even judgmental. Confronting spending habits, especially those driven by emotion or convenience, requires a level of self-awareness and discipline that not everyone is immediately comfortable with. Overcoming this resistance involves reframing the process as an act of self-care and empowerment, rather than deprivation.

Acknowledging these challenges upfront allows you to approach zero-based budgeting with realistic expectations and proactive strategies to overcome obstacles, ensuring a more sustainable and successful implementation.

Practical Tips for ZBB Success in 2026 and Beyond

Mastering the zero-based budgeting method requires more than just understanding its mechanics; it demands consistency, adaptability, and the right tools. Here are practical tips to help you achieve lasting success with ZBB in 2026 and for years to come:

1. Embrace Budgeting Tools and Apps

While a spreadsheet can work, modern budgeting apps (many of which are fintech-enabled) can significantly streamline the ZBB process. Look for apps that allow you to easily categorize transactions, track spending against your budget, and visualize your financial progress. Many offer features like automatic transaction import and goal tracking, making it easier to see where your money is going and ensure every dollar has a job. Experiment with a few to find one that aligns with your preferences and makes the process enjoyable, not a chore.

2. Automate Savings and Bill Payments

Once you’ve assigned specific jobs to your dollars, automate as much as possible. Set up automatic transfers from your checking account to your savings accounts (emergency fund, investment accounts, specific goals) immediately after you get paid. Similarly, automate bill payments for fixed expenses like rent, utilities, and loan payments. Automation ensures that your budgeted allocations actually happen, reducing the temptation to dip into funds meant for savings or debt repayment.

3. Build an Emergency Fund First (or Simultaneously)

Before you get too aggressive with optimizing every last dollar, prioritize building a foundational emergency fund. Aim for at least 3-6 months of essential living expenses. This fund acts as your safety net, absorbing unexpected costs without derailing your meticulously planned zero-based budget. If an emergency arises, you can draw from this fund rather than having to scramble and reallocate funds from categories like groceries or rent, which can be incredibly stressful.

4. Review and Adjust Your Budget Monthly (or Even Weekly)

Your budget is a living document, not a static decree. Life happens, and your financial situation can change. Make it a habit to review your budget at the end of each month, or even more frequently if your spending is highly variable. What worked last month might not work this month. Be prepared to adjust categories, reallocate funds, and learn from your spending patterns. This flexibility prevents frustration and ensures your budget remains a relevant and useful tool, embodying the iterative process of How To Create A Monthly Budget.

5. Involve Household Members

If you share finances with a partner or family, involve them in the zero-based budgeting process. Open communication about financial goals, income, and expenses is crucial for success. When everyone understands and agrees on where the money is going, it fosters teamwork and reduces potential conflict over spending decisions. Regular “budget meetings” can be a great way to stay aligned.

6. Be Patient and Persistent

You won’t master zero-based budgeting overnight. The first few months might feel challenging, and you’ll likely make mistakes or misjudge allocations. Don’t get discouraged! View each month as a learning opportunity. Persistence is key. The more you practice, the more intuitive and efficient the process becomes. Celebrate small wins, learn from setbacks, and keep refining your approach.

7. Use a “Buffer” or “Miscellaneous” Category

To prevent rigidity and accommodate minor unexpected expenses or slight miscalculations, consider including a small “buffer” or “miscellaneous” category in your budget. This allows for a small degree of flexibility without completely throwing off your “income – expenses = 0” equation. Just be mindful not to let this category become a dumping ground for unexamined spending.

8. Connect Your Budget to Your Long-Term Goals

Always remember why you’re budgeting. Whether it’s to pay off debt, save for a down payment, invest for retirement, or even pursue ambitious goals like How To Build Generational Wealth, connecting your monthly allocations to these larger aspirations will provide the motivation needed to stick with ZBB. Seeing how each dollar contributes to your bigger picture makes the effort worthwhile.

By integrating these practical tips, you can transform the zero-based budgeting method from a mere financial exercise into a powerful habit that propels you towards financial mastery and security in 2026 and for all your years to come.

Frequently Asked Questions About Zero-Based Budgeting

What is the main difference between zero-based budgeting and traditional budgeting?

The main difference lies in the starting point and philosophy. Traditional budgeting often starts by looking at past spending and adjusting it, allowing for “leftover” money that might be spent without a clear purpose. Zero-based budgeting (ZBB), on the other hand, starts from zero each month, requiring every dollar of income to be intentionally assigned a job (expense, saving, debt payment) until your income minus your allocations equals zero. This forces a proactive and purposeful approach to every financial decision.

Is zero-based budgeting only for people with low incomes or debt?

Absolutely not. While ZBB is incredibly effective for those looking to get out of debt or manage limited resources, it’s equally powerful for high-income earners or those with significant wealth. It’s about intentionality and control, not just scarcity. Even wealthy individuals benefit from knowing exactly where their money is going, optimizing investments, and ensuring their spending aligns with their values and long-term financial goals, including strategies like How To Build Generational Wealth.

How do I handle variable expenses like groceries or utilities in a zero-based budget?

Variable expenses can be challenging, but there are strategies. For groceries, track your spending for a month or two to get an average, then budget that average amount. For utilities, you can budget the highest expected amount for the season, or use an average. If you come in under budget, reallocate the surplus. If you go over, you’ll need to adjust another category to maintain your “zero” balance. Over time, you’ll get better at estimating these categories.

What if I don’t spend all the money allocated to a specific category?

If you have money left over in a category at the end of the month (or even mid-month), you don’t just “keep” it there. In true zero-based budgeting, that money must be reallocated. Give it a new job! You might move it to your emergency fund, an investment account, an extra debt payment, or even roll it over to a specific savings goal for the next month. The goal is that no dollar is left without a purpose.

How often should I create a new zero-based budget?

It’s recommended to create a new zero-based budget at the beginning of each month. This monthly refresh ensures that your budget remains relevant to your current income, expenses, and financial goals. While the core categories might remain similar, starting from zero each time forces you to re-evaluate and justify every allocation, preventing complacency and ensuring optimal financial control. This is a key aspect of How To Create A Monthly Budget effectively.

What if I have an unexpected expense that wasn’t in my zero-based budget?

Unexpected expenses are why an emergency fund is crucial. Ideally, you’d cover such costs from your emergency savings. If you don’t have an emergency fund, or if the expense exceeds it, you’ll need to adjust your current month’s budget. This means going back to your existing categories and reducing spending in other areas (often discretionary categories first) to free up funds to cover the unexpected cost. The goal is always to get back to a zero balance, even if it means making tough choices.

Recommended Resources

You might also enjoy Affiliate Marketing For Beginners 2026 from Page Release.

Learn more about this topic in How To Start Investing With 100 Dollars at AssetBar.

From Our Network

- how to create a strong brand identity for your business (en Kacerr)

- startup marketing on a budget (en Pagerelease)

- how to build a brand from scratch (en Assetbar)